Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

When you’re starting or growing a business, it’s tempting to choose the simplest option (usually sole trader) and “sort the rest later”.

But your business structure is more than paperwork, it affects:

how much tax you pay

how much personal risk you carry

how you pay yourself

how easy it is to bring in partners or investors

how your profits can be distributed

your accounting, admin and compliance

your long-term wealth and asset protection

In Australia, the most common structures are:

Sole trader

Company (Pty Ltd)

Trust (usually a discretionary/family trust)

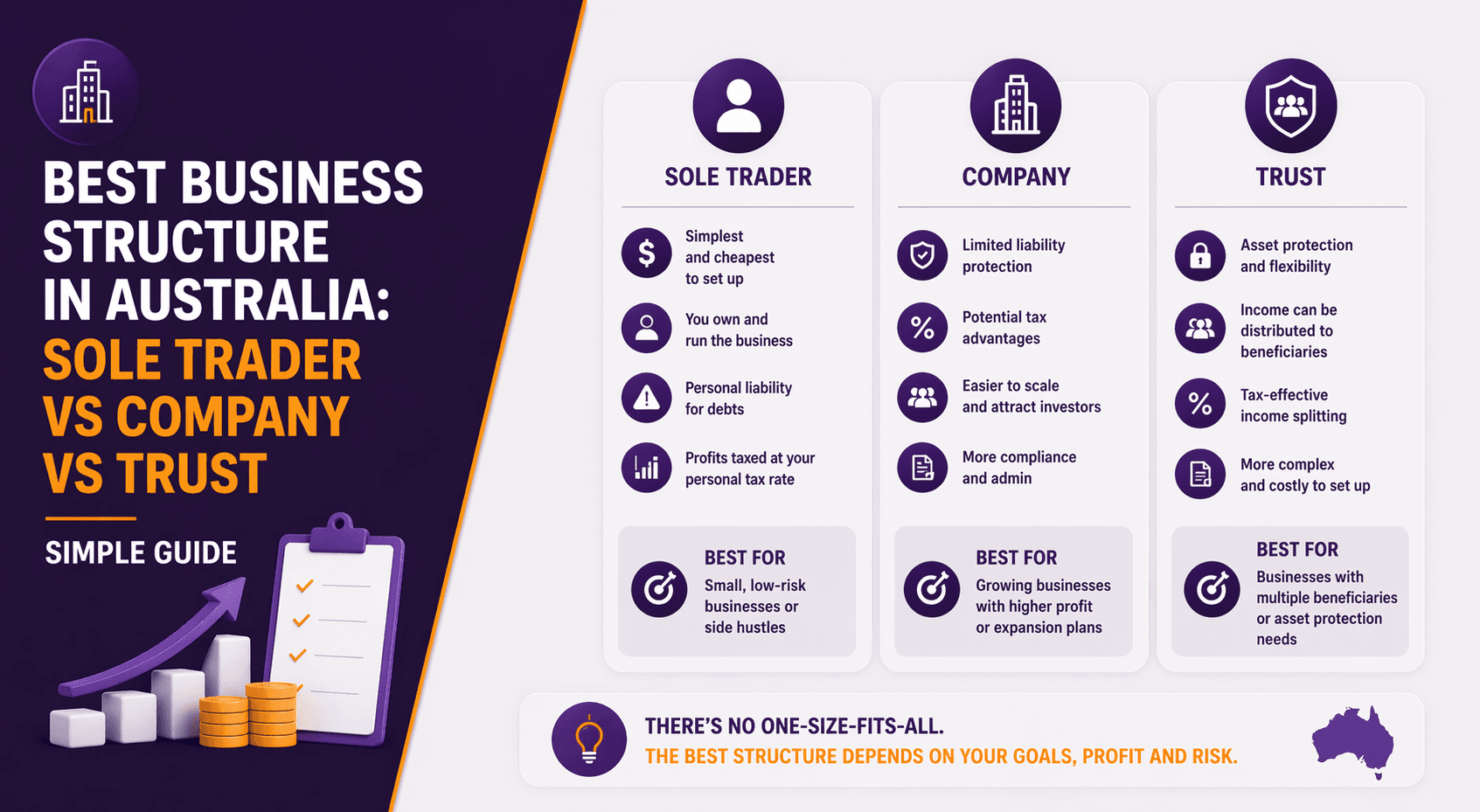

There’s no single “best” structure for everyone. The best option depends on your income level, risk, growth plans, and personal circumstances.

Let’s break it down clearly, without jargon.

Quick Snapshot: Which Structure Suits Who?

Sole trader is often best if:

you’re starting out or testing an idea

income is still modest or unpredictable

you want low cost and minimal admin risk is low (e.g., service-based work with low liabilities)

Company is often best if:

you’re earning consistent profits

you want limited liability protection

you want better separation between business and personal

you plan to hire staff or scale

you want flexibility in paying yourself (salary/dividends)

Trust is often best if:

you want flexibility to distribute profits to different beneficiaries

you want asset protection (in the right setup)

you want long-term family wealth planning

you have strong profits and professional support

you’re comfortable with extra admin and compliance

What Is a Sole Trader Structure?

A sole trader is the simplest structure. You operate the business as an individual.

How tax works

You declare business income in your personal tax return, and you pay tax at individual marginal tax rates.

Pros of being a sole trader

Cheap to set up

Minimal admin (compared to company/trust)

Full control over decisions

Simple bookkeeping and tax reporting

Good for side hustles and early-stage businesses

Cons of being a sole trader

You are personally liable for business debts and legal issues

Harder to separate personal assets from business risk

Profit taxed at personal rates (can become expensive as income rises)

Harder to bring in partners/investors

Some lenders and suppliers may prefer dealing with a company for larger arrangements

Example: sole trader may suit

A freelance designer or consultant earning under (say) mid-six figures, with minimal business debt and low legal risk.

What Is a Company Structure (Pty Ltd)?

A company is a separate legal entity registered with ASIC. It can own assets, borrow money, and enter contracts in its own name.

How tax works

A company pays tax at the company tax rate, which is different from individual tax rates. The full rate is 30%, and a lower rate may apply to “base rate entities” (depending on current ATO rules).

Then, when you take profits out (via salary or dividends), tax is assessed depending on how it’s paid and your personal situation.

Pros of a company

Limited liability (your personal assets are generally more protected)

Clear separation between business and personal finances

Perceived as more “established” by clients, lenders and suppliers

Can be more tax-effective once profits are high

More flexible for growth, staff, investors and future sale

Cons of a company

Higher setup and ongoing costs

More admin: ASIC obligations, director duties, extra reporting

Must keep good records and run properly (minutes, compliance, accounts)

Director obligations can still create personal risk if mismanaged

Example: company may suit

A trades business, agency, or product business earning strong profits consistently, hiring staff, and taking on risk/contracts.

What Is a Trust Structure?

A trust is a legal structure where a trustee holds and manages assets on behalf of beneficiaries.

Most business owners who use a trust use a discretionary (family) trust, which can distribute income to different beneficiaries (within the trust deed rules).

How tax works

A trust generally doesn’t pay tax as a separate entity if it distributes income to beneficiaries. The beneficiaries pay tax at their own marginal rates on the distributions they receive.

If the trust retains income (or does not distribute properly), tax outcomes can become less favourable.

Pros of a trust

Flexibility to distribute profits among family members (where appropriate)

Can support long-term family wealth planning

Potential asset protection (depending on design and how it’s used)

Useful for investment income and holding assets

Can be combined with a company (“bucket company”) for planning (with correct advice)

Cons of a trust

More complex and more expensive than sole trader

Requires ongoing accounting support and documentation

Distributions must be done correctly and on time

Trust losses generally can’t be distributed like income, losses stay in the trust and are carried forward subject to rules

Trust arrangements and distribution strategies are an area of ATO scrutiny documentation and “doing it right” is essential

Example: trust may suit

A business with strong profits where the owner wants flexibility to distribute income to a spouse/adult beneficiaries (where appropriate), and wants asset protection and long-term wealth strategy.

Key Comparison: Sole Trader vs Company vs Trust

1) Liability (personal risk)

Sole trader: You are personally liable

Company: Limited liability (but directors still have responsibilities)

Trust: Liability depends on trustee structure (corporate trustee is common for protection)

2) Tax flexibility

Sole trader: Taxed at your personal marginal rates

Company: Taxed at company tax rate, then taxed again when profits are paid out (depending on method)

Trust: Income can be distributed to beneficiaries for potentially flexible tax outcomes (within rules)

3) Setup + ongoing admin

Sole trader: Lowest cost, simplest

Company: More admin and ASIC obligations

Trust: Complex, requires careful compliance and documentation

4) Paying yourself

Sole trader: drawings (not a wage)

Company: salary and/or dividends

Trust: distributions to beneficiaries (and potentially salary if employing you)

5) Growth and investment

Sole trader: harder to scale and bring in investors

Company: easier to scale, sell, bring in shareholders

Trust: can be very effective for holding assets and long-term wealth, but not as simple for investors

“Best Structure” Depends on Your Stage of Business

If you’re starting out (low income, testing ideas)

Sole trader is usually the simplest and cheapest.

But it’s worth reviewing if:

profit grows quickly

risk increases (contracts, staff, debt, legal exposure)

your personal tax bracket climbs

you begin investing profits

If you’re growing (profits increasing and consistent)

A company often becomes attractive because of:

limited liability

professionalism

flexibility in reinvesting profits

scalability and sale potential

If you’re profitable and planning long-term wealth

A trust (or trust + company) can make sense when:

you want income distribution flexibility

you want asset protection layers

you’re building investments

you want intergenerational wealth planning

you can afford the setup and admin

Common “Best Practice” Structures Australians Use

1) Sole trader (basic)

Good for early stage. Often evolves later.

2) Company only

Good for growth, limited liability, strong profits, simple reinvestment.

3) Family trust (with corporate trustee)

Good for asset protection and flexibility, but must be managed properly.

4) Trust + Company (“bucket company”)

Common for higher-profit businesses and families where:

trust earns income

distributes to a company beneficiary (within rules)

company retains profits at company tax rates

cash and documentation are managed properly

This is powerful but complex and needs professional advice because trusts are a focus area for ATO compliance and documentation standards.

Mistakes to Avoid When Choosing a Structure

1) Choosing based on “tax savings” only

Tax matters, but so do:

risk exposure

admin costs

your lifestyle and exit plans

personal borrowing needs

industry requirements

2) Setting up a structure you can’t maintain

A trust or company structure is pointless if:

records are messy

distributions aren’t documented properly

BAS and tax are always late

business and personal spending are mixed

3) Ignoring liability

If your business has contracts, staff, equipment, debt, or public-facing risk, a sole trader structure may expose your personal assets more than you realise.

4) Not planning “how you’ll pay yourself”

Different structures change whether you use:

wages

dividends

trust distributions

drawings

Your pay strategy affects tax, super, and compliance.

Practical Checklist: How to Choose the Right Structure

Ask yourself:

Income & profitability

How much profit do I expect this year?

Will I reinvest profits or withdraw most of it?

Risk & liability

Am I exposed to legal claims?

Do I have debt, staff, or contracts?

Growth plans

Do I plan to scale, hire, or sell?

Do I want to bring on partners/investors?

Personal and family planning

Do I want to distribute income to family beneficiaries (where appropriate)?

Am I building investments or assets outside the business?

Admin tolerance

Am I willing to maintain higher compliance requirements?

Key Takeaways

Sole trader is simple and cheap but offers little liability protection

Company structures offer limited liability and flexibility for growth, but have higher admin costs Trusts can provide distribution flexibility and wealth planning benefits, but require strong compliance and documentation

The best structure depends on your profits, risk, growth plans and long-term goals

Many businesses evolve from sole trader → company → trust/company combination as they grow

The wrong structure can cost you in tax, risk and admin time

FAQ

1) What is the best business structure in Australia?

There isn’t one best structure for everyone. The best structure depends on your income, risk exposure, growth goals, and need for tax and asset protection strategies.

2) Should I start as a sole trader or a company?

Many people start as a sole trader because it’s cheaper and simpler. If profit becomes consistent or risk increases, a company may be worth considering.

3) Is a trust better than a company for tax?

A trust can offer flexibility in distributing income to beneficiaries, but it’s not automatically “better”. Trusts are complex and need correct documentation and compliance.

4) Can a trust run a business in Australia?

Yes. A trust can operate a business, with the trustee responsible for running the trust’s affairs.

5) Can I change business structure later?

Yes, but changing structures can trigger tax and legal consequences (for example, transferring assets). It’s best to plan before switching and get advice.

Still asking “what if” about your finances?

That’s exactly where clarity begins.

Whether you’re planning ahead, growing wealth, or simply want confidence in your financial decisions, the advisers at What If Advice can help you turn questions into a clear, personalised plan.

👉 Book a free 15-minute strategy session or get in touch today at

whatifadvice.com.au

General Advice Disclaimer

This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions. You should seek professional tax and legal advice before establishing or changing a business structure.