Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

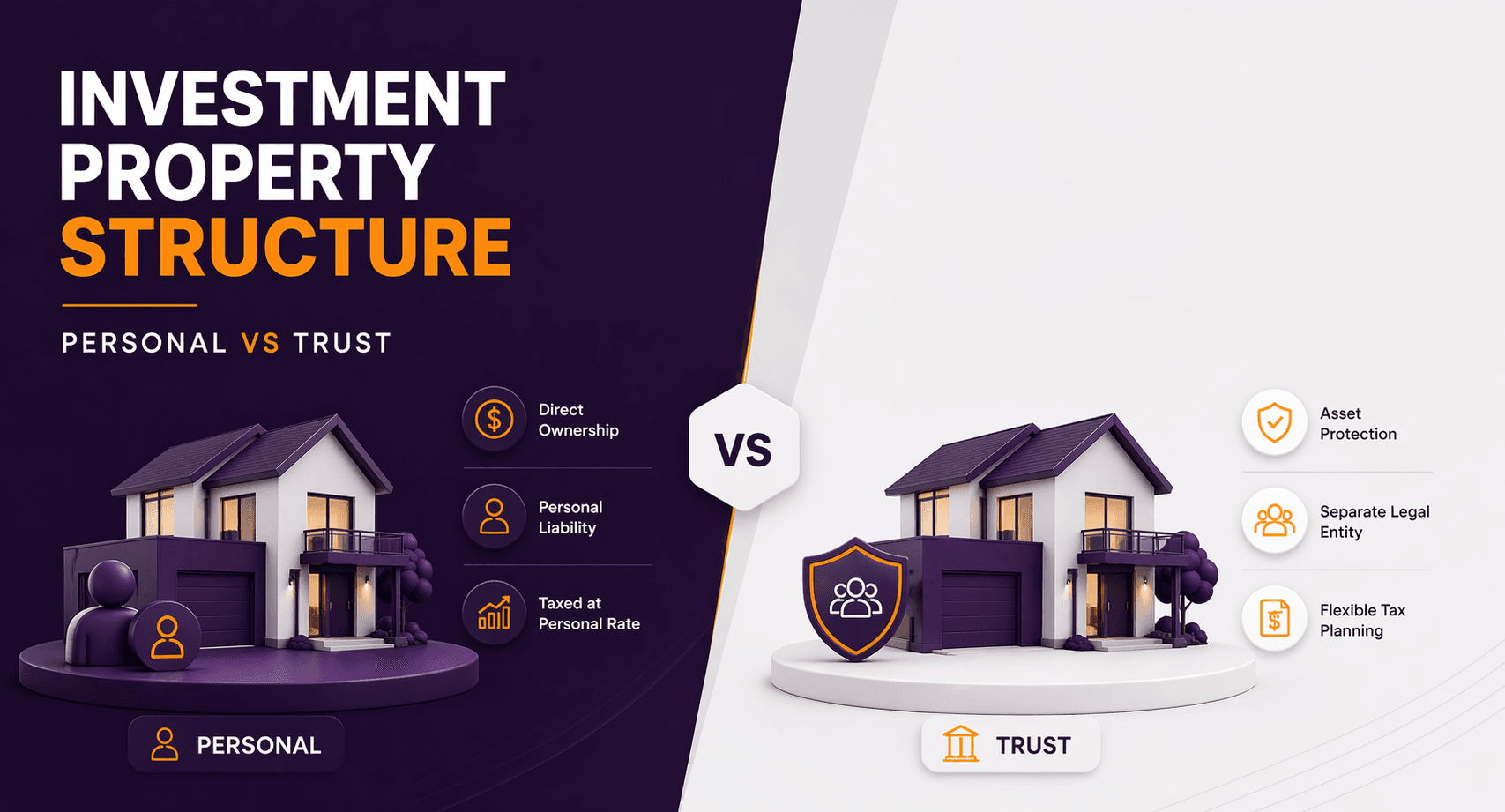

Investment Property Structure: Personal vs Trust (Australia)

Choosing how to hold an investment property is just as important as choosing the property itself.

The short answer:

Personal ownership = simpler and often more tax-efficient for individuals

Trust ownership = more flexibility and asset protection, but more complexity

There’s no one-size-fits-all answer. The right structure depends on your income, goals, and long-term strategy.

Why Structure Matters

The way you own a property affects:

Tax outcomes

Asset protection

Borrowing capacity

Estate planning

Getting it wrong can limit flexibility or cost you more over time.

Option 1: Buying in Your Personal Name

This is the most common approach in Australia.

How it works:

You purchase the property in your own name (or jointly with a partner).

Benefits of Personal Ownership

1. Simpler and Lower Cost

No complex legal structures

Lower setup and ongoing costs

2. Access to Negative Gearing Benefits

Losses can be offset against your personal income (subject to ATO rules).

This can reduce your taxable income if you’re negatively geared.

3. Capital Gains Tax (CGT) Discount

Individuals may access the 50% CGT discount if the property is held for more than 12 months (subject to ATO rules).

Drawbacks of Personal Ownership

1. Limited Asset Protection

Your personal assets may be exposed to:

Legal claims

Financial risk

2. Less Tax Flexibility

Income is taxed at your personal marginal tax rate.

You can’t distribute income to others.

Option 2: Buying Through a Trust

A trust is a legal structure where a trustee holds assets on behalf of beneficiaries.

The most common type is a discretionary (family) trust.

Benefits of Using a Trust

1. Asset Protection

Assets held in a trust may be better protected from:

Personal liabilities

Legal claims

(Subject to proper structuring and legal advice.)

2. Income Distribution Flexibility

Trusts can distribute income to beneficiaries, which may:

Reduce overall tax

Provide flexibility year-to-year

3. Estate Planning Advantages

Trusts can:

Simplify transfer of wealth

Avoid some estate complications

Drawbacks of Using a Trust

1. No Negative Gearing Benefits to Individuals

Losses are typically:

Trapped in the trust

Cannot offset personal income

This reduces short-term tax benefits.

2. Higher Costs

Setup costs

Ongoing accounting and compliance

3. Lending Can Be More Complex

Some lenders:

Offer fewer options

Charge higher rates

Require personal guarantees

Personal vs Trust: Side-by-Side Comparison

Feature | Personal Ownership | Trust Structure |

Setup complexity | Low | High |

Ongoing costs | Low | Higher |

Tax flexibility | Limited | High |

Negative gearing | Yes | Limited |

CGT discount | Yes (50%) | Yes (conditions apply) |

Asset protection | Low | Higher |

Lending ease | Easier | More complex |

Tax Considerations (Important)

Subject to current ATO rules:

Personal ownership:

Income taxed at your marginal rate

Losses can offset your income

Trust ownership:

Income distributed to beneficiaries

Losses remain in the trust

This makes trusts less attractive for negatively geared strategies in the short term.

Real-Life Scenarios

Scenario 1: High-Income Earner (Personal Ownership)

James (earning $180,000):

Buys investment property personally

Uses negative gearing

Outcome:

Reduces taxable income

Gains CGT discount

Scenario 2: Family Wealth Strategy (Trust)

The Patel Family:

Uses discretionary trust

Distributes income across family members

Outcome:

Greater tax flexibility

Improved asset protection

When Personal Ownership May Be Suitable

You’re a PAYG employee

You want to use negative gearing

You prefer simplicity

You’re buying your first investment

When a Trust May Be More Appropriate

You have higher income and complex finances

You want asset protection

You’re building a long-term portfolio

You want flexibility in distributing income

Common Mistake: Choosing Structure Based Only on Tax

Tax is important, but it’s not everything.

You should also consider:

Risk exposure

Borrowing capacity

Long-term plans

A structure that saves tax today may limit flexibility tomorrow.

Can You Change Structure Later?

Not easily.

Changing ownership usually triggers:

Stamp duty

Capital gains tax (CGT)

This makes it critical to choose the right structure from the start.

Key Question: Personal vs Trust – Which Is Better?

Neither is “better” universally.

Personal ownership works well for simplicity and tax deductions

Trust structures work well for flexibility and asset protection

The right decision depends on your:

Income level

Investment strategy

Risk tolerance

Long-term goals

FAQs

1. Is it better to buy property in a trust or personal name?

It depends on your goals. Personal ownership is simpler, while trusts offer flexibility and asset protection.

2. Can I negatively gear in a trust?

Losses are generally retained within the trust and cannot offset personal income (subject to ATO rules).

3. Do trusts get the CGT discount?

Yes, in many cases, if conditions are met and assets are held for more than 12 months.

4. Are trusts more expensive?

Yes, due to setup and ongoing compliance costs.

5. Can I transfer property into a trust later?

Usually not without triggering stamp duty and CGT.

6. Do banks treat trust loans differently?

Yes. Lending may be more complex and sometimes less favourable.

7. Is asset protection guaranteed with a trust?

No. It depends on proper structuring and legal advice.

Choosing the Right Structure for Your Investment Property

The way you structure your investment can impact tax, risk, and long-term outcomes.

A poorly chosen structure can:

Limit flexibility

Increase costs

Create unnecessary complexity

A well-structured approach considers:

Your income and tax position

Your investment strategy

Your long-term goals

Getting this right from the beginning can save significant time, cost, and stress later.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional financial advice. Information is subject to current ATO and Services Australia rules and may change over time.