Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

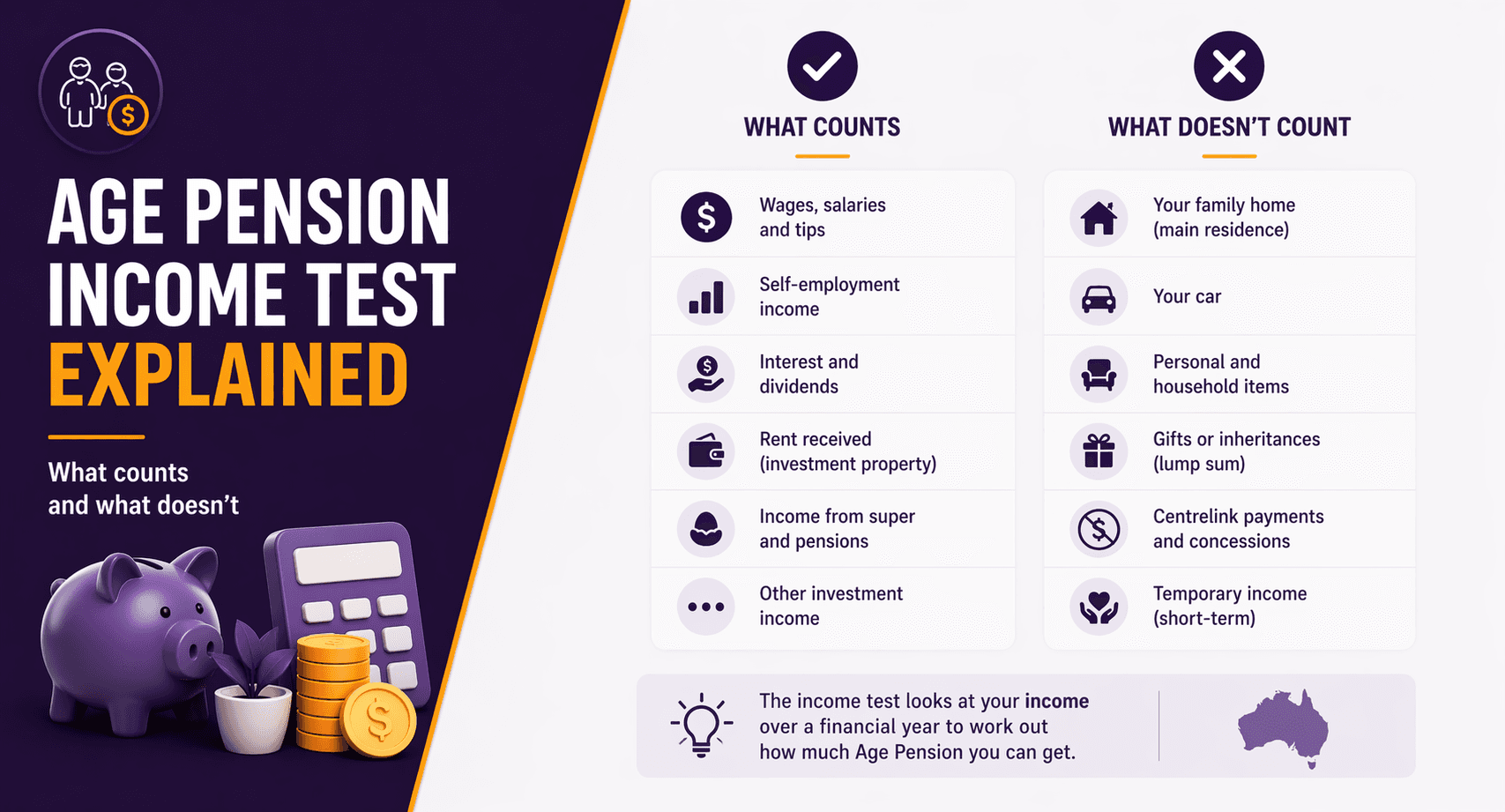

Age Pension income test explained (what counts and what doesn’t)

If you’re approaching retirement, the Age Pension income test is one of the biggest “unknowns”. Many Australians assume it only looks at wages, but Services Australia may assess a wider range of income; especially income from financial assets under deeming. The good news: once you understand the categories, you can gather the right paperwork, avoid surprises, and make better decisions about work, superannuation and savings.

This guide explains the income test in plain English, with common examples of what usually counts and what often doesn’t. Always subject to current Services Australia rules.

Quick answer: what’s the income test in one paragraph?

The Age Pension income test looks at the income Services Australia assesses you (and your partner, if applicable) as receiving. Some income is “actual” (like wages or rent). Other income is “deemed” (an assumed amount earned from certain financial assets such as bank accounts and shares, regardless of what you actually earn). If your assessable income is above the relevant limits, your Age Pension may reduce, and above a higher point it may cut out entirely, subject to current Services Australia rules.

How does the Age Pension income test work?

Services Australia applies two separate tests: an assets test and an income test. Your payment is generally based on whichever test results in the lower pension rate.

The income test is designed to target payments to people who have less income coming in.

What does “assessable income” mean?

“Assessable income” is the income Services Australia counts for the purpose of the income test. It’s not the same as taxable income, and it’s not always what you receive in your bank account.

In practice, assessable income commonly includes a mix of:

Employment income (if you still work)

Income from investments (often calculated using deeming)

Income from other sources (for example, some pensions or rent)

What income usually counts under the Age Pension income test?

What counts depends on the type of income and the product structure. The list below covers common categories and the typical treatment, subject to current Services Australia rules.

Does employment income count (wages, salary and self-employment)?

Generally, yes. If you or your partner continue working, wages and salary are usually assessed as income.

Self-employment income can be more complicated. Services Australia may look at business income differently to your tax return figures, and may ask for profit-and-loss information.

If you’re working, also ask about any applicable Work Bonus arrangements and reporting requirements, subject to current Services Australia rules.

Do bank accounts, shares and managed funds count as income?

Often, yes. But commonly via deeming rather than your actual interest or dividends.

Financial assets that may be deemed can include:

Savings and transaction accounts

Term deposits

Listed shares and many managed funds

Deeming means Services Australia applies assumed rates of return to the value of those assets. This can surprise people who hold lots of cash earning low interest, because the deemed income may be higher than what they actually receive (or lower, depending on market conditions). Deeming rates and thresholds can change, so check the current settings.

Do investment properties and rent count?

Rent you receive is generally treated as income, subject to current Services Australia rules. Services Australia may allow certain deductions (for example, some costs of earning rental income), but the treatment is not the same as negative gearing in the tax system.

If you own a holiday home or a second property that produces no rent, it may not create income, but it may still matter under the assets test.

Do superannuation income streams count?

Often, yes. Particularly if you are over Age Pension age and receiving income from an account-based pension or other retirement income stream.

The income test treatment can depend on:

The type of income stream (account-based pension vs other structures)

The start date and rules applying to that product

Whether the income is assessed under deeming or under an “income stream” assessment method

Because product rules vary, it’s worth confirming the specific Centrelink assessment for your super pension rather than assuming.

Do other pensions and overseas income count?

Income from other sources, such as certain defined benefit pensions, compensation payments, or overseas pensions, may be assessed. Overseas income and assets can affect both the income and assets tests.

If you have lived or worked overseas, keep records handy and expect extra questions, subject to current Services Australia rules.

What income may not count (or may be treated differently)?

Some amounts may be excluded, partially exempt, or assessed in a specific way. The exact treatment depends on your circumstances and current rules.

Does the family home affect the income test?

Your principal home is generally not counted as an asset under the assets test, and it typically doesn’t produce income for the income test. However, decisions around downsizing, renting out rooms, or moving into aged care can change the picture.

Are gifts and one-off withdrawals “income”?

A one-off withdrawal from your own bank account is usually not “income” (it’s your capital), but it may change your asset balances and therefore deeming.

Gifting can be complex. Giving away money may still be counted under the assets test (and can affect deeming) for a period of time, subject to current Services Australia rules. Before making large gifts, check the implications.

What about inheritances?

An inheritance is generally not “income” in the ordinary sense, but once received it becomes an asset. That can increase deemed income and may affect your Age Pension rate.

Does the Age Pension itself count as income?

The Age Pension is not assessed as income for calculating itself. But it may interact with other payments and tax outcomes depending on your overall situation.

Common traps that affect your Age Pension rate

Even when you know what counts, these practical issues can catch people out:

Not updating asset balances: Deeming is based on the value of your financial assets.

Assuming taxable income equals assessable income: Centrelink rules are different.

Overlooking partner income: Couples are assessed together for many rules.

Changing from accumulation to pension phase in super: The assessment may change at Age Pension age.

Renting out part of your home: It can create assessable income and may affect exemptions.

How can you prepare before you claim?

A small amount of preparation can make the claim process smoother.

What documents should you gather?

Commonly useful documents include:

Recent bank statements and term deposit details

Shareholding or managed fund statements

Superannuation balances and pension details

Rental statements (if applicable)

Payslips or business financials (if you work)

Details of any overseas pensions or assets

When should you update Services Australia?

Report changes promptly. Such as selling an asset, starting an income stream, stopping work, or receiving a lump sum, subject to current Services Australia reporting rules.

FAQs

1. What counts as income for the Age Pension income test?

Assessable income commonly includes wages, net rental income, and income from financial assets (often calculated using deeming). Some income streams and overseas payments may also be assessed, subject to current Services Australia rules.

2. What is deeming and why does it matter?

Deeming is a method where Services Australia assumes your financial assets earn a set rate of return. It matters because your Age Pension may be reduced based on deemed income even if your actual interest or dividends are lower, subject to current rules.

3. Does my superannuation count as income?

It depends on your age and how your super is structured. Once you’re over Age Pension age, super in certain forms (including many income streams) can affect the income test either through deeming or income-stream rules, subject to current Services Australia rules.

4. Does rent from an investment property reduce my Age Pension?

Rent is generally assessed as income, which can reduce your Age Pension depending on the amount and your overall situation. Some expenses may be recognised, but the calculation is not the same as your tax return, subject to current Services Australia rules.

5. Can I still work and get the Age Pension?

Many people can. Wages are generally assessed under the income test, but there may be concessions such as the Work Bonus and different reporting arrangements. Always check the current rules before relying on a specific outcome.

The Age Pension income test is about more than just wages. It can include rent, some pensions, and most importantly for many retirees, deemed income from bank accounts, shares and managed funds. Understanding what is likely to be assessed (and what may be treated differently) helps you avoid nasty surprises and plan your retirement income with more confidence.

Learn how the rules fit your retirement plan

Want help mapping your super, savings and any part-time work against the Age Pension income and assets tests (subject to current Services Australia rules)? Join a What If Advice retirement workshop to learn the key moving parts and the questions to ask before you lodge a claim.

General advice disclaimer

This article is general information only and doesn’t take into account your objectives, financial situation or needs. It’s not personal financial advice. Rules and interpretations can change and eligibility depends on your circumstances, subject to current Services Australia and ATO rules. Consider getting personal advice before making decisions.