Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

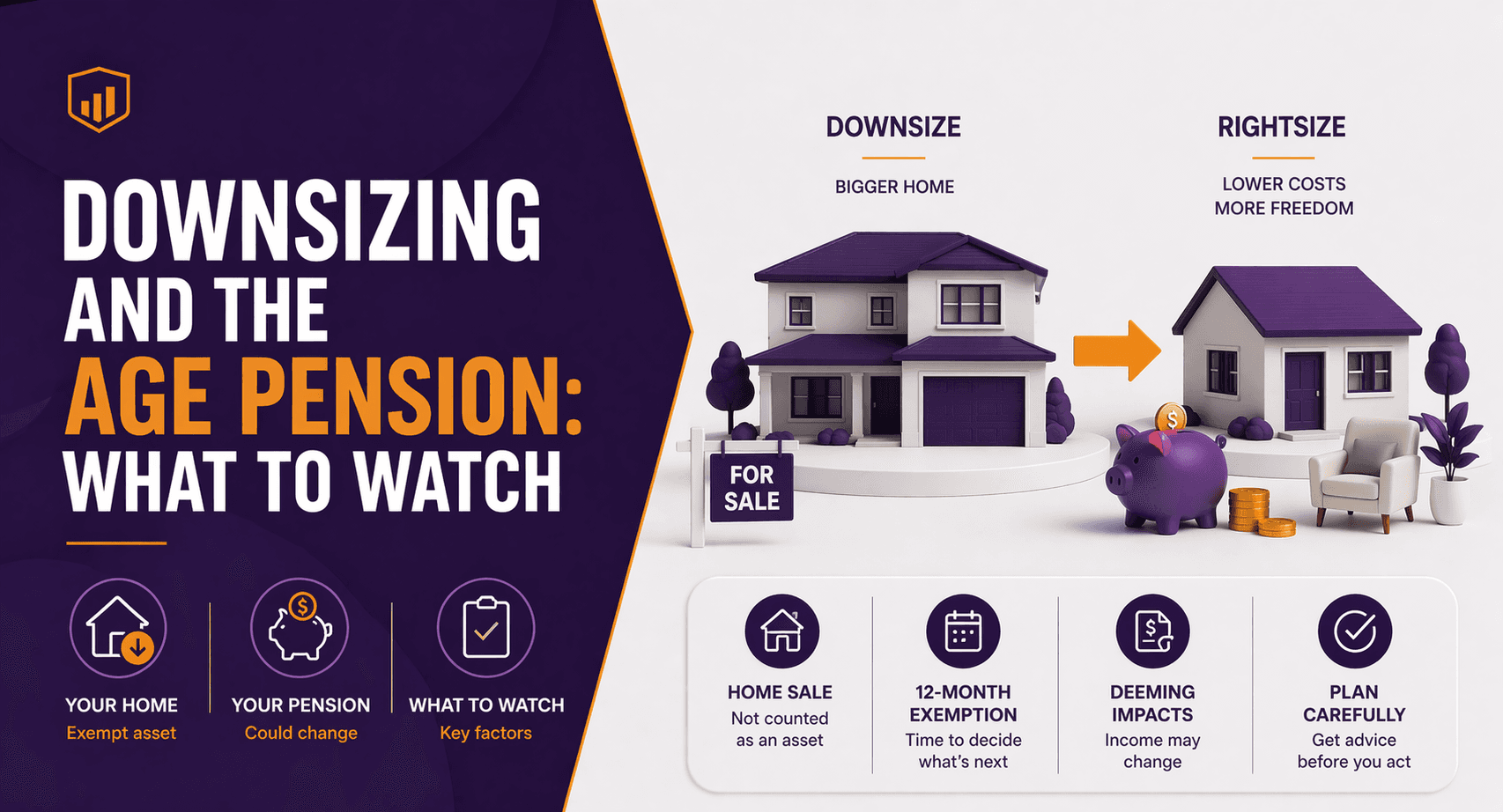

Downsizing and the Age Pension: What to Watch

For many Australians approaching retirement, the family home represents a significant portion of their wealth.

Downsizing to a smaller property can free up capital and reduce living expenses. However, selling your home may also affect your Age Pension eligibility.

This is because while your principal residence is generally exempt from the Age Pension assets test, the proceeds from selling it may not be.

Understanding how downsizing interacts with pension rules can help retirees make more informed decisions.

(All rules subject to current Services Australia regulations.)

How the Age Pension Assets Test Treats Your Home

Under current Age Pension rules:

Your principal residence is generally exempt from the assets test

Other assets are counted toward pension eligibility

This means homeowners may qualify for higher pension payments compared to renters with the same financial assets.

However, the exemption applies only while the home remains your primary residence.

What Happens When You Sell Your Home

When you sell your home, the proceeds may temporarily affect your Age Pension assessment.

There are two possible scenarios.

1. Buying Another Home

If you plan to purchase another principal residence:

The sale proceeds may be temporarily exempt from the assets test for a limited period while you acquire a new property.

During this time, Services Australia may assess the funds under different rules.

The exact treatment depends on timing and intention to purchase another home.

2. Keeping the Remaining Proceeds

If you downsize and retain excess funds after purchasing a smaller home:

These funds typically become assessable financial assets

They may be subject to deeming rules under the income test

This may reduce Age Pension payments.

Example Scenario

Michael and Susan sell their family home for $1.3 million.

They purchase a smaller home for $800,000.

Remaining proceeds: $500,000

Under Age Pension rules:

The new home remains exempt.

The $500,000 becomes an assessable financial asset.

This amount may reduce their Age Pension under the assets and income tests.

The Downsizer Contribution Strategy

Some retirees choose to contribute part of their home sale proceeds to superannuation using the downsizer contribution rule.

Eligible individuals may contribute up to $300,000 per person into super (subject to current ATO rules).

This strategy can:

Boost super balances

Improve retirement income flexibility

Provide tax advantages within the super system

However, once funds are inside super and in pension phase after Age Pension age, they are typically assessable under pension means tests.

Temporary Exemption for Home Sale Proceeds

If you sell your home intending to purchase another property, proceeds may be temporarily exempt from the assets test for a limited period.

During this time:

Funds may still be subject to deeming under the income test.

The exemption period allows retirees to secure a new residence without immediate pension impact.

The specific timeframe and conditions are set by Services Australia.

Downsizing May Still Improve Retirement Income

Even if downsizing reduces Age Pension payments slightly, it may still improve overall financial security.

Benefits may include:

Lower housing costs

Access to home equity

Additional funds for retirement income

Reduced maintenance expenses

The decision should consider both financial and lifestyle factors.

Other Considerations When Downsizing

Before selling a home in retirement, retirees should consider:

Transaction Costs

Costs may include:

Stamp duty

Legal fees

Real estate agent commissions

Moving costs

These expenses can reduce the net financial benefit.

Lifestyle Factors

Downsizing may affect:

Proximity to family

Access to healthcare

Community and social networks

These factors are often just as important as financial outcomes.

Pension and Tax Interaction

The interaction between:

Age Pension rules

Super contributions

Investment income

can influence retirement outcomes.

Common Downsizing Mistakes

Retirees sometimes overlook important pension implications.

Common mistakes include:

Assuming the entire home sale remains exempt

Ignoring deeming rules on retained funds

Not considering transaction costs

Downsizing without reviewing Age Pension eligibility

Planning ahead can help avoid surprises.

FAQs

1. Does selling your home affect the Age Pension?

Yes. While your principal residence is exempt, any remaining sale proceeds may become assessable assets.

2. Is a smaller home still exempt from the assets test?

Yes. Your new principal residence is generally exempt under current Age Pension rules.

3. What happens to leftover money after downsizing?

Funds remaining after purchasing a new home usually become assessable financial assets.

4. Can downsizing increase my Age Pension?

In some cases, but often it may reduce payments if significant assets are released.

5. Can I put downsizing proceeds into super?

Eligible individuals may contribute up to $300,000 per person using the downsizer contribution rule (subject to current ATO regulations).

6. Should I consider pension rules before downsizing?

Yes. Pension eligibility can change depending on how sale proceeds are structured.

Understand How Downsizing Could Affect Your Pension

Downsizing can improve retirement flexibility, but it may also change how your Age Pension is assessed.

At What If Advice, we help Australians model property decisions, super strategies and Age Pension eligibility under current Services Australia rules.

If you are considering selling your home in retirement, structured advice can help you understand the full financial impact.

Book a retirement and pension strategy consultation with What If Advice.

General Advice Disclaimer

This article provides general information only and does not take into account your personal objectives, financial situation or needs. Before making financial decisions, consider whether the information is appropriate to your circumstances and seek personal advice from a licensed financial adviser. Age Pension, taxation and superannuation rules are subject to change under current Services Australia and ATO regulations.