Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

Superannuation is one of the best long-term wealth tools Australians have, but the rules around contributions can feel like a maze.

One of the biggest points of confusion is the difference between:

Concessional contributions (before-tax)

Non-concessional contributions (after-tax)

Both are ways to grow your super. But they’re taxed differently, have different contribution caps, and can suit different strategies depending on your stage of life.

This guide breaks it down in a simple, practical way without jargon.

What Are Super Contributions?

Super contributions are the payments that go into your super fund. They can come from:

your employer (like Super Guarantee contributions)

your own money (extra contributions)

your spouse (in some cases)

government payments (in some situations)

The type of contribution matters because it affects:

how much tax you pay

whether you get a tax deduction

how much you’re allowed to contribute each year

whether you may be penalised if you exceed caps

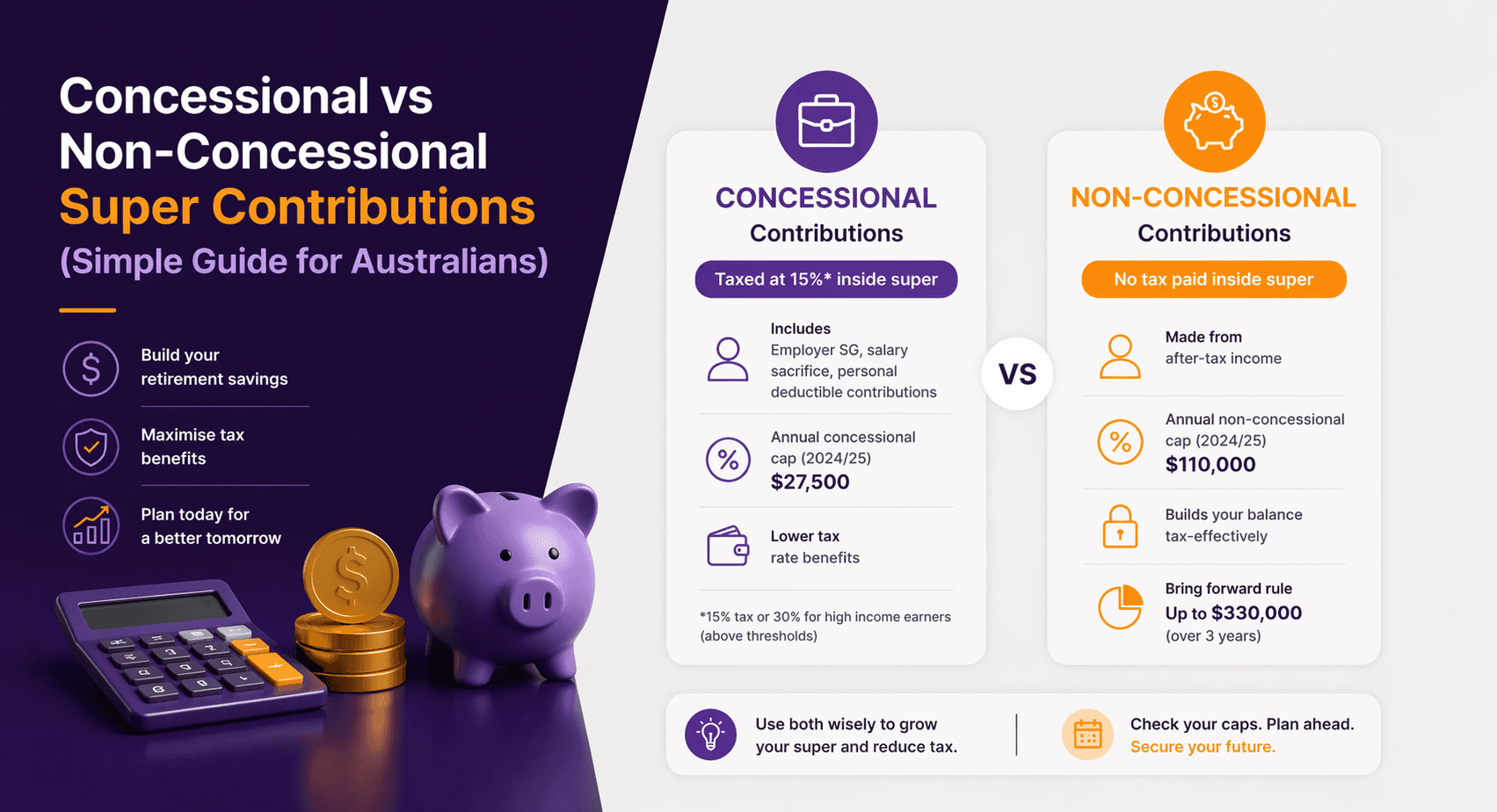

The Two Main Types: A Simple Summary

Concessional contributions = “before-tax” contributions

These are contributions where the ATO gives you a tax concession (a tax benefit).

They include:

employer Super Guarantee contributions

salary sacrifice contributions

personal contributions where you claim a tax deduction

They’re generally taxed at a concessional rate inside super (subject to rules and your income level).

Non-concessional contributions = “after-tax” contributions

These are contributions you make from money you’ve already paid income tax on.

They include:

personal after-tax contributions (where you do not claim a tax deduction)

spouse contributions (usually)

contributions from a personal savings account (without claiming deductions)

These generally aren’t taxed when they enter super (but caps and eligibility rules apply).

Concessional Contributions Explained (Plain English)

What counts as concessional?

Concessional contributions include:

Employer contributions (Super Guarantee)

Salary sacrifice contributions

Personal contributions you claim as a deduction

Example:

You earn $90,000 per year and your employer pays your Super Guarantee amount into your super. That employer contribution is concessional.

How are concessional contributions taxed?

Concessional contributions are typically taxed inside super at a lower rate than most people’s personal tax rate, which is why they’re popular.

However:

higher income earners may pay extra tax on concessional contributions

the ATO applies strict annual caps

you may pay additional tax if you exceed the cap

Always check the current ATO concessional contribution cap as it can change.

Why use concessional contributions?

Concessional contributions are often used to:

reduce personal taxable income

boost retirement savings efficiently

build super faster (because tax inside super can be lower)

catch up in later years (using carry-forward rules if eligible)

In simple terms:

If you earn a reasonable income and want to save for retirement, concessional contributions can be one of the smartest ways to do it.

Common concessional contribution strategies

1) Salary sacrifice

This is when you ask your employer to divert some of your pre-tax salary into super.

Example:

Instead of receiving $200 per week in your bank, you salary sacrifice it into super.

This can:

reduce your taxable income

increase your retirement balance

potentially help you save more without “feeling” it too much

2) Personal deductible contributions

This is when you make a contribution from your bank account and later claim it as a tax deduction through the ATO.

This is popular for:

self-employed people

people with irregular income

people who want to top up near the end of the financial year

Non-Concessional Contributions Explained (Plain English)

What counts as non-concessional?

Non-concessional contributions include:

Personal after-tax contributions (without claiming a deduction)

Spouse contributions

Contributions made from savings or inheritance (after-tax money)

Example:

You receive a $20,000 inheritance and put it into your super without claiming a tax deduction that’s a non-concessional contribution.

How are non-concessional contributions taxed?

Generally, non-concessional contributions:

enter super without contributions tax

(because you’ve already paid tax on that money)

But they are subject to strict caps and eligibility rules.

Always check the current ATO non-concessional contribution cap, especially if you plan to contribute a large amount.

Why use non-concessional contributions?

Non-concessional contributions are often used to:

build super faster if you already have savings

contribute proceeds from selling an asset

invest outside cash into a tax-advantaged environment

boost super closer to retirement

fund spouse contribution strategies

Non-concessional contributions can be powerful for people who:

have a lump sum to invest

are approaching retirement

want to maximise super balances over time

Concessional vs Non-Concessional: The Key Differences

Here’s the simplest comparison:

Concessional contributions

Paid from before-tax income

Includes employer super + salary sacrifice + deductible contributions

Usually taxed when entering super

Can reduce your taxable income

Has an annual cap (check ATO)

Non-concessional contributions

Paid from after-tax money

Usually not taxed when entering super

Does not reduce taxable income

Has an annual cap (check ATO)

Eligibility rules may apply (e.g., total super balance limits)

Which One Should You Use?

The best type depends on your situation, goals, and income.

Concessional contributions may suit you if:

you are working and earning income

you want to reduce taxable income

you want to build super efficiently

you want to salary sacrifice

you’re catching up on retirement savings

Non-concessional contributions may suit you if:

you have savings you want to invest long-term

you’ve received a lump sum (inheritance, bonus, sale of asset)

you’re nearing retirement and want to boost super

you’re maximising super after already hitting concessional limits

you want to support a spouse’s super strategy

Common Mistakes to Avoid

Super contribution rules are strict, and mistakes can lead to tax headaches.

Here are common issues Australians run into:

1) Exceeding contribution caps

If you exceed the concessional or non-concessional cap, the ATO may apply additional tax and require you to withdraw amounts.

Tip: Track contributions throughout the year; especially employer contributions, which are often overlooked.

2) Forgetting employer contributions count

Many people's salary sacrifice without realising employer contributions already use up part of the concessional cap.

Example:

You salary sacrifice $20,000 but forget your employer contributed $12,000, you may exceed the cap.

3) Claiming a deduction incorrectly

If you plan to claim a personal contribution as a deduction, you must follow ATO steps (including submitting a notice of intent to claim a deduction to your fund).

If you do this incorrectly:

you may lose the deduction

you may accidentally trigger non-concessional treatment

your tax return may become messy

4) Assuming non-concessional contributions are always allowed

Non-concessional contributions can be restricted depending on:

your age

your total super balance

whether you meet eligibility rules

Always check current ATO rules before making large contributions.

Practical Examples (So It Makes Sense)

Example 1: Salary sacrifice (concessional)

Sam earns $85,000 and wants to reduce tax and build super.

He salary sacrifices $150 per week.

This is a concessional contribution, and it counts toward the concessional cap (along with employer super).

Example 2: Personal deductible contribution (concessional)

Lisa is self-employed and has a strong year.

She puts $10,000 into super from her bank account and claims it as a deduction.

That becomes a concessional contribution, and it reduces her taxable income.

Example 3: Saving boost (non-concessional)

Ben has $30,000 in savings and wants to invest it long-term.

He contributes the money to super and does not claim a tax deduction.

That’s a non-concessional contribution.

Example 4: Mixed strategy (both types)

Nina wants to maximise super before retirement.

She salary sacrifices (concessional), and also adds extra after-tax contributions (non-concessional).

This allows her to use both caps (subject to ATO rules).

Key Takeaways

Concessional contributions are before-tax and may reduce your taxable income

Non-concessional contributions are after-tax and don’t reduce taxable income

Both have caps and eligibility rules, check current ATO limits

Employer contributions count towards the concessional cap

The best strategy depends on your income, goals, and retirement timeline

A tailored plan can help you boost super while staying within the rules

FAQ

1) Are employer super contributions concessional contributions?

Yes. Employer super contributions count as concessional contributions and use part of your concessional cap.

2) Is salary sacrifice concessional or non-concessional?

Salary sacrifice is concessional because it comes from pre-tax salary and counts toward concessional caps.

3) Can I make both concessional and non-concessional contributions in the same year?

Yes, as long as you stay within each cap and meet eligibility rules.

4) Do non-concessional contributions reduce my taxable income?

No. Non-concessional contributions are made from after-tax money and do not reduce taxable income.

5) What happens if I exceed my contribution cap?

You may face additional tax and the ATO may require you to withdraw excess contributions. It’s best to track contributions carefully.

Understanding concessional vs non-concessional contributions is one of the simplest ways to take control of your retirement.Because once you know the difference, you can make smarter decisions and avoid costly mistakes.

Whether you’re trying to:

reduce tax

boost super faster

or plan for retirement,

Choosing the right contribution strategy can make a real difference over time.

Still asking “what if” about your finances?

That’s exactly where clarity begins.

Whether you’re planning ahead, growing wealth, or simply want confidence in your financial decisions, the advisers at What If Advice can help you turn questions into a clear, personalised plan.

👉 Book a free 15-minute strategy session or get in touch today at

whatifadvice.com.au