Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

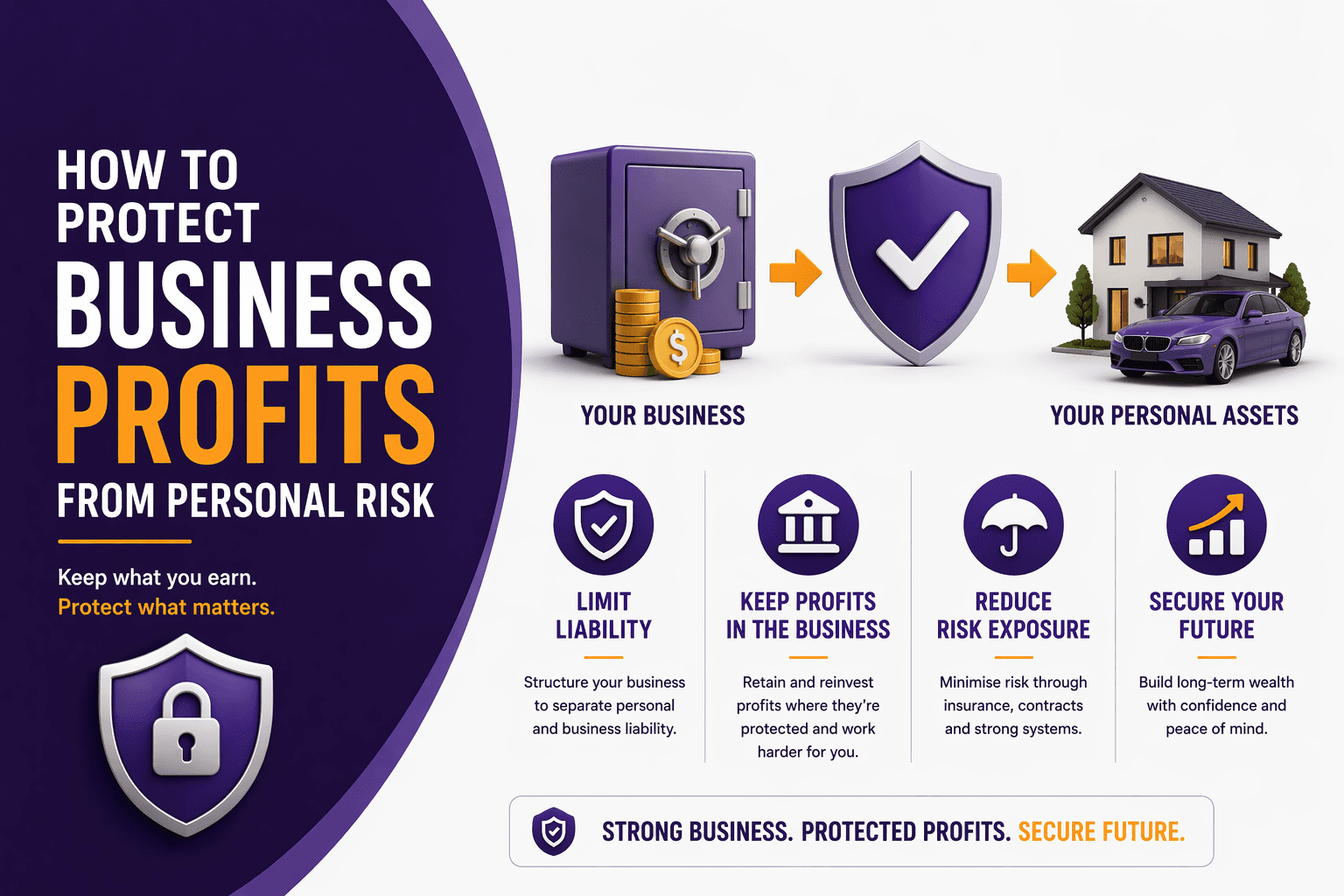

How to Protect Business Profits From Personal Risk (Australia)

If your business is making money but everything is tied to you personally, you don’t really have protection — you have exposure.

And it only takes one:

Lawsuit

Business failure

Personal liability issue

…to wipe out what you’ve built.

Protecting business profits isn’t complicated, but it does require structure, discipline, and planning.

What Is “Personal Risk” for Business Owners?

Personal risk includes anything that could impact you financially outside normal operations:

Legal claims

Business debts

Director liability

Personal guarantees

Divorce or relationship breakdown

Bankruptcy

If your business and personal finances are not properly separated:

These risks can flow directly into your wealth.

Why Structure Matters More Than Income

Many business owners focus on:

Making more money

But ignore:

Where that money sits

Who legally owns it

Reality:

Structure determines protection, not income level.

Strategy 1: Use the Right Business Structure

Sole Trader (High Risk)

No separation between you and the business

Unlimited personal liability

If something goes wrong, your personal assets are exposed.

Company (Better Protection)

Separate legal entity

Limited liability (in most cases)

Business risks are generally contained within the company

Trust Structures (Strategic Protection)

Assets held by a trustee

Beneficiaries do not legally own assets

Adds flexibility and protection when structured correctly

Strategy 2: Separate Business and Personal Assets

One of the most common mistakes:

Mixing everything together

You should:

Keep business income in business structures

Avoid holding significant wealth personally

Separate bank accounts and ownership

Strategy 3: Retain Profits Strategically

Instead of:

Taking all profits personally

Consider:

Retaining profits within a company

Benefits:

Lower tax environment

Reduced exposure to personal liabilities

Strategy 4: Use Holding Structures

A common approach:

Trading entity → runs the business

Separate entity → holds assets

Example:

Company A = trading business

Company B or trust = holds investments

If the trading business is sued:

Asset-holding entity is insulated

Strategy 5: Be Careful With Personal Guarantees

Banks and lenders often require:

Personal guarantees

This can:

Override your company protection

You’re personally liable regardless of structure

Strategy:

Limit guarantees where possible

Understand exposure before signing

Strategy 6: Manage Director Risk

As a director, you can still be personally liable for:

Insolvent trading

Unpaid super

Certain tax obligations

Protection includes:

Staying compliant

Monitoring cash flow

Seeking advice early

Strategy 7: Use Insurance as a Backup Layer

Structure is the first line of defence.

Insurance is the backup.

Types to consider:

Public liability

Professional indemnity

Key person insurance

Example Scenario

Unprotected Structure

Sole trader

Profits held personally

No separation

Outcome:

Legal issue = personal assets at risk

Protected Structure

Business operated through company

Profits retained and structured

Assets held separately

Outcome:

Risk contained

Personal wealth protected

Same business. Very different exposure.

Common Mistakes

1. Staying a Sole Trader Too Long

Simple early, risky later.

2. Treating Company Money as Personal Money

Breaks protection and creates tax issues.

3. No Asset Separation

Everything exposed in one place.

4. Ignoring Legal Advice

Structure isn’t just tax, it’s legal protection.

5. Assuming “It Won’t Happen to Me”

It eventually happens to someone.

Strategic Insight: Protection Is About Layers

No single strategy protects you fully.

You need:

Legal structure

Financial separation

Tax planning

Insurance

Think of it as a system, not a single fix.

When Should You Get Advice?

You should seek advice if:

Your business is generating consistent profits

You’re exposed to liability

You’re growing or hiring

You’re unsure about your structure

Because:

The best time to protect your assets is before something goes wrong.

FAQs

1. Can a company fully protect my personal assets?

Not completely. It provides limited liability, but personal guarantees and director obligations still apply.

2. Is a trust better than a company for asset protection?

They serve different purposes. Often used together for effective structuring.

3. What is the biggest risk for business owners?

Mixing personal and business finances.

4. Should I keep profits in the company?

In many cases, yes. But it depends on your overall strategy.

5. Are personal guarantees risky?

Yes. They can expose your personal assets even if you use a company.

6. When should I change my structure?

Usually when profits grow or risk increases.

7. What is the most common mistake?

Ignoring asset protection until it’s too late.

Is Your Business Actually Protecting You or Exposing You?

Making money is one thing. Protecting it is another.

At What If Advice, we help business owners:

Structure their business for protection

Separate personal and business risk

Build long-term, secure wealth

Book a strategy session to make sure what you’re building is actually protected.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional advice. Legal and taxation rules, including director obligations and asset protection structures, are subject to change.