Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

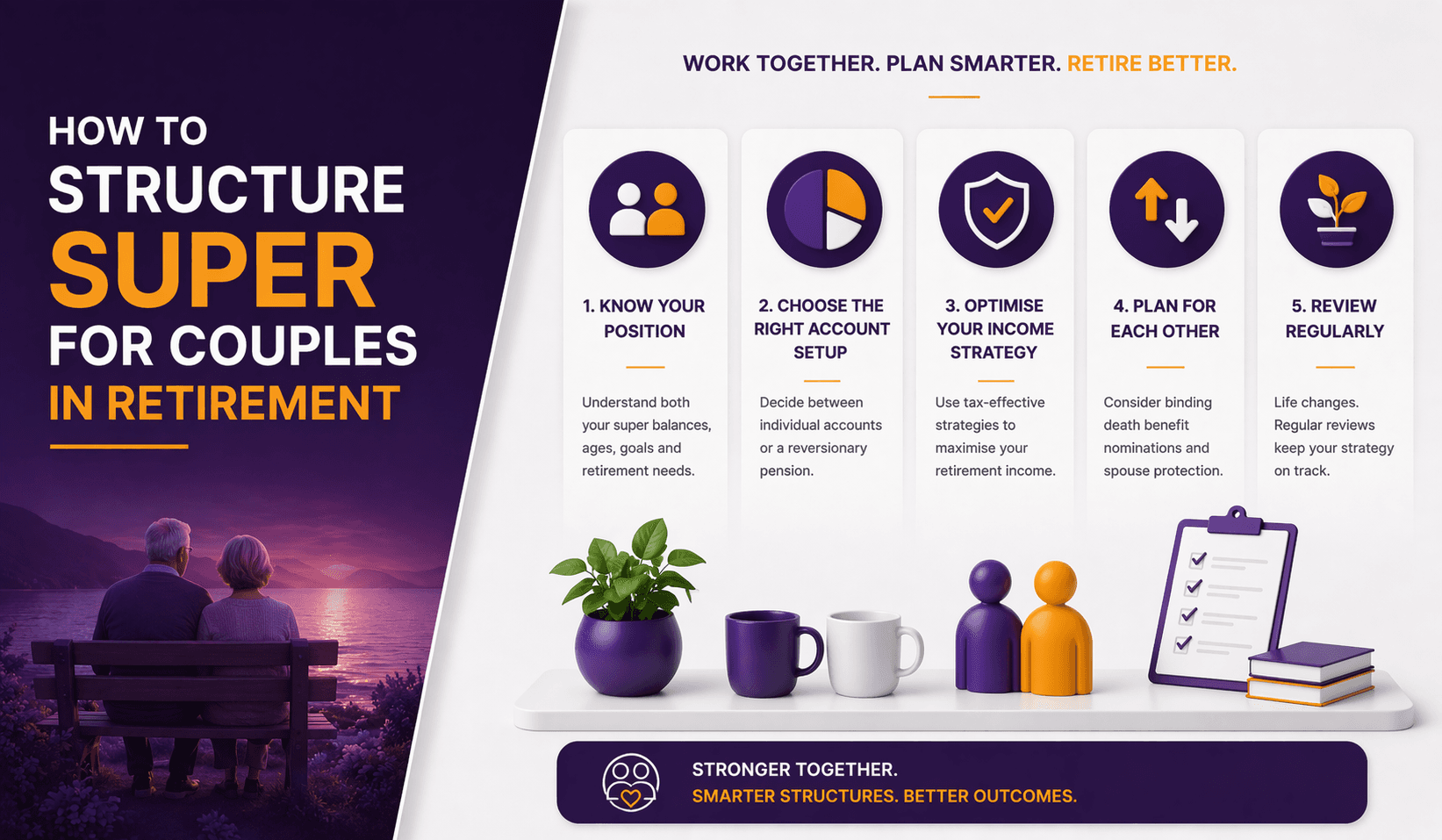

How to Structure Super for Couples in Retirement

When couples retire, superannuation should not be viewed as two separate accounts operating independently.

Strategic structuring can improve:

Tax efficiency

Age Pension eligibility

Income sustainability

Estate planning outcomes

Handled poorly, it can reduce entitlements and increase long-term risk.

Here’s how Australian couples can structure super effectively in retirement.

Step 1: Assess Combined Super Balances

Start by reviewing:

Each partner’s super balance

Contribution history

Preservation age

Tax components (tax-free vs taxable)

Imbalances are common. One partner may have significantly more super than the other.

Example:

Partner | Super Balance |

Chris | $900,000 |

Taylor | $200,000 |

Without planning, this imbalance may affect pension caps, Age Pension assessments and estate outcomes.

Step 2: Understand the Transfer Balance Cap (Per Person)

Each individual has their own Transfer Balance Cap (TBC), the limit on how much can move into tax-free pension phase (subject to current ATO rules).

This cap applies per person, not per couple.

If one spouse has significantly more super:

They may exceed their cap.

Excess must remain in accumulation phase (taxed at 15%).

Strategically equalising balances before retirement can maximise tax-free pension space.

Step 3: Consider Super Splitting Strategies

Before retirement, couples may consider:

Contribution splitting

Spouse contributions

These strategies can:

Equalise balances

Increase access to two pension caps

Improve Age Pension positioning

Contribution splitting allows concessional contributions to be transferred to a spouse’s super (subject to eligibility rules).

Timing is critical and must comply with ATO regulations.

Step 4: Start Separate Account-Based Pensions

In retirement, each partner should generally:

Establish their own account-based pension

Meet minimum drawdown requirements individually

Why this matters:

Each person’s pension is assessed separately under Age Pension rules.

Tax-free status applies individually.

Estate planning flexibility improves.

A joint pension is not typical in Australia. Each super account remains legally separate.

Step 5: Optimise for the Age Pension Assets Test

For couples, Age Pension eligibility is assessed on combined assets.

However:

The principal residence is generally exempt (subject to Services Australia rules).

Super in pension phase counts as an assessable asset once both partners are Age Pension age.

Strategic considerations include:

Balancing assets inside and outside super

Considering downsizing contributions

Reviewing timing of pension commencement

Small structuring differences can materially affect part-pension eligibility.

Step 6: Coordinate Withdrawal Rates

Couples should not automatically withdraw equal amounts.

Instead, consider:

Tax components

Age Pension impact

Longevity expectations

Health status

For example:

If one partner has a larger taxable component, structured withdrawals may reduce long-term tax exposure for beneficiaries.

Withdrawal coordination is often overlooked but important.

Step 7: Investment Allocation in Retirement

Each partner’s pension can have different investment allocations.

However, from a household perspective, asset allocation should be viewed holistically.

Example structure:

Partner A: Slightly higher growth allocation

Partner B: More defensive allocation

Together, this balances risk and sustainability.

Retirement may last 25–30 years. Inflation protection remains essential.

Step 8: Estate Planning Alignment

Super does not automatically form part of your estate.

Couples should review:

Binding death benefit nominations

Reversionary pension nominations

Tax implications for adult children

A reversionary pension allows the surviving spouse to continue receiving pension income without interruption.

Failure to align estate planning with super structure can create avoidable complications.

Example Scenario

Emma and Daniel, both 67:

Emma: $1.2 million super

Daniel: $300,000 super

Without adjustment:

Emma exceeds her Transfer Balance Cap.

Daniel underutilises his.

With pre-retirement balancing:

They equalise closer to $750,000 each.

Both maximise tax-free pension phase.

Age Pension modelling improves.

This type of structuring can materially increase long-term after-tax income.

Common Mistakes Couples Make

Treating super independently instead of strategically

Ignoring contribution splitting before retirement

Overlooking Transfer Balance Cap limits

Failing to review estate planning documents

Assuming equal withdrawals are optimal

Retirement planning for couples requires coordinated modelling.

FAQs

1. Can couples combine their super accounts?

No. Super remains individually owned, but strategies can be coordinated.

2. Does each spouse get their own Transfer Balance Cap?

Yes. The cap applies per individual under current ATO rules.

3. Should couples have equal super balances?

Not mandatory, but balance equalisation can improve tax efficiency and pension flexibility.

4. How does super affect the Age Pension for couples?

Combined assessable assets and income determine eligibility under Services Australia rules.

5. Can a pension continue to a surviving spouse?

Yes, via a reversionary pension nomination.

6. Is super tax-free in retirement for both partners?

Generally yes after age 60, subject to current super legislation.

Coordinate Your Super Strategically Before and During Retirement

For couples, retirement planning is not just about total assets, it is about how those assets are structured.

Balancing super accounts, managing pension caps, coordinating withdrawals and aligning estate planning can materially improve long-term outcomes.

At What If Advice, we help Australian couples model retirement income scenarios under current ATO and Services Australia rules to optimise tax efficiency and sustainability.

If you are within 10 years of retirement or already retired, structured advice can make a meaningful difference.

Book a retirement strategy consultation for couples with What If Advice.

General Advice Disclaimer

This article provides general information only and does not take into account your personal objectives, financial situation or needs. Before making financial decisions, consider whether the information is appropriate for your circumstances and seek personal advice from a licensed financial adviser. Superannuation, taxation and Age Pension rules are subject to change under current ATO and Services Australia regulations.