Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

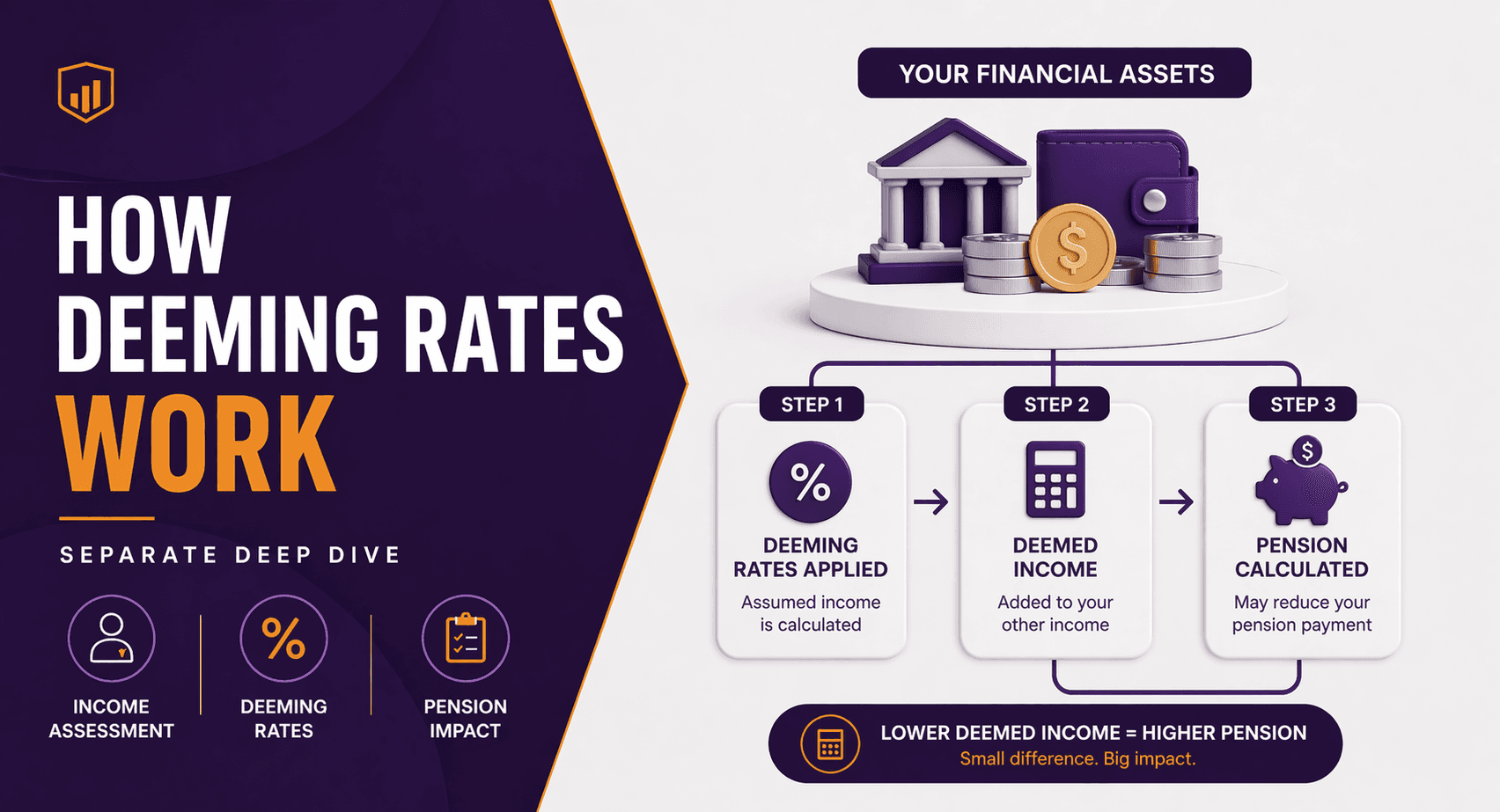

How Deeming Rates Work (Complete Guide for Retirees)

If you receive the Age Pension, your income is assessed using deeming rates.

Instead of looking at the actual income your investments generate, the government assumes your financial assets earn a set rate of return.

This is known as deeming.

The system simplifies income testing but can affect pension payments depending on your assets.

(All rules subject to current Services Australia regulations.)

What Are Deeming Rates?

Deeming rates are assumed rates of return applied to financial assets when calculating Age Pension income.

They apply to assets such as:

Bank accounts

Term deposits

Shares

Managed funds

Superannuation pensions

Some trusts and investment products

The government assumes these assets earn a certain amount of income, regardless of actual earnings.

Why Deeming Exists

Before deeming rules were introduced, pension income tests assessed the actual income from each investment.

This created complexity and opportunities to restructure assets to maximise pension payments.

Deeming simplified the system by applying a standard income assumption to financial assets.

This makes pension assessments easier for both retirees and Services Australia.

Current Deeming Rate Structure

Deeming rates operate on a tiered system.

Financial Assets | Deeming Rate Applied |

Below threshold | Lower deeming rate |

Above threshold | Higher deeming rate |

Thresholds differ for singles and couples.

Example structure (subject to change):

Household Type | Lower Threshold |

Single | ~$60,000 |

Couple (combined) | ~$100,000 |

Assets above these levels are deemed at a higher rate.

Example: How Deeming Works

David is a single Age Pension recipient.

He has $100,000 in financial assets.

Example calculation:

Portion | Deeming Rate |

First $60,000 | Lower rate |

Remaining $40,000 | Higher rate |

The total deemed income is calculated using both rates.

This deemed income is then assessed under the Age Pension income test.

What Counts as Financial Assets?

Several assets fall under deeming rules.

Common examples include:

Cash savings

Bank accounts

Shares

Managed funds

Term deposits

Superannuation pensions after Age Pension age

These assets are grouped together when applying deeming calculations.

What Is Not Subject to Deeming?

Certain assets are assessed differently.

Examples may include:

Investment property (assessed using actual income)

Business income

Employment income

These are typically assessed using different rules under the Age Pension income test.

Why Deeming Matters for Retirees

Deeming affects Age Pension payments in several ways.

1. Low Interest Rates

If bank accounts earn less than the deeming rate, retirees may still be assessed as earning more income than they actually receive.

2. Higher Return Investments

If investments outperform deeming rates, the extra income does not increase pension reductions.

In this case, retirees effectively keep the additional earnings.

3. Investment Decisions

Deeming can influence how retirees structure financial assets within their retirement strategy.

Example Scenario

Linda and Peter are a retired couple with:

$200,000 in savings

No other income

Their financial assets are assessed using deeming rates.

The calculated deemed income is then compared to the Age Pension income-free area to determine whether pension payments reduce.

Strategies to Consider

Understanding deeming can help retirees plan their finances more effectively.

Possible strategies include:

Structuring Financial Assets Carefully

Different asset types are assessed differently under Age Pension rules.

Reviewing Super Pension Balances

Super in pension phase becomes assessable under deeming rules once you reach Age Pension age.

Coordinating Retirement Income

Balancing super withdrawals, investments and Age Pension entitlements may improve long-term income sustainability.

Common Deeming Misconceptions

Retirees often misunderstand deeming.

Common misconceptions include:

Thinking only interest income counts

Assuming actual returns determine pension income tests

Believing deeming only applies to bank accounts

In reality, most financial assets fall under deeming rules.

FAQs

1. What are deeming rates?

Deeming rates are assumed investment returns used by Services Australia to calculate income from financial assets for Age Pension eligibility.

2. Do deeming rates use actual investment income?

No. The government applies assumed income based on deeming rates rather than actual returns.

3. What assets are subject to deeming?

Assets such as savings, shares, managed funds and superannuation pensions are typically subject to deeming.

4. Do deeming rates change?

Yes. Deeming rates and thresholds can change depending on government policy.

5. Does deeming apply before Age Pension age?

Generally, deeming applies when assessing Age Pension eligibility after reaching Age Pension age.

6. Can investment performance affect deeming?

Actual performance does not affect deemed income. The same rate applies regardless of actual returns.

Understand How Deeming Affects Your Pension

Deeming rules can significantly influence how much Age Pension you receive.

At What If Advice, we help Australians understand how financial assets, superannuation pensions and investment income interact with Age Pension rules under current Services Australia regulations.

If you want clarity on how deeming affects your retirement income, professional advice can help you structure assets effectively.

Book an Age Pension strategy consultation with What If Advice.

General Advice Disclaimer

This article provides general information only and does not take into account your personal objectives, financial situation or needs. Before making financial decisions, consider whether the information is appropriate to your circumstances and seek personal advice from a licensed financial adviser. Age Pension, taxation and superannuation rules are subject to change under current Services Australia and ATO regulations.