Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

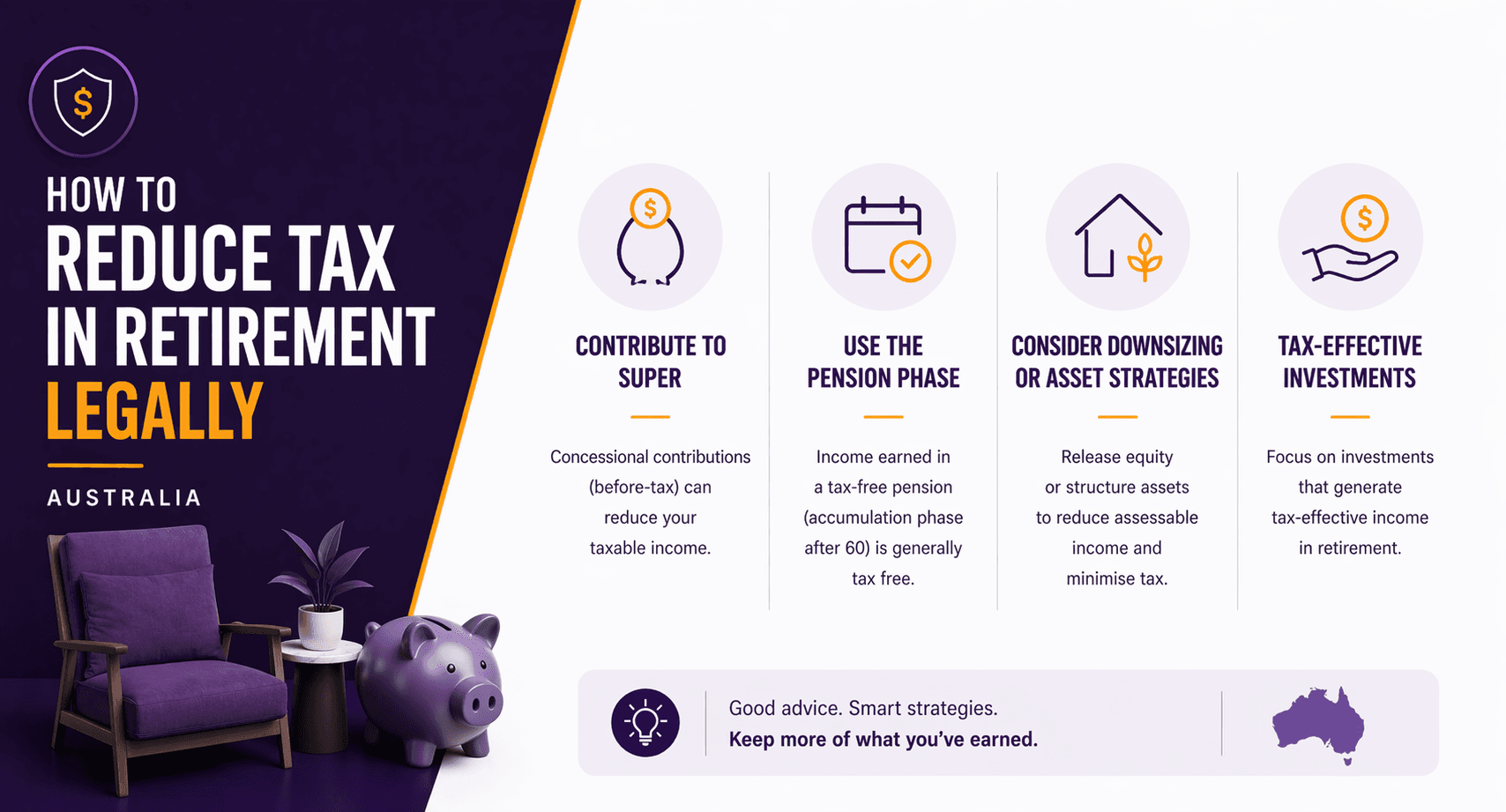

Retirement often comes with a welcome change: you may control when and where your income comes from. That flexibility can also create legal opportunities to reduce tax, without complicated schemes.

In Australia, the big lever is the mix between taxable income (like some interest, dividends, rent and employment income) and concessionally taxed income (often via superannuation, depending on your age and the type of payment). The best approach is usually a simple one: structure your accounts and withdrawals so you’re not paying more tax than you need to, while still meeting your spending needs.

Quick answer: what are the main legal ways to reduce tax in retirement?

For many retirees, the most effective legal tax reducers are:

Using superannuation income streams (for example, an account-based pension) where eligible, subject to current ATO rules

Managing withdrawals so you don’t accidentally push yourself into a higher marginal tax bracket

Splitting income across two people (where appropriate) to use both partners’ tax-free thresholds and offsets

Being deliberate about investment structures (super vs personal names vs joint vs trust/company, where relevant)

Timing capital gains and deductible expenses to smooth taxable income across years

What works best depends on your age, super balance, other assets, and whether you’re aiming to qualify for (or keep) Centrelink payments.

What income is actually taxed in retirement?

Retirees can have several income “buckets”, each with different tax treatment (subject to current ATO rules):

Superannuation withdrawals: Lump sums and pensions can be taxed differently depending on age, components, and the fund

Personal investment income: Bank interest, dividends, managed funds distributions

Rental income: Rent received minus deductible property costs

Capital gains: Selling shares, managed funds or property outside super

Employment or consulting income: Common for part-time work in early retirement

A good plan aims to maximise after-tax income while keeping enough flexibility for unexpected expenses.

How can superannuation help reduce tax after you stop work?

Super is designed to be tax-effective. Two common strategies are:

Can an account-based pension reduce tax?

Starting an account-based pension (also called an allocated pension) can reduce tax because earnings on investments supporting the pension may be taxed more favourably than earnings in the accumulation phase, subject to current ATO rules.

Key points:

You generally choose an annual pension payment within required ranges (subject to current rules)

Payments can be made regularly or as ad-hoc withdrawals

It may help you better control taxable income compared with drawing everything from personal accounts

This is not automatic for everyone; eligibility and outcomes depend on your situation and how your super is structured.

Should you consider a Transition to Retirement (TTR) strategy?

If you’re still working (even part-time) and have reached preservation age, a Transition to Retirement strategy may allow you to draw income from super while making contributions, potentially improving tax efficiency (subject to current ATO rules).

A TTR strategy can be useful when:

You want to reduce work hours without reducing take-home pay too much

You’re trying to build super while smoothing your taxable income

Because contribution rules and TTR conditions can be technical, it’s worth getting advice before implementing.

How do you keep taxable income low without running out of money?

Tax minimisation shouldn’t create cashflow stress. The practical skill is withdrawal planning.

What order should you draw income from?

Common retirement “drawdown order” ideas include:

Use cash and personal investments to cover short-term spending while managing capital gains

Use super pension payments to meet regular income needs

Consider lump sum withdrawals strategically for large one-off expenses (car, renovations), subject to current rules

The best order depends on your age, super tax components, and whether you’re trying to keep taxable income below certain thresholds.

How do you avoid jumping into a higher tax bracket?

A simple technique is to model your expected taxable income and then decide whether to:

Take an extra withdrawal this year or delay it until the next financial year

Realise capital gains gradually rather than in one hit

Hold more of your defensive assets (cash/term deposits) in the most tax-effective place for your situation

Small timing decisions can make a meaningful difference.

What tax offsets and concessions might retirees be eligible for?

Retirees may qualify for offsets that reduce tax payable, subject to current ATO rules. One commonly discussed example is the Seniors and Pensioners Tax Offset (SAPTO).

Potential benefits of offsets and concessions include:

Paying less tax even if your assessable income stays the same

In some cases, reducing or eliminating tax payable if you’re on lower retirement incomes

Because eligibility can depend on your income sources and residency status, it’s important to check your position each year.

How can couples reduce tax in retirement?

For couples, tax planning often improves when you look at your finances as a combined household.

Can splitting income between spouses reduce tax?

Potential opportunities include:

Holding some investments in the name of the lower-income spouse (where appropriate)

Using both partners’ super accounts strategically

Balancing pension payments and personal income to use both tax-free thresholds and offsets

These steps need to be weighed against non-tax considerations like estate planning, access to money, and investment risk.

Does Centrelink change the best tax strategy?

It can. Some choices that reduce tax may affect Age Pension eligibility under the income and assets tests (subject to current Services Australia rules). For example:

Moving assets between super and personal names may change how they’re assessed

Different income streams can be treated differently under Centrelink rules

Ideally, your plan considers tax and Centrelink together, not in isolation.

What investment choices can reduce tax in retirement?

Investment tax outcomes vary by structure and asset type.

Are franked dividends helpful for retirees?

Australian shares paying franked dividends may provide franking credits, which can reduce tax payable (subject to current ATO rules). The value depends on your taxable income and whether you can use the credits.

Franking shouldn’t be the only reason to invest; diversification and risk still matter.

When should you sell assets to manage capital gains tax (CGT)?

If you’re selling investments outside super, CGT can be a major driver of tax.

Practical CGT management ideas include:

Spreading sales over multiple financial years

Pairing gains with losses where appropriate

Planning sales around years where your other taxable income is lower

Always keep records of purchase prices, reinvested distributions and selling costs.

FAQs

1. Is super tax-free after 60 in Australia?

Often, payments from super can be tax-free after age 60, depending on the type of payment, the fund, and your super components, subject to current ATO rules. It’s still important to confirm how your super is taxed before you set up a drawdown plan.

2. Do I pay tax on an account-based pension?

It depends on your age and the taxable/tax-free components of your super, subject to current ATO rules. Even where pension payments are tax-free, other income (like rent or interest) may still create a tax bill.

3. Can I reduce tax by withdrawing a lump sum from super?

A lump sum can sometimes be tax-effective for specific goals, but it can also be inefficient if it creates unnecessary taxable income or reduces long-term tax advantages inside super, subject to current ATO rules. The “right” answer depends on what the money is for and your future income needs.

4. Will reducing my taxable income increase my Age Pension?

Possibly, but not always. The Age Pension is assessed under income and assets tests, and strategies that reduce tax can change how income or assets are counted, subject to current Services Australia rules. Consider modelling both outcomes together.

5. What’s the biggest mistake retirees make with tax?

Not planning withdrawals. Many retirees focus only on investment returns and ignore where the income comes from, leading to avoidable tax and missed offsets. A simple annual plan (and review) can prevent nasty surprises at tax time.

Conclusion: focus on structure, timing and withdrawal planning

Reducing tax in retirement legally is usually about three things: using super effectively, timing income and asset sales, and structuring accounts (especially for couples). Done well, it can increase your after-tax income and help your money last longer while staying within the rules.

Want a clearer plan for drawing income tax-effectively from super and investments? Join a What If Advice retirement workshop to learn how retirement income streams, withdrawal strategies, and common offsets fit together (and what to ask before you act).

General advice disclaimer: This article provides general information only and doesn’t consider your objectives, financial situation or needs. Tax and Centrelink rules are complex and change over time. Consider getting personal advice from a licensed financial adviser and/or registered tax agent, and confirm details are subject to current ATO and Services Australia rules.