Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

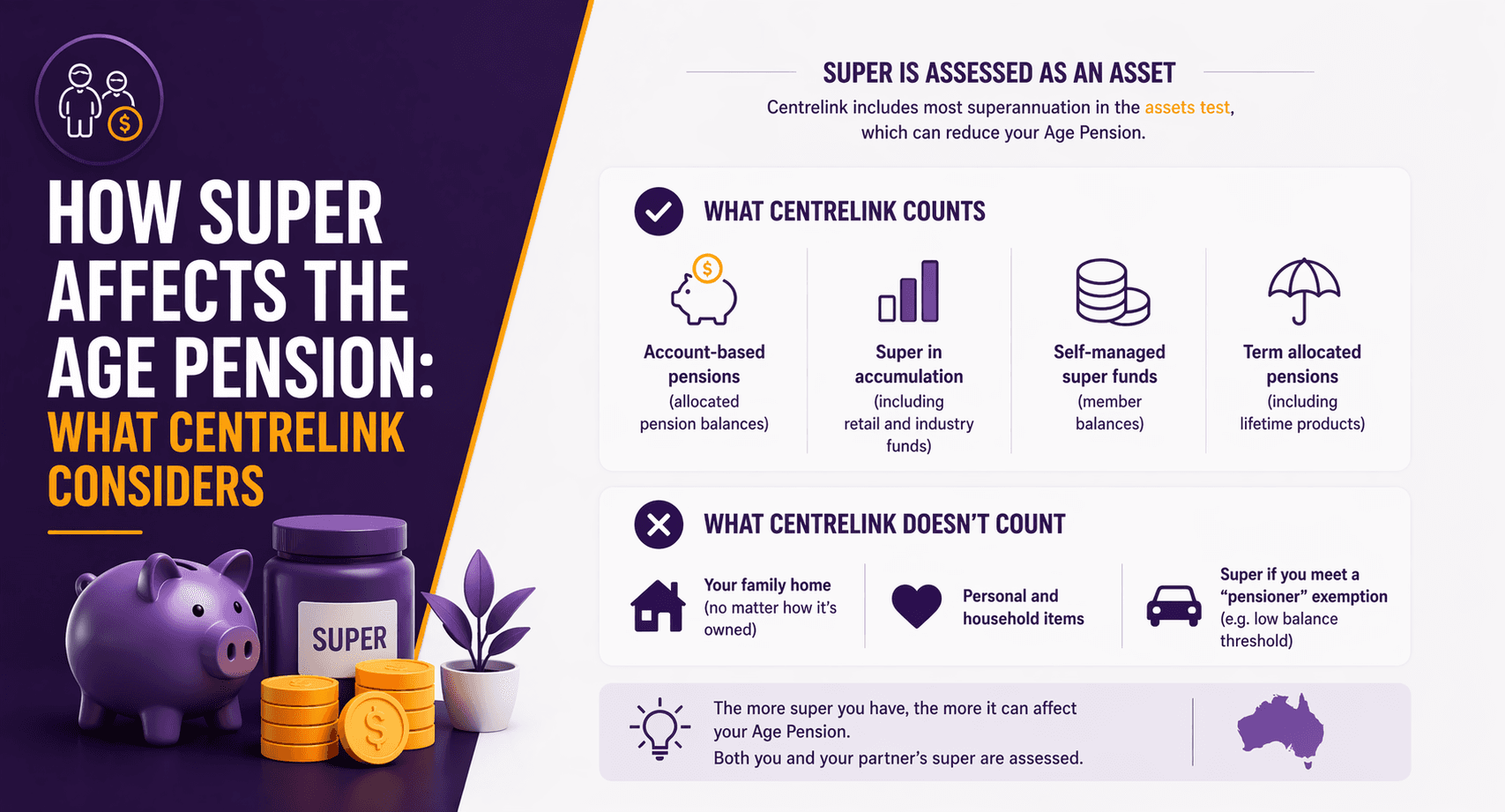

How super affects the Age Pension: what Centrelink considers

Many Australians assume superannuation and the Age Pension are completely separate. In reality, Centrelink (Services Australia) looks closely at your super when applying the Age Pension assets and income tests. The tricky part is that the way super is counted can change depending on your age, whether you’ve reached Age Pension age, and whether your super is still in accumulation or has started paying you an income.

Understanding the basics can help you avoid surprises, plan your drawdown strategy, and feel more confident about what may happen to your Age Pension entitlement. The information below is general and subject to current Services Australia rules.

Quick answer: does super count for the Age Pension?

Yes, super can count, but how it’s assessed depends on your circumstances.

If you’re under Age Pension age, super in accumulation is generally not counted for the Age Pension (because you can’t claim the Age Pension yet). If you’re on a different Centrelink payment, rules may differ.

Once you reach Age Pension age, most super interests are assessed under the assets test and income test, usually either by deeming (for certain income streams) or by assessing income payments.

Because Centrelink applies both tests, your Age Pension rate is generally based on the test that produces the lower payment (subject to current rules).

What does Centrelink actually assess?

Centrelink assesses your financial position under two main lenses:

Assets test: what you own (including eligible super interests)

Income test: what income you receive (including income deemed from certain financial assets)

Your super may be assessed differently depending on whether it is:

Super in accumulation (not started as an income stream)

An account-based pension (a common retirement income stream)

Other income streams (some may be treated differently under Centrelink rules)

Does super in accumulation count once you reach Age Pension age?

Generally, yes. Once you reach Age Pension age, your super in accumulation is typically treated as an assessable asset, even if you haven’t started drawing it. That can reduce your Age Pension under the assets test and can also affect the income test if it’s treated as a financial asset subject to deeming.

Practical implication: delaying the start of a pension payment doesn’t necessarily keep your super “off Centrelink’s radar” once you’re Age Pension age.

How is an account-based pension assessed?

Many retirees start an account-based pension (also called an allocated pension) from super. Centrelink usually assesses this in two ways:

Asset value: the account balance is generally counted under the assets test.

Income: for many account-based pensions, Centrelink applies deeming rules (subject to current Services Australia rules and the specific commencement date and product type).

That means Centrelink may not look at what you actually withdraw each fortnight; instead it may “deem” a notional amount of income from the balance. In some cases, different income assessment methods can apply (for example, certain older or specific income streams).

What is deeming and why does it matter?

Deeming is Centrelink’s way of estimating income from certain financial assets, including bank accounts and many super income streams. Rather than tracking actual earnings, Centrelink assumes your money earns a set rate.

Why this matters:

Investment returns going up or down doesn’t necessarily change the deemed income immediately.

Large changes to your super balance (rollovers, withdrawals, market movements) can change your assessable assets and therefore your deeming assessment.

The deemed income can affect your Age Pension under the income test.

Deeming rates are set by the government and can change, so always check the latest settings (subject to current Services Australia rules).

Is your age the key factor?

Age is a major pivot point.

What happens before you reach Pension age?

Before Pension age, super is often treated differently across Centrelink payments. For the Age Pension specifically, you generally can’t claim it until you reach Age Pension age (subject to current rules). If you are receiving another payment, the way super is counted may vary depending on payment type and whether the money is accessible.

What happens once you reach Pension age?

Once you reach Age Pension age, Centrelink will typically assess:

Your super balance (if still in accumulation)

Your super income stream balance (if you’ve commenced a pension)

Any withdrawals you take, including lump sums, which can change what’s assessable (for example, if moved to a bank account or used to buy assets)

Do withdrawals from super affect the Age Pension?

Withdrawals can affect your Age Pension, but usually indirectly.

A lump sum withdrawal may not be assessed as “income” in the same way as wages, but it can change your assessable assets depending on what you do with it.

If you withdraw and leave it in cash, it remains an assessable financial asset.

If you use it for home renovations on your principal residence, the home is generally treated differently under Centrelink rules (subject to current Services Australia rules).

If you gift money or transfer value for less than it’s worth, gifting rules may apply.

The key is that Centrelink generally assesses what your money becomes, not just where it came from.

How does your partner’s super affect your Age Pension?

Age Pension assessments for couples can be complex because Centrelink looks at combined circumstances in many cases.

Common scenarios:

If one partner is over Age Pension age and the other is under, Centrelink may assess each partner’s accessible assets differently (subject to current Services Australia rules).

Super held by the partner who is under Age Pension age may be treated differently than super held by the partner who is over.

This is an area where getting help to understand the interaction can be valuable.

What reporting and paperwork should you expect?

To apply for the Age Pension, you’ll usually need to provide information about:

Super fund details and balances

Income stream details (product type, start date, current balance)

Bank accounts and other investments

Property and other assets

Tips to reduce delays:

Keep recent statements handy.

If you start or stop an income stream, notify Centrelink promptly.

Check that your super is correctly categorised (accumulation vs pension).

FAQs

1. Does Centrelink count super if I’m still working?

If you’re at or over Age Pension age, Centrelink can still assess your super under the assets and income tests, even if you’re working (subject to current Services Australia rules). Your employment income may also be assessed separately.

2. Is super in my spouse’s name assessed for my Age Pension?

Centrelink often considers the combined circumstances of a couple. However, super can be treated differently depending on whether each person has reached Age Pension age and whether the super is accessible (subject to current Services Australia rules).

3. If I start an account-based pension, will my Age Pension drop?

It might, depending on your total assets and deemed income. Starting a pension changes how your super is structured, but Centrelink usually still counts the balance under the assets test and may apply deeming under the income test (subject to current Services Australia rules).

4. Are lump sums from super counted as income by Centrelink?

A lump sum withdrawal may not be treated like regular employment income, but it can affect your Age Pension by changing your assessable assets (for example, cash in the bank or other purchases). Gifting rules can also apply (subject to current Services Australia rules).

5. Can I rearrange my super to get a higher Age Pension?

Some strategies may improve outcomes, but Centrelink’s rules are detailed and anti-avoidance provisions can apply. It’s important to understand the consequences across both tests and ensure any decisions suit your broader retirement goals.

Superannuation can materially affect the Age Pension because Centrelink generally assesses super interests once you reach Age Pension age, whether your super is still in accumulation or paying an income stream. The main levers are the assets test and income test (including deeming), and your entitlement can change if you withdraw, rollover, gift, or significantly change your balances.

If you’re approaching Age Pension age, it’s worth mapping out how your super structure and drawdown plans may interact with Centrelink, so you can make informed decisions and avoid last-minute surprises.

Want help making sense of super and Centrelink together?

Join a What If Advice retirement workshop to learn how Age Pension assessments typically work, what information Centrelink considers, and what to prepare before you apply.

General advice disclaimer

This information is general in nature and prepared without taking into account your objectives, financial situation or needs. It is not personal financial advice. Rules and eligibility can change and assessments are subject to current ATO and Services Australia rules. Consider your circumstances and seek advice before acting.