Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

For many Australians approaching or already in retirement, the Age Pension plays an important role in providing ongoing income support.

But eligibility isn’t automatic.

To qualify for the Age Pension (and to work out how much you may receive), Services Australia looks at two main tests:

The income test

The assets test

Whichever test results in the lower payment is the one that applies.

In this article, we’ll focus on the Age Pension assets test; what it is, what counts as an asset, what doesn’t, and how it can affect your Age Pension, with clear examples along the way.

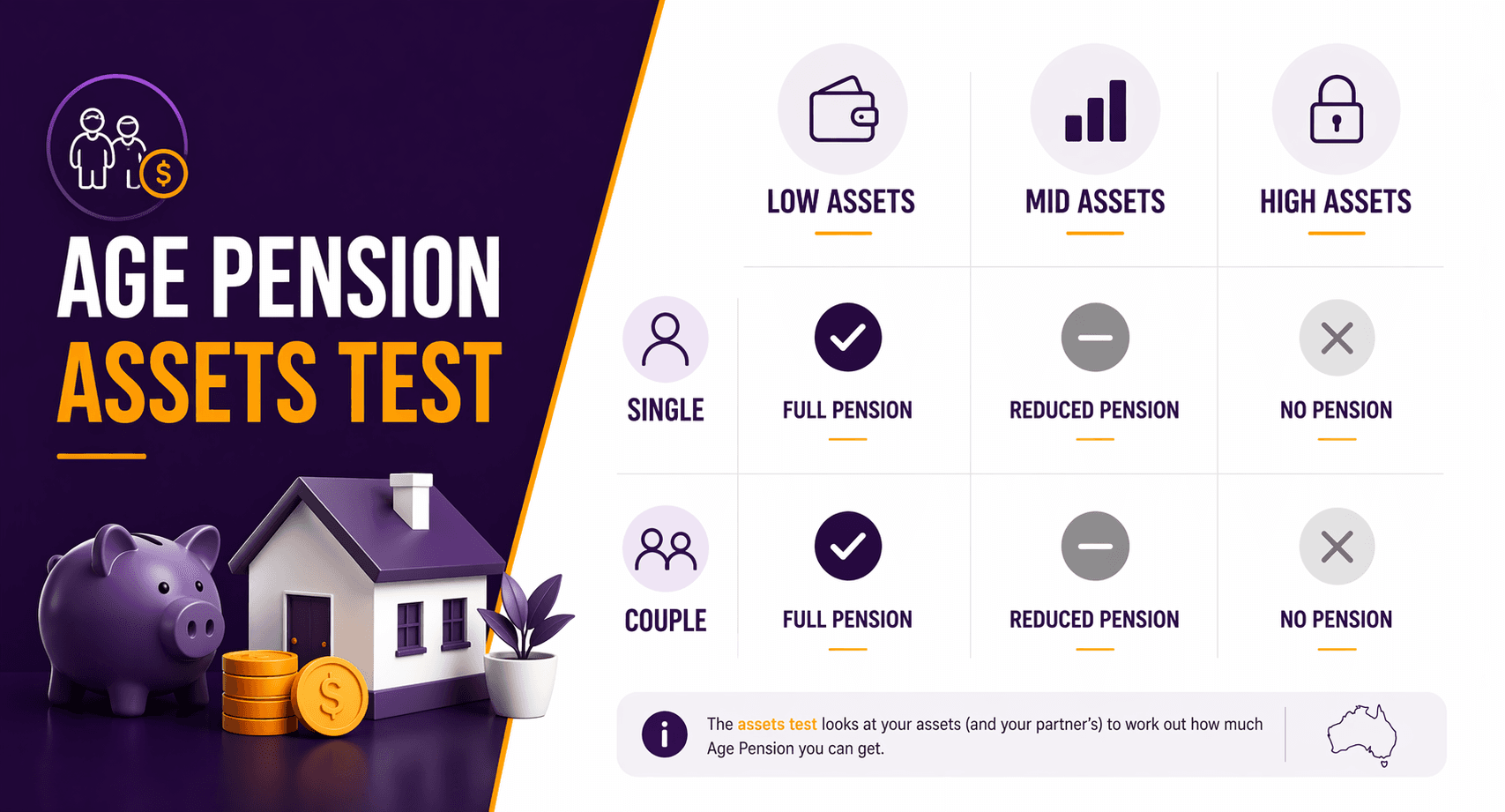

What Is the Age Pension Assets Test?

The assets test looks at the value of what you own, not what you earn.

If the total value of your assessable assets is:

below certain limits, you may receive the full Age Pension

above those limits, your pension may be reduced

above higher limits, you may not qualify at all

The actual asset thresholds change over time. Always check current Services Australia rules for up-to-date limits.

Why the Assets Test Matters

Many people assume:

“I don’t earn much income, so I’ll get the Age Pension.”

But the assets test can still reduce or cancel your pension if you own significant assets. Even if they don’t produce much income.

This commonly affects people who:

own investments or investment properties

have large super balances

have savings or shares

downsized their home and kept excess cash

moved money between different asset types

Understanding the assets test helps you avoid surprises and plan more confidently.

What Counts as an Asset Under the Assets Test?

Services Australia looks at the market value of most things you own, whether they produce income or not.

Common assets that ARE counted

1) Superannuation (in retirement)

Super is generally counted once you reach Age Pension age

This includes:

super accumulation accounts

account-based pensions

Before Age Pension age, super held in accumulation is generally not counted — but this changes once you reach Age Pension age.

2) Investment properties

Investment properties are assessed at market value

Any loans secured against them are usually deducted to get a net value

3) Shares and managed funds

Shares, ETFs, managed funds and similar investments are counted

Market value is used

4) Savings and cash

Bank account balances

Term deposits

Cash held outside super

5) Vehicles

Cars, caravans, boats and similar assets are counted

Value is usually based on market or resale value

6) Contents and personal belongings

Furniture, appliances, jewellery, collectibles, etc.

Usually assessed as a combined value, not item by item

7) Business assets

Business interests, goodwill, plant and equipment

Treatment can be complex and depends on structure and use

What Does NOT Count as an Asset?

The family home (principal residence)

For most people, your home is exempt from the assets test.

This means:

The value of the home you live in is not counted

It doesn’t matter how valuable the home is

However:

Assets outside the home (cash, investments) still count

Downsizing and holding large amounts of cash can affect pension outcomes

Some other exclusions (depending on circumstances)

Certain prepaid funeral expenses

Some compensation payments

Certain special-purpose assets

Rules vary, so it’s important to check current Centrelink guidance.

Homeowners vs Non-Homeowners: Why It Matters

The assets test uses different thresholds depending on whether you:

own your home, or

do not own your home (renting, living in a retirement village, etc.)

Generally:

Non-homeowners are allowed higher asset limits

Homeowners have lower asset limits, because the home itself is exempt

This difference can significantly affect Age Pension outcomes.

How the Assets Test Reduces Your Pension

Once your assets exceed the lower threshold:

your Age Pension is reduced progressively

for every additional amount of assets, your pension reduces by a set rate

If your assets exceed the upper limit:

your Age Pension reduces to zero

Exact reduction rates and thresholds are set by Services Australia and can change and always check current rules.

Assets Test Examples (Simple Scenarios)

Example 1: Homeowner with modest assets

Maria is retired and owns her home outright.

She has:

some super in an account-based pension

a small share portfolio

modest cash savings

Her total assessable assets are below the lower threshold.

Maria may qualify for the full Age Pension, subject to the income test.

Example 2: Homeowner with higher investments

David and Anne own their home and have:

a larger super balance

an investment portfolio

Their assessable assets exceed the lower threshold but are below the upper limit.

They may qualify for a part Age Pension, reduced under the assets test.

Example 3: Non-homeowner with significant cash

Tom rents and has:

sold his former home

kept a large amount of cash and investments

Because he is a non-homeowner, higher asset thresholds apply.

He may still qualify for a part Age Pension, even with higher assets than a homeowner.

Example 4: Assets too high

Jenny owns her home and has:

a large super balance

an investment property

Her assessable assets exceed the upper limit.

She may not qualify for the Age Pension under the assets test (even if her income is low).

Common Traps and Misunderstandings

1) “My super won’t affect my pension”

Once you reach Age Pension age, super generally does count as an asset.

2) “If I give money away, it won’t count”

Gifting rules apply. Large gifts can still be counted as assets for Centrelink purposes for a period of time.

3) “Downsizing always improves pension outcomes”

Downsizing can:

reduce housing costs

free up cash

But if the cash sits outside the home, it becomes accessible, which can reduce or cancel the Age Pension.

4) “I only need to worry about income, not assets”

Many retirees lose pension entitlements due to assets, not income.

Assets Test vs Income Test: Which One Applies?

Both tests are assessed.

Services Australia calculates your payment under both

The lower result applies

This means:

You can pass the income test but fail the assets test

Or pass the assets test but fail the income test

Good retirement planning considers both together.

Planning Considerations (Without Getting Technical)

The goal is not to “game” Centrelink rules. It’s to:

understand how decisions affect outcomes

avoid unintended consequences

align lifestyle, income and eligibility sensibly

Things worth considering:

how assets are held (inside vs outside super)

timing of super withdrawals

downsizing decisions

long-term income needs vs pension eligibility

how long retirement may last

This is where personalised advice and modelling is valuable.

Key Takeaways

The Age Pension assets test looks at what you own, not what you earn

Most assets are counted, including super (after pension age), investments and cash

The family home is usually exempt

Different limits apply to homeowners and non-homeowners

Exceeding thresholds can reduce or eliminate the Age Pension

Assets test and income test both apply, the lower result wins

Small decisions (like downsizing or moving money) can have big pension impacts

FAQ (5 Questions with Short Answers)

1) What is the Age Pension assets test?

It’s a Centrelink test that assesses the value of your assets to determine whether you qualify for the Age Pension and how much you receive.

2) Does my home count under the assets test?

Generally no. Your principal residence is exempt from the assets test.

3) Does super count for the Age Pension assets test?

Once you reach Age Pension age, super is generally counted as an asset.

4) What happens if my assets are over the limit?

Your Age Pension may be reduced or stop completely, depending on how far over the limit you are.

5) Is the assets test the only test that applies?

No. Centrelink applies both the assets test and income test, whichever results in the lower payment is used.

The Age Pension assets test can feel confusing, but at its core it’s about understanding how what you own affects your eligibility.

Before making big decisions; like accessing super, downsizing, or moving investments, it’s important to understand how those choices interact with Centrelink rules.

Want clarity on how your assets affect your Age Pension?

At What If Advice, we help Australians:

understand Centrelink rules

model Age Pension outcomes

plan super withdrawals alongside pension eligibility

make informed retirement decisions

Book a Retirement & Super Workshop and get a clear picture of how your assets and retirement plans work together.

General Advice Disclaimer

This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions.