Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

Retirement is one of those life goals that sounds simple, “stop working and enjoy your time” but the planning behind it can feel confusing.

The most common question Australians ask is:

“How much super do I need to retire comfortably?”

And the honest answer is: it depends on the lifestyle you want, your age, your health, whether you own your home, and how long your money needs to last.

But don’t worry, in this article we’ll break it down clearly so you can get a realistic target and start planning with confidence.

What Does “Comfortable Retirement” Actually Mean?

Before we talk numbers, it helps to understand what “comfortable” means in a real-world sense.

A comfortable retirement usually includes things like:

Owning your home (or minimal rent/mortgage)

Paying bills without stress

Maintaining a car

Going out for meals occasionally

Regular local travel and occasional overseas trips

Private health cover (if desired)

Covering medical and unexpected expenses

Having money for hobbies, family gifts, and lifestyle enjoyment

A modest retirement might be more basic. Essential expenses covered, but fewer luxuries and limited travel.

Why lifestyle matters

If your retirement goal is:

“I just want peace of mind and to cover essentials”

your target will be lower than someone who wants:

“I want to travel every year and live more freely.”

The Big Factors That Decide How Much Super You’ll Need

There are a few core things that affect how big your retirement super balance needs to be.

1) Whether you own your home

This is one of the biggest differences.

If you own your home outright by retirement, you usually need far less than someone who will be renting.

Why? Because rent is often the largest expense in retirement, and it rises with inflation over time.

2) How old you retire

Retiring at 60 vs 67 is a major difference.

If you retire earlier, your super needs to last longer, and you may not be eligible for the Age Pension yet.

3) Your spending habits

Some people live comfortably on $50,000 per year.

Others need $80,000+ per year to feel comfortable.

Retirement planning is really about matching your super to your desired yearly income.

4) Investment returns and inflation

Your super continues to grow (or fall) depending on how it’s invested.

At the same time, inflation slowly increases costs over time.

This is why a good retirement plan includes:

realistic investment assumptions

a buffer

and flexible withdrawal strategies.

5) Your health and longevity

Many Australians now spend 20–30 years in retirement.

That means your super needs to support:

general living costs

medical expenses

aged care needs (later in life).

A Simple Way to Estimate Your Retirement Super Target

Here’s a helpful starting formula:

Step 1: Decide how much income you want each year

For example:

$50,000/year might feel modest-to-comfortable for some

$70,000/year might suit a more comfortable lifestyle

$90,000+/year may suit frequent travel or higher living standards

(These are just examples, your target should be personalized.)

Step 2: Estimate how long you’ll need income

A common planning approach is to assume retirement lasts until around age 90 (or beyond).

Step 3: Work out whether you’ll get the Age Pension

Many Australians receive some form of Age Pension depending on eligibility and assets. This can reduce the super required.

To check eligibility, you can use:

Services Australia rules (income and asset tests)

Age Pension calculators

adviser modelling tools.

Step 4: Estimate how much super provides per year

A common retirement planning guideline is the 4% rule (not perfect, but useful as a starting point).

It means you might withdraw about 4% of your retirement balance per year to reduce the chance of running out.

Example:

$500,000 super ~$20,000/year income

$800,000 super ~$32,000/year income

$1,000,000 super ~$40,000/year income

This is just a guide; actual outcomes depend on investment returns, inflation, and your withdrawal pattern.

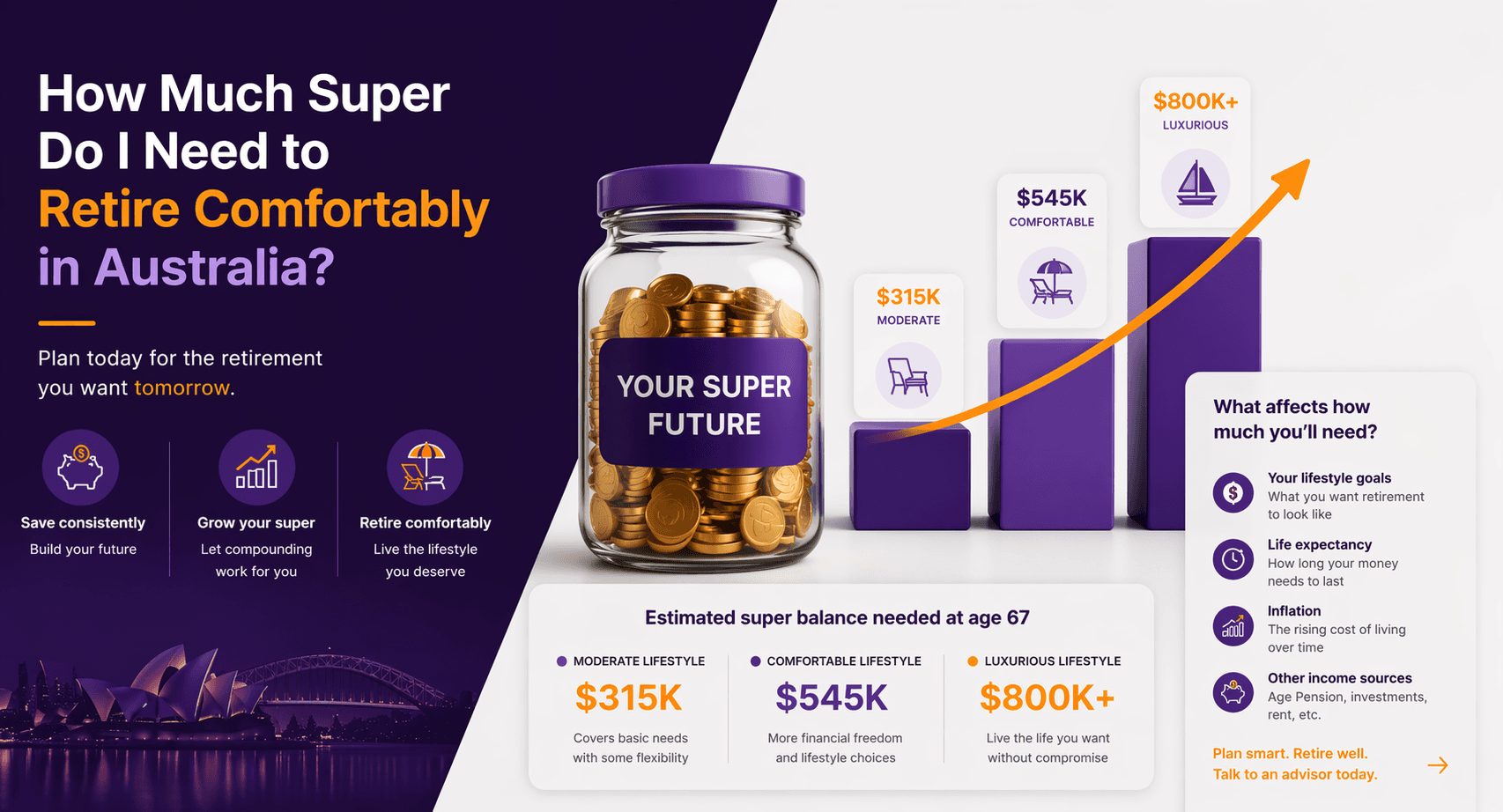

So… How Much Super Do You Need to Retire Comfortably?

There’s no “one size fits all”, but these rough balance ranges can help frame your expectations:

If you own your home outright

Many Australians aiming for a comfortable retirement target somewhere in the range of:

$500,000 to $800,000 for a couple

$400,000 to $650,000 for a single person

If you expect to rent in retirement

A higher target may be needed because ongoing rent can significantly impact your retirement income:

$800,000+ for a couple

$650,000+ for a single person

Note: These ranges are general estimates only. For accurate planning, it’s best to use personalised modelling and check current rules around super access, Age Pension, and cost of living.

Why Your “Super Number” Might Be Smaller Than You Think

Many people assume they need over $1 million to retire, and while that might be true for some, it’s not always the case.

Here’s why:

1) The Age Pension may support you

Even with a decent super balance, you may still be eligible for a part Age Pension depending on assets and income tests.

That extra income can reduce the super you need to fund your lifestyle.

2) You may spend less as you get older

Many people naturally reduce spending later in retirement.

Travel slows down, lifestyle costs drop, and expenses become more predictable.

3) Your home is often your biggest asset

If you own a home outright, you have stability and optional strategies later, such as downsizing (if it suits your situation).

How Much Super Should You Have at Different Ages?

A helpful way to check if you’re “on track” is to compare your balance at different life stages.

While it varies widely, here are benchmark-style questions you can ask:

At age 30

Are you contributing regularly?

Are you invested appropriately for long-term growth?

Do you have multiple super accounts losing fees?

At age 40

Are you building momentum?

Are you adding extra contributions if affordable?

Do you have any insurance inside super that suits your needs?

At age 50

Have you done a retirement projection?

Are you salary sacrificing or using catch-up contributions (if eligible)?

Do you know your likely retirement age?

At age 60+

Do you know your retirement income strategy?

Do you understand transition-to-retirement options?

Have you planned around tax-effective withdrawals?

Ways to Boost Your Super (Without Making Life Miserable)

You don’t need to drastically change your lifestyle to improve your retirement outcome. Even small, consistent moves can make a big difference.

1) Consolidate your super accounts

Many Australians have multiple super accounts without realising.

Consolidating can help reduce:

duplicate fees

duplicate insurance premiums

admin costs.

2) Review your investment option

Your super investment choice influences long-term performance.

For example:

a conservative option may be lower risk but grow slower

a growth option may fluctuate but potentially grow more over time.

The “best” option depends on your age, time horizon, and risk tolerance.

3) Consider extra contributions

Depending on your circumstances, extra contributions could include:

salary sacrifice (pre-tax contributions)

personal after-tax contributions

spouse contributions (where eligible)

Always check current ATO contribution caps and eligibility.

4) Track your super performance

Most people never check whether their super is performing well compared to alternatives.

A simple annual review can help ensure you’re not falling behind.

5) Work a little longer (if possible)

This is underrated.

Working even an extra 1–3 years can:

reduce the years your super needs to last

increase contributions

allow the balance to grow longer

potentially improve Age Pension alignment.

Retirement Planning Example (Simple Scenario)

Let’s say:

You’re 45 years old

You have $190,000 in super

You want to retire at 65

You own your home

You want around $60,000/year retirement income combined (as a couple)

A realistic retirement plan might include:

projecting super growth using conservative assumptions

testing different retirement ages (65 vs 67)

estimating Age Pension eligibility

designing a drawdown strategy

checking whether extra contributions are needed.

This is exactly what a retirement modelling session can provide, a clear plan instead of guesswork.

Key Takeaways

“Comfortable retirement” depends on lifestyle and housing costs

Owning your home usually means you need less super

Retirement length matters. Many people live 20–30 years post-work

Super isn’t the only income source. Age Pension may support you

Small improvements (consolidation + contributions + investment review) can have a big impact

A personalised plan is the best way to know your number confidently

FAQ

1) What is a “comfortable” retirement in Australia?

A comfortable retirement generally means covering bills easily, enjoying lifestyle spending, and having flexibility for travel and unexpected costs.

2) Is $500,000 super enough to retire?

It can be; especially if you own your home and are eligible for some Age Pension. It depends on your spending and retirement age.

3) Do I need $1 million in super to retire comfortably?

Not always. Some people may need it for higher spending or renting, but many retirees can be comfortable with less depending on pension eligibility and lifestyle.

4) Can I rely on the Age Pension?

You may be eligible depending on your assets and income. Rules change, so always check current Services Australia rules and consider planning for a mix of super + pension.

5) What’s the best way to find my retirement number?

A retirement modelling session with an adviser is the most reliable way, because it accounts for your goals, spending, pension eligibility, and super strategy.

Working out how much super you need to retire comfortably can feel overwhelming, but once you break it down into lifestyle, housing, retirement age, and expected income, it becomes much clearer.

The key is to stop guessing and get a plan that shows:

your likely retirement balance

your estimated retirement income

your gap (if any)

and the steps to close it.

Want a clear retirement plan (not just a guess)?

If you’re thinking seriously about retirement, we can help you model your super and create a practical strategy to reach your goals.

Book a Retirement & Super Workshop with What If Advice and walk away with a clear roadmap for your next steps.

General Advice Disclaimer

This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions.