Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

what first home buyers need to know upfront

Buying your first home is exciting, but it’s also a big financial decision with lots of moving parts: deposit size, eligibility for grants and concessions, loan features, and the “hidden” costs that catch many buyers off guard. In Australia, the right approach is usually less about finding a perfect property first and more about getting your numbers and loan strategy clear early.

This guide walks through the practical steps: how deposits work, what government help may be available (subject to current ATO / Services Australia rules and state and territory rules), and which loan options first home buyers commonly consider.

Quick answer: what’s the simplest path to buying your first home?

Most first home buyers do best when they:

Save a deposit that suits their risk level and borrowing capacity

Understand the trade-off between a smaller deposit and paying lenders mortgage insurance (LMI)

Check eligibility for first home buyer grants, stamp duty concessions, and guarantee-style schemes

Choose a loan structure (variable, fixed or split) that matches their cashflow and plans

Build a buffer for rate rises and surprise costs

The “best” mix depends on your income stability, spending habits, timeframe, and whether you’re buying alone or with a partner.

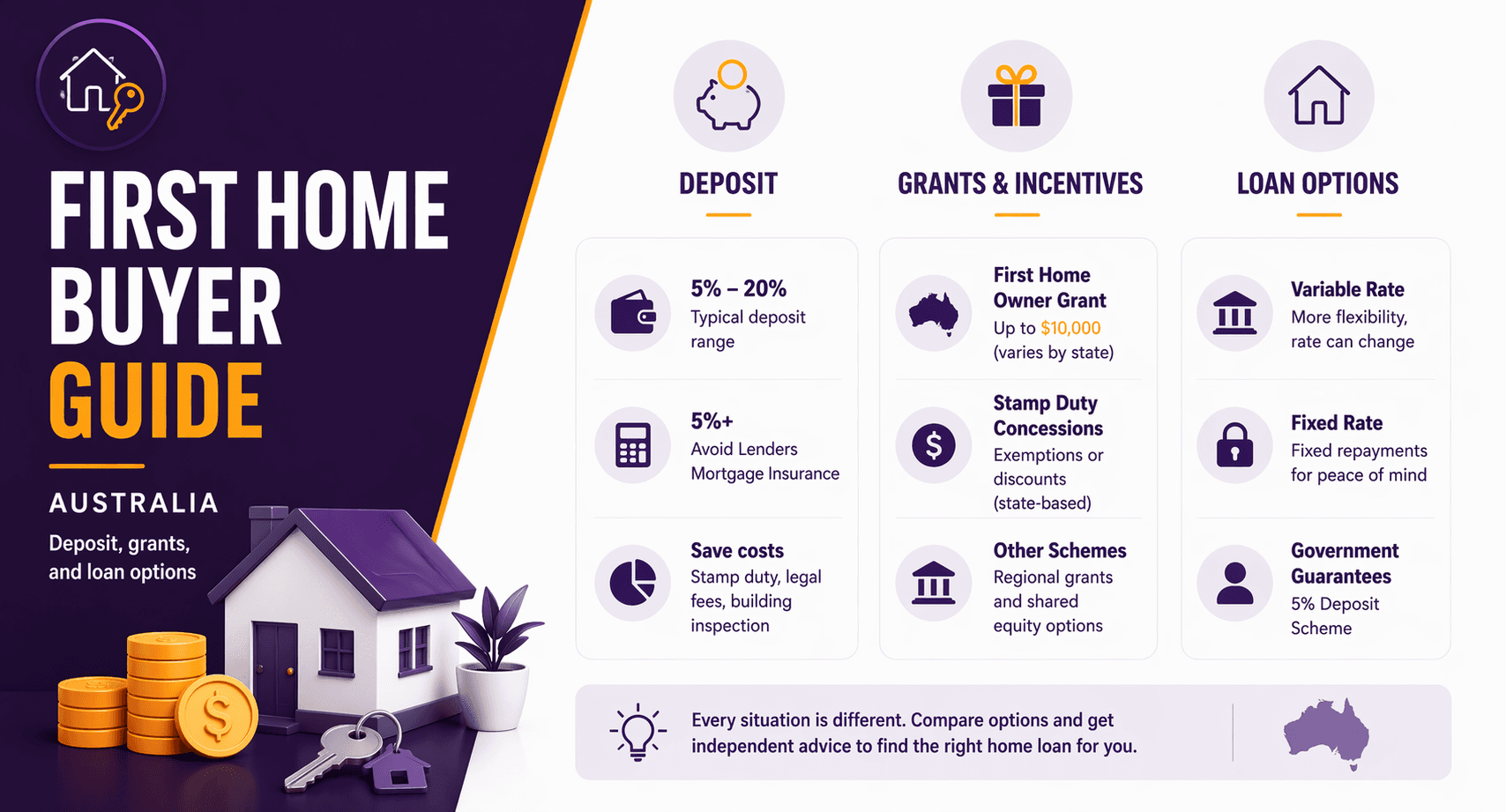

How much deposit do you need as a first home buyer?

There isn’t a single deposit requirement that applies to everyone. In general, the larger your deposit, the more flexibility you tend to have with lender policy, interest rates, and overall borrowing costs.

What is a “good” deposit vs a “minimum” deposit?

A higher deposit can reduce risk for the lender and may improve the deal you’re offered. Some buyers aim for a larger deposit to avoid LMI, while others accept LMI or use an eligible guarantee scheme so they can buy sooner.

What costs should your deposit plan include?

Your deposit is only part of the upfront cash you’ll likely need. A realistic plan often includes:

Stamp duty (or first home buyer concessions/exemptions where eligible)

Conveyancing/solicitor fees

Building and pest inspections (where relevant)

Loan application, valuation or settlement fees (varies by lender)

Moving costs and immediate repairs

A cash buffer for unexpected bills after settlement

What is LMI and when does it apply?

Lenders mortgage insurance (LMI) is an insurance premium that protects the lender (not you) if the loan defaults. It commonly applies when your deposit is smaller and your loan-to-value ratio is higher.

Is paying LMI always a bad idea?

Not always. Paying LMI may be worth considering if:

Property prices are rising faster than your savings rate

You have strong income stability but a shorter savings timeframe

You can still maintain a healthy buffer after purchase

The key is comparing the total cost over time: LMI plus interest versus the cost of waiting longer (including rent and possible price movements).

What first home buyer grants and concessions might you access?

Australia has a mix of state and territory grants, stamp duty concessions, and federal programs designed to help eligible first home buyers. Eligibility and property requirements vary and change over time.

What is the First Home Owner Grant (FHOG)?

The FHOG is generally administered by state and territory governments and is often linked to buying or building a new home. The amount and eligibility criteria vary by location and are subject to current state/territory rules.

Can you get stamp duty relief as a first home buyer?

Many states and territories offer stamp duty concessions or exemptions for eligible first home buyers, sometimes with property value caps and residency requirements. Always check the latest rules in your state or territory.

What is the First Home Super Saver Scheme (FHSSS)?

The FHSSS allows eligible people to save part of a deposit inside superannuation and later withdraw eligible contributions (and associated earnings) for a first home. This is subject to current ATO rules and eligibility criteria.

It can be powerful if used correctly, but it’s important to understand the contribution types, withdrawal process, timing, and how it interacts with your broader super strategy.

What are guarantee-style schemes and how do they help with a smaller deposit?

The Australian Government has supported first home buyer guarantee-style programs in recent years, often aimed at helping eligible buyers purchase with a smaller deposit without paying LMI. These programs typically have eligibility criteria around property type, income, and occupancy, and places may be limited, so confirm details under current program rules.

What loan options do first home buyers usually consider?

The right loan structure is about managing risk and cashflow, not just chasing the lowest advertised rate.

Variable vs fixed: which is better for first home buyers?

Variable rate loans often provide flexibility, including extra repayments and redraw (depending on the lender).

Fixed rate loans provide repayment certainty for a set period, but may limit extra repayments and flexibility.

A common compromise is a split loan, where part is fixed and part is variable.

Offset accounts and redraw: what’s the difference?

Both can help you reduce interest while keeping access to funds, but they work differently:

An offset account is a transaction account linked to your loan; the balance “offsets” interest calculated on the loan.

Redraw lets you access extra repayments you’ve made (subject to lender rules).

Offset accounts can be especially useful if you’re building a buffer or plan to renovate, travel, or take parental leave.

Interest-only vs principal and interest: is interest-only an option?

Most owner-occupiers use principal and interest repayments so the loan balance reduces over time. Interest-only can lower repayments for a period, but it usually comes with higher long-term risk and may have stricter approval criteria.

What is a guarantor (family guarantee) home loan?

Some lenders allow a parent or close family member to guarantee part of the loan using equity in their property. This can reduce the deposit needed or help avoid LMI, but it involves real risk for the guarantor. Everyone should get independent advice before signing.

How do you get “mortgage-ready” before you start house hunting?

Preparation can improve your approval chances and reduce stress.

What do lenders look at when assessing first home buyers?

While policies vary, lenders commonly review:

Income (including casual, overtime and bonuses depending on evidence)

Living expenses and spending patterns

Existing debts and credit limits (credit cards, personal loans, HECS/HELP)

Savings history and genuine savings requirements

Employment stability and probation periods

What steps can you take in the next 30–90 days?

Build a clear budget and set an automated savings plan

Reduce high-interest debts and review credit card limits

Keep records of income and savings (payslips, statements)

Price the “full cost” of owning (rates, strata, insurance, maintenance)

Consider pre-approval to set a realistic price range (noting pre-approval isn’t a guarantee)

FAQs

1. Do first home buyer grants apply to established homes?

It depends on the state or territory and the specific program. Some grants are targeted to new builds, while established homes may be eligible for stamp duty concessions instead. Check current state/territory rules before relying on a benefit.

2. Can I buy with a small deposit without paying LMI?

Possibly, if you meet eligibility for a government-backed guarantee scheme or if a family guarantor arrangement is available through your lender. Both options have conditions and risks, and availability can change under current program and lender rules.

3. Is it better to use the FHSSS or save a deposit in a high-interest account?

It depends on your tax position, timeframe, and discipline with saving. The FHSSS can be effective for eligible buyers, but it has contribution and release rules under current ATO settings and may not suit every situation.

4. What’s the difference between pre-qualification and pre-approval?

Pre-qualification is usually an indicative estimate based on limited information. Pre-approval is a more formal lender assessment (with supporting documents), but it’s still not a final guarantee until you have an accepted contract and the lender completes all checks.

5. How much extra should I budget for buying costs beyond the deposit?

Many first home buyers underestimate upfront and early ownership costs. Budget for stamp duty (if payable), inspections, legal fees, lender fees, moving, insurance, and a cash buffer for repairs and rate rises. The exact amount varies widely, so price these items before you commit.

Focus on the plan, not just the property

A successful first purchase usually comes down to three things: a deposit strategy you can actually stick to, a clear understanding of grants and schemes you may be eligible for, and a loan structure that fits your life (not just today’s rate). If you’re unsure, getting your numbers checked before you start making offers can save you time, money, and stress.

Book a home buyer consult

Want a clear deposit target, an estimate of likely upfront costs, and a loan options shortlist that matches your situation? Book a consult with What If Advice to map out your first home buyer plan and next steps.

General advice disclaimer: This information is general in nature and prepared without taking into account your objectives, financial situation or needs. It is not personal financial advice. Consider whether it’s appropriate for you and check current ATO, state/territory revenue office, lender, and Services Australia rules before acting, and seek professional advice where needed.