Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

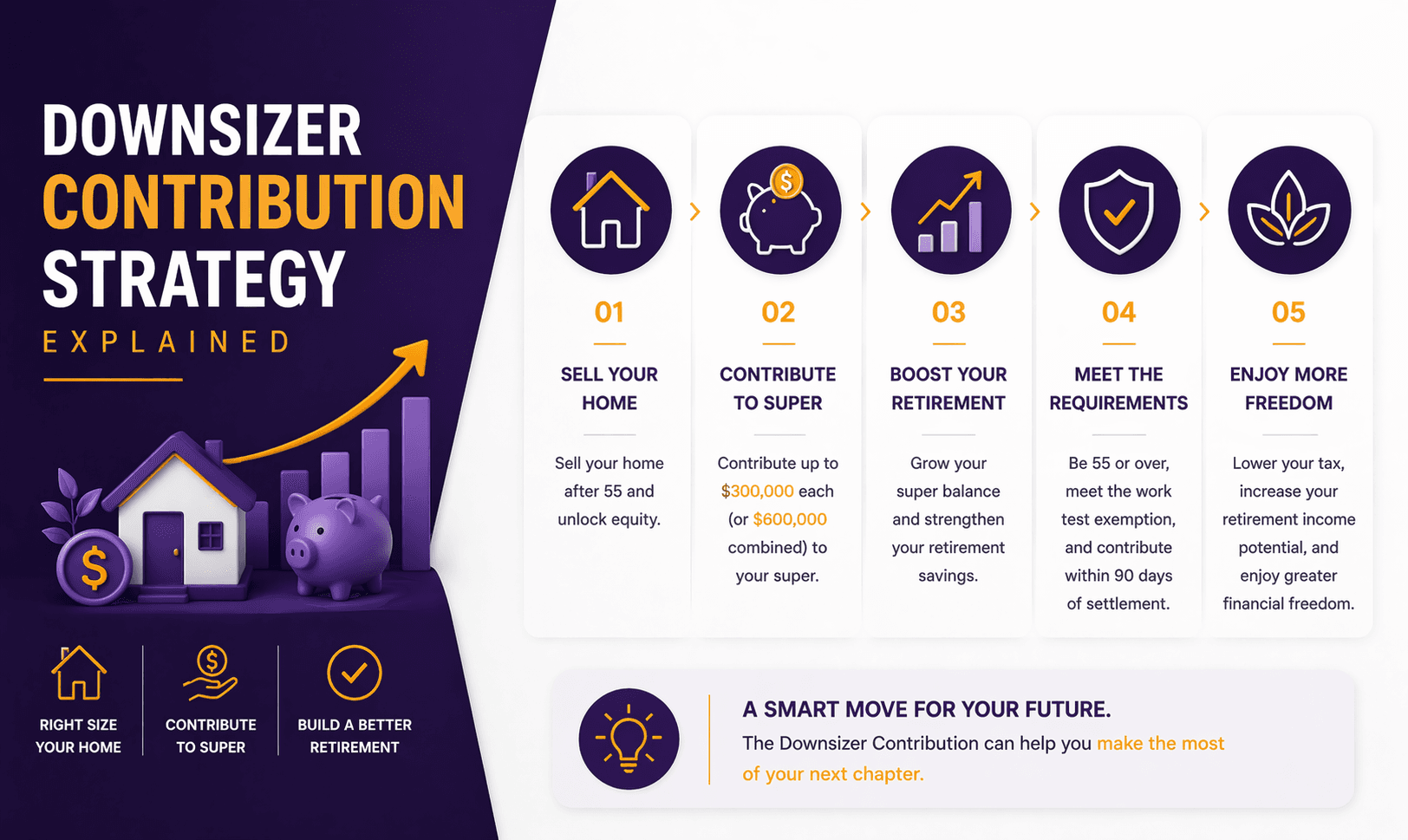

Downsizer Contribution Strategy Explained

For many Australians, the family home is their largest asset.

The downsizer contribution rule allows eligible homeowners to contribute some of the proceeds from selling their home directly into superannuation — even if they are over the usual contribution age limits.

This strategy can significantly boost retirement savings, improve income flexibility and form part of a broader retirement planning strategy.

Here’s how it works.

What Is a Downsizer Contribution?

A downsizer contribution allows eligible individuals to contribute up to $300,000 per person into super from the sale of their home.

For couples, this means up to $600,000 combined may be contributed.

Key features include:

It does not count toward concessional or non-concessional contribution caps.

The work test does not apply.

It can be used even if you already have a high super balance.

This makes it a valuable strategy for Australians approaching or entering retirement.

(All rules subject to current ATO legislation.)

Who Is Eligible?

To make a downsizer contribution, you must generally meet the following conditions:

Be 55 years or older at the time of contribution

Sell a home located in Australia

Have owned the property for at least 10 years

The home must qualify (at least partially) for the main residence CGT exemption

Make the contribution within 90 days of settlement

Both members of a couple may contribute even if only one partner owned the property.

Eligibility rules are subject to current ATO regulations.

How Much Can You Contribute?

The maximum downsizer contribution is:

$300,000 per person

$600,000 for couples

Example:

John and Sarah sell their home for $1.2 million.

They can contribute:

John: $300,000

Sarah: $300,000

Total added to super: $600,000

Importantly, the contribution does not need to match the exact sale proceeds, provided it does not exceed the $300,000 cap per person.

Why Downsizer Contributions Are Powerful

1. Boost Retirement Savings Later in Life

Many Australians reach their 60s with significant home equity but limited super.

Downsizer contributions allow some of that wealth to move into the super system, where earnings may be taxed more favourably.

2. Improve Retirement Income

Moving funds into super allows them to be converted into an account-based pension, which may generate tax-free income after age 60 (subject to current ATO rules).

This can materially improve retirement cash flow.

3. Flexibility Without Standard Contribution Limits

Unlike other super contributions:

The total super balance restriction does not apply.

You can contribute even if your balance exceeds the non-concessional cap limits.

This makes it one of the few ways to add significant funds to super later in life.

Impact on Age Pension Eligibility

The downsizer strategy can affect Age Pension entitlements.

Your principal residence is generally exempt from the Age Pension assets test, but once sale proceeds are contributed to super:

The funds become assessable assets.

Pension eligibility may change under Services Australia rules.

Example:

Before downsizing:

Home value: $1.2 million (exempt asset)

After downsizing:

$600,000 in super pension account (assessable asset)

This could reduce or eliminate Age Pension benefits depending on total assets.

Careful modelling is essential.

Timing Considerations

The downsizer contribution must be made within 90 days of settlement of the property sale.

To complete the contribution correctly:

Notify your super fund using the ATO Downsizer Contribution Form.

Transfer the contribution within the required timeframe.

Ensure the fund processes it as a downsizer contribution.

Missing these steps may result in the contribution being rejected.

Downsizing vs Staying in the Family Home

Downsizing should not be viewed purely as a financial decision.

Other factors include:

Lifestyle changes

Emotional attachment to the home

Proximity to family

Moving costs and stamp duty

For some retirees, downsizing improves both lifestyle and financial flexibility.

For others, staying in the home remains preferable.

Example Scenario

Linda, age 68:

Owns a home worth $1 million

Has $250,000 in super

She sells her home and purchases a smaller property for $600,000.

Remaining equity: $400,000

She contributes $300,000 to super using the downsizer rule.

Her new super balance: $550,000, which can be converted into a retirement income stream.

Common Mistakes

Missing the 90-day contribution deadline

Not submitting the ATO downsizer form

Assuming it improves Age Pension eligibility automatically

Ignoring the impact on Transfer Balance Cap limits

Not modelling retirement income outcomes

Strategic advice before selling can prevent these issues.

FAQs

1. What is the downsizer contribution age limit?

Currently, individuals aged 55 and over may be eligible (subject to current ATO rules).

2. Can both spouses make a downsizer contribution?

Yes. Each partner may contribute up to $300,000 even if only one owned the property.

3. Does the downsizer contribution count toward super caps?

No. It does not count toward concessional or non-concessional contribution limits.

4. Can I make multiple downsizer contributions?

No. The downsizer contribution can generally only be used once per individual.

5. Does it affect the Age Pension?

Yes. Funds contributed to super become assessable assets under Services Australia rules.

6. Do I have to buy another home?

No. Purchasing another property is not required to make the contribution.

Use Your Home Equity to Strengthen Your Retirement Plan

The downsizer contribution can be a powerful strategy — but its impact on tax, super limits and Age Pension eligibility must be carefully assessed.

At What If Advice, we help Australians evaluate downsizing scenarios and integrate property decisions into a comprehensive retirement strategy aligned with current ATO and Services Australia rules.

If you are considering selling your home before or during retirement, strategic advice can ensure the proceeds are used effectively.

Book a retirement planning consultation with What If Advice.

General Advice Disclaimer

This article provides general information only and does not consider your personal objectives, financial situation or needs. Before making financial decisions, consider whether the information is appropriate for your circumstances and seek personal advice from a licensed financial adviser. Superannuation, taxation and Age Pension rules are subject to change under current ATO and Services Australia regulations.