Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

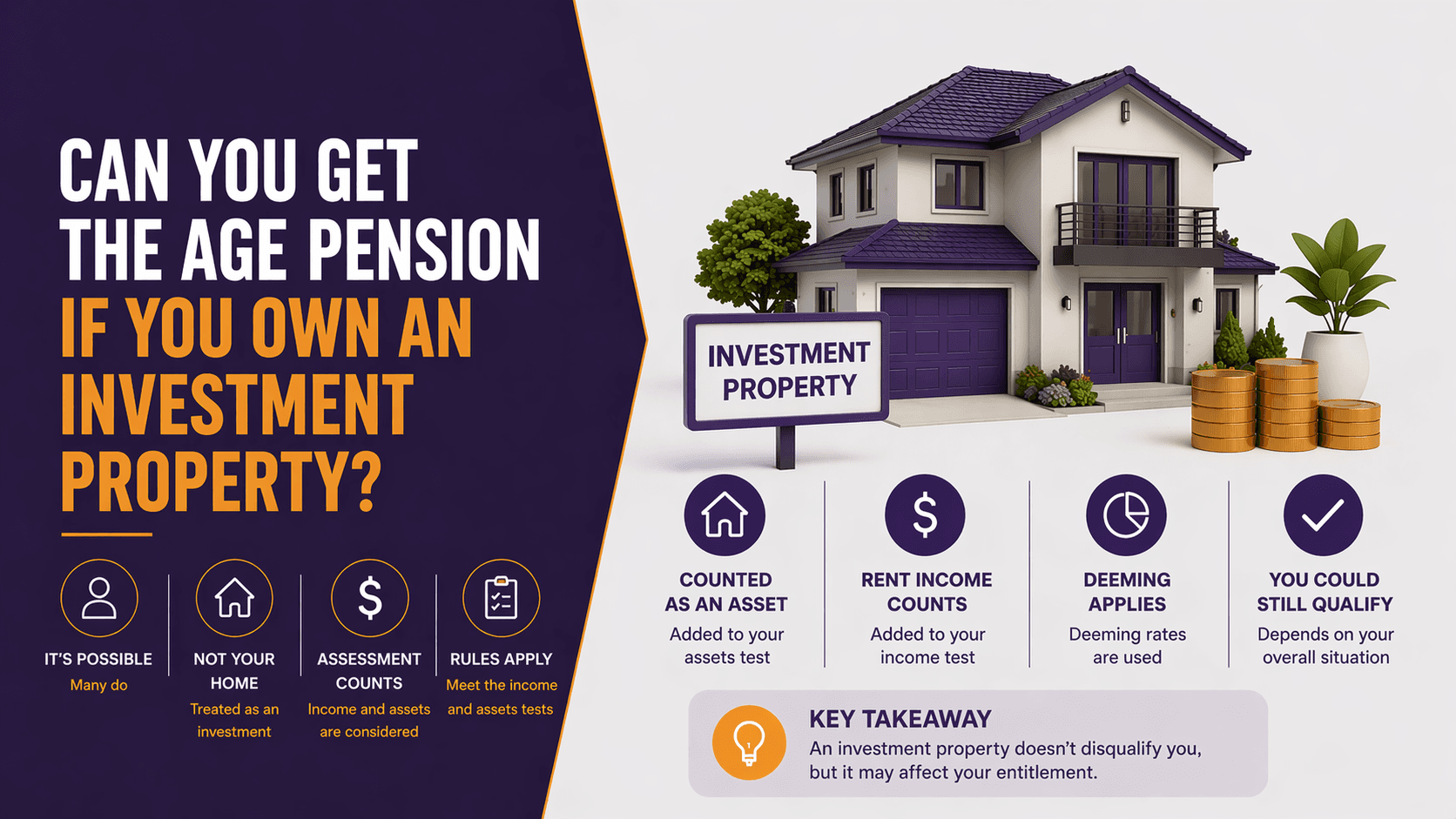

Can You Get the Age Pension If You Own an Investment Property?

Yes, it is possible to receive the Age Pension while owning an investment property.

However, the property will be assessed under the Age Pension means tests, which include:

The assets test

The income test

Both the value of the property and the rental income it produces can influence how much Age Pension you receive.

(All rules subject to current Services Australia regulations.)

How the Age Pension Means Test Works

To determine Age Pension eligibility, Services Australia applies two assessments:

Test | What It Measures |

Income Test | Income from work, investments and pensions |

Assets Test | Total value of assets excluding the family home |

Your pension payment is determined by whichever test produces the lower result.

How Investment Property Is Treated Under the Assets Test

Unlike your principal residence, investment properties are not exempt from the Age Pension assets test.

The property is assessed based on its market value, minus any outstanding mortgage attached to the property.

Example:

Property Value | Mortgage | Assessable Value |

$700,000 | $200,000 | $500,000 |

The assessable value is added to your other assets when calculating Age Pension eligibility.

Rental Income and the Income Test

Rental income from an investment property is assessed under the Age Pension income test.

Services Australia generally considers:

Gross rental income

Allowable deductions related to the property

The resulting net income may count toward your assessable income.

This income may reduce your Age Pension depending on total income levels.

Example Scenario

David is a retired homeowner with:

Principal home: exempt

Investment property worth $450,000

Rental income: $18,000 per year

Savings: $100,000

Under Age Pension rules:

The investment property value is included in the assets test.

The rental income is included in the income test.

His final Age Pension payment depends on which test reduces it more.

Can You Still Qualify for a Part Age Pension?

Yes.

Many retirees who own investment property still receive a partial Age Pension.

Eligibility depends on:

Total asset levels

Rental income

Other financial investments

Household structure (single or couple)

The Age Pension gradually reduces as assets and income increase.

Investment Property vs Financial Investments

Investment property is treated differently from financial assets.

Asset Type | Income Assessment |

Financial assets | Deemed income |

Rental property | Actual rental income |

This difference can influence retirement income planning decisions.

Should Retirees Keep Investment Property?

The decision depends on several factors:

Income Stability

Rental income can provide steady retirement cash flow.

Property Maintenance

Owning property involves ongoing maintenance, management and costs.

Liquidity

Property is less liquid than financial investments.

Age Pension Impact

Large property values may reduce pension eligibility.

Retirement property decisions should consider both financial and lifestyle factors.

Downsizing or Selling Property

Some retirees choose to sell investment property in retirement.

Possible benefits include:

Access to capital

Simpler investment structure

Reduced management responsibilities

However, selling may trigger capital gains tax and affect Age Pension eligibility depending on how proceeds are invested.

Common Mistakes Retirees Make

Retirees sometimes misunderstand how investment property affects the Age Pension.

Common misconceptions include:

Thinking rental property is exempt like the family home

Ignoring rental income under the income test

Assuming property ownership automatically cancels the pension

Not reviewing asset values regularly

Understanding these rules can help retirees plan more effectively.

FAQs

1. Can I receive the Age Pension if I own an investment property?

Yes. However, the property is included in the assets test and rental income is included in the income test.

2. Is the family home counted for the Age Pension?

No. Your principal residence is generally exempt from the assets test.

3. Does rental income reduce the Age Pension?

Yes. Rental income is assessed under the income test and may reduce pension payments.

4. How is an investment property valued?

Services Australia generally uses the market value of the property when assessing assets.

5. Can I have multiple investment properties and still receive a pension?

Possibly. Eligibility depends on total asset values and income levels.

6. Should I sell my investment property before retirement?

This depends on factors such as cash flow, tax implications and pension eligibility.

Understand How Property Affects Your Pension

Owning investment property can provide valuable retirement income, but it can also influence Age Pension eligibility.

At What If Advice, we help Australians understand how property, superannuation and other assets interact with pension rules under current Services Australia regulations.

If you own property and want clarity on how it affects your retirement income, professional advice can help you plan effectively.

Book an Age Pension strategy consultation with What If Advice.

General Advice Disclaimer

This article provides general information only and does not take into account your personal objectives, financial situation or needs. Before making financial decisions, consider whether the information is appropriate to your circumstances and seek personal advice from a licensed financial adviser. Age Pension, taxation and superannuation rules are subject to change under current Services Australia and ATO regulations.