Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

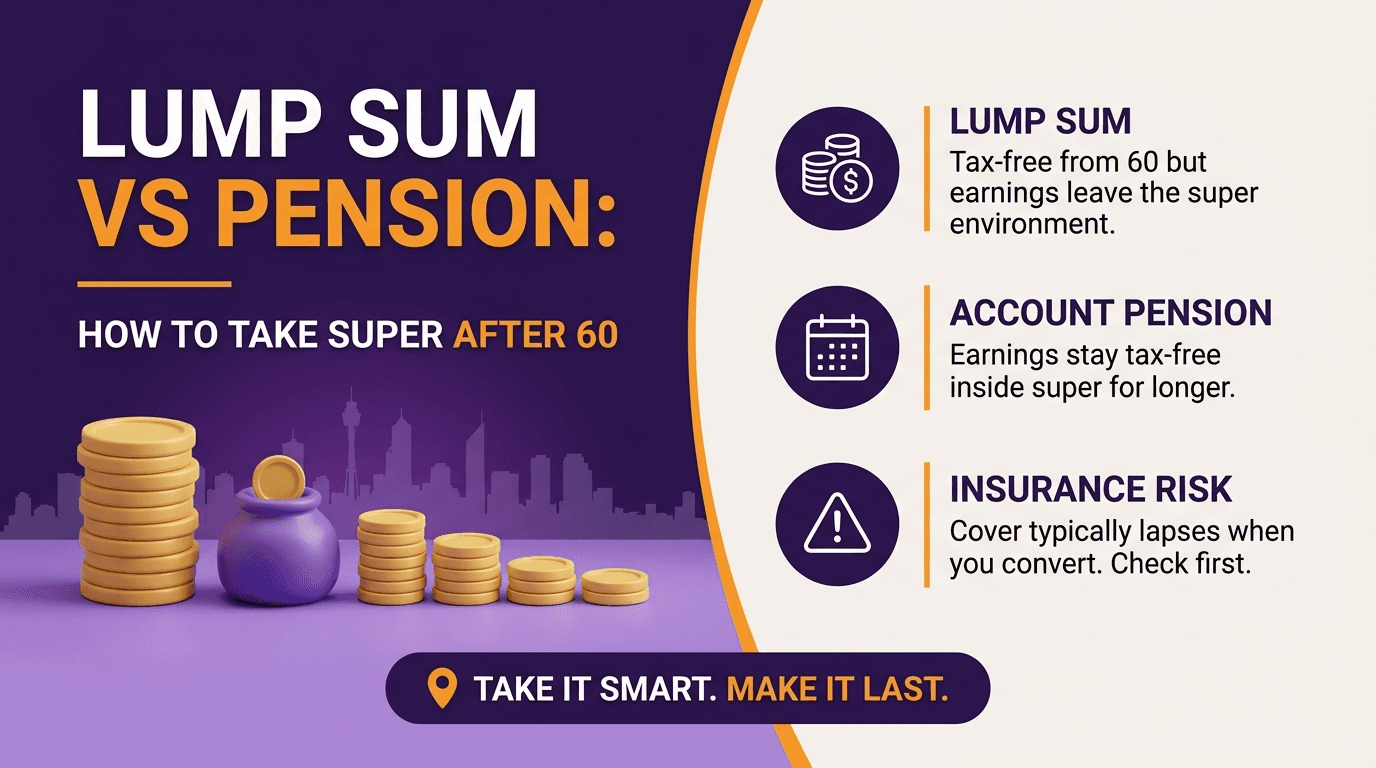

Lump Sum vs Pension: How to Take Money Out of Super After 60

What if the decision about how to take your super out is more consequential than any investment decision you've ever made, because it shapes your income, your tax, and your financial security for the next 30 years? The two main options are a lump sum or an account-based pension. Both are generally tax-free from age 60 for most Australians. But the critical difference isn't how they're taxed on the way out. It's what happens to the earnings on the money that stays invested. This guide explains both options clearly, when each one wins, and why most Australians end up using a combination of the two.

TL;DR: The Decision in Plain English

Both lump sum withdrawals and account-based pension payments are generally tax-free from age 60 for taxed super funds

The critical difference is not tax on withdrawal but tax on earnings while the money remains invested

Earnings inside an account-based pension are tax-free; earnings in accumulation are taxed at 15%; earnings on money withdrawn to a personal account are taxed at your marginal rate

A lump sum gives full flexibility but removes the tax-free earnings environment

An account-based pension keeps money growing tax-free inside super while providing regular income

Most Australians benefit from a combination approach — taking a partial lump sum for specific needs and converting the remainder to a pension

Don't convert super to a pension without checking your insurance cover first — it typically lapses on conversion and most retirees don't know this

Bottom line: The decision is not really about lump sum versus pension. It is about how much of your super to keep in the tax-free pension environment and how much to move outside it.

Jump to a Section

What Changes When You Turn 60

How Lump Sum Withdrawals Work

How Account-Based Pensions Work

The Critical Tax Difference: Earnings, Not Withdrawals

When a Lump Sum Makes Sense

When an Account-Based Pension Wins

The Combination Approach: What Most Retirees Actually Do

The Insurance Warning: Act Before Converting — read this before you do anything

Two Retirement Examples: Single and Couple

Common Mistakes Retirees Make

FAQ

Ready to Work Out the Right Strategy for Your Retirement?

What Changes When You Turn 60

The change at 60 is significant and immediate. These are the things that shift simultaneously once you meet the conditions:

From age 60 in a standard taxed super fund:

Lump sum withdrawals are generally tax-free on both the tax-free and taxable components

Account-based pension payments are generally tax-free on the taxed element

Investment earnings inside a pension account are tax-free at the fund level

The 15% tax on earnings that applies in the accumulation phase is eliminated in the pension phase

Equally important is what doesn't change. These rules continue to apply regardless of age:

The transfer balance cap still limits how much super can move into retirement phase ($2.0 million currently, rising to $2.1 million from 1 July 2026)

Minimum drawdown rates still apply to account-based pensions

Age Pension deeming rules still apply once you reach Age Pension age (67)

Superannuation insurance (life, TPD, income protection) typically lapses when you convert from accumulation to pension phase

Bottom line: The key change at 60 is the shift to tax-free treatment on both withdrawals and pension earnings. The strategies that make sense before 60 change significantly once this threshold is reached.

Approaching 60 and want to understand your specific options before you reach the milestone? Book a free 15-min chat with WIAA's financial advisers now. It costs nothing and ensures you're prepared before the decision arrives. Phone 1800 942 843.

How Lump Sum Withdrawals Work

Lump sums are simple and flexible. These are the mechanics:

Can be taken as a single large withdrawal or multiple smaller amounts over time

Generally tax-free from age 60 for most Australians in taxed super funds

No minimum or maximum limits in the retirement phase

Funds withdrawn are immediately available for any purpose

If reinvested outside super, investment earnings are taxed at the individual's marginal rate

Interest on bank deposits, dividends, and capital gains on shares held outside super all become personal taxable income

The flexibility of a lump sum is its primary appeal. A retiree who needs $80,000 to pay off a mortgage, fund a renovation, or buy a caravan can access that exact amount without being restricted to the income stream structure.

The disadvantage is that once the money leaves super, it loses access to the most tax-efficient investment environment in Australia. Reinvesting $500,000 outside super at a 6% return generates approximately $30,000 per year in taxable income versus $0 in tax if the same amount earns the same return inside a pension account.

What if you took your entire super as a lump sum at 63, reinvested it personally, and then watched $15,000 per year disappear in income tax on the earnings, every year for 25 years? That's the cost of leaving the pension environment. The lump sum is tax-free on the way out. What happens to the earnings on the money you keep is the decision that actually matters.

Bottom line: Lump sums provide maximum flexibility and are tax-free from 60. The cost is losing the tax-free earnings environment on whatever is withdrawn.

How Account-Based Pensions Work

Account-based pensions are the most common retirement structure for good reason. These are the mechanics:

Super balance stays invested, now in the pension phase where earnings are tax-free

Regular income payments made to your bank account monthly, quarterly, or annually at your choice

Payment amount is flexible: choose any amount above the minimum drawdown

Minimum drawdown rates apply by age band (see table below)

No maximum drawdown in retirement phase: you can withdraw any amount including the full balance at any time

Additional lump sum withdrawals can be made at any time alongside regular pension payments

From age 60, both regular payments and lump sum withdrawals from the pension are generally tax-free

Minimum annual drawdown rates:

Age at 1 July | Minimum Annual Drawdown |

Under 65 | 4% |

65 to 74 | 5% |

75 to 79 | 6% |

80 to 84 | 7% |

85 to 89 | 9% |

90 to 94 | 11% |

95 and over | 14% |

The minimum is calculated on the account balance at 1 July each year. If a pension commences on or after 1 June, no minimum payment is required for that year.

What if starting a pension doesn't mean you lose access to your money? This is the most common misconception about account-based pensions. The money is accessible at any time, in any amount, with no restrictions beyond the minimum drawdown. The pension is a tax structure, not a lock.

Bottom line: An account-based pension keeps super invested in a tax-free environment while providing flexible income. The minimum drawdown requirement is the only structural constraint on how little you take out each year.

The Critical Tax Difference: Earnings, Not Withdrawals

Most Australians focus on the tax treatment of withdrawals when comparing lump sums and pensions. This is the wrong focus. Both are generally tax-free from age 60. The critical tax difference is what happens to the earnings on the remaining balance.

Scenario | Tax on Earnings |

Super in accumulation phase | 15% on investment earnings (10% on capital gains held 12+ months) |

Super in pension phase (account-based pension) | 0% on all investment earnings |

Money withdrawn and held in bank account | Marginal rate on interest (up to 47%) |

Money withdrawn and invested in shares | Marginal rate on dividends and capital gains (up to 47%, or 23.5% after 50% CGT discount) |

For a retiree with $600,000 who achieves a 6% net return:

Kept in accumulation: earnings of $36,000 taxed at 15% = $5,400 in tax annually

Converted to an account-based pension: earnings of $36,000 taxed at 0% = $0 in tax annually

Withdrawn and invested personally at 37% marginal rate: earnings of $36,000 taxed at $13,320 annually

The annual tax difference between keeping money in an account-based pension versus withdrawing it and reinvesting personally is $13,320 per year for a retiree in the 37% bracket with $600,000 invested. Over 20 years, the compounding impact of this difference is substantial.

Bottom line: The decision between lump sum and pension is primarily a decision about how much to keep in the tax-free earnings environment of the pension phase. Every dollar withdrawn from the pension and reinvested personally moves from 0% tax on earnings to the individual's marginal rate.

Want to understand how the lump sum versus pension decision plays out with your specific super balance and income needs? The free Retire Ready Roundtable workshop covers exactly this — retirement income structuring, tax treatment, and Age Pension integration in 90 minutes. Brisbane, Melbourne, and online. Reserve your seat.

When a Lump Sum Makes Sense

Lump sums are not wrong. They're right in specific circumstances. These are the situations where they make sense:

Paying off non-deductible debt. A mortgage with a 6% interest rate is not tax-deductible. Withdrawing super to eliminate it provides a guaranteed 6% after-tax return, often comparable to or better than investing that amount inside or outside super depending on the circumstances.

Funding a specific large purchase. A caravan, renovation, overseas trip, or other defined purpose where the amount is known and the need is immediate.

Bringing the balance below a structurally important threshold. For members approaching the transfer balance cap, withdrawing a lump sum from accumulation before commencing a pension can preserve more cap space. Professional advice is essential before this decision.

Estate planning reasons. In some circumstances, withdrawing super and restructuring it outside the super system aligns better with estate planning intentions, particularly where non-dependant beneficiaries would face tax on inherited super.

Emergency or unexpected needs. Account-based pensions allow additional lump sum withdrawals at any time, so a pension does not lock away access to capital.

Bottom line: Lump sums make sense for specific, defined purposes. Taking the entire super balance as a lump sum and reinvesting it outside super is rarely the optimal strategy from a tax perspective.

When an Account-Based Pension Wins

The account-based pension is the right primary structure in most circumstances from age 60, for three main reasons.

Tax-Free Earnings

As demonstrated above, the pension phase provides 0% tax on earnings compared to accumulation (15%) or personal investment (marginal rate). For a $700,000 balance growing at 6%, this saves approximately $10,500 per year versus accumulation and up to $19,740 per year versus personal investment at the top marginal rate.

Regular, Structured Income

The pension provides a regular income stream aligned to living expenses. For most retirees, a predictable monthly or fortnightly payment is operationally superior to periodically withdrawing lump sums and manually managing cashflow.

Flexibility Is Not Sacrificed

A critical misunderstanding: many retirees think that starting an account-based pension locks away their money. It does not. An account-based pension in retirement phase allows lump sum withdrawals at any time, in any amount, with no restrictions. The pension is a structure, not a lock.

Age Pension Integration

Account-based pensions are assessed under the assets test and income test (via deeming) for Age Pension purposes. The pension's ability to generate tax-free earnings means the balance sustains for longer, supporting income across a 25 to 30 year retirement, which in turn supports partial Age Pension entitlements as the balance eventually reduces.

Bottom line: The account-based pension wins on tax efficiency, structured income, and longevity. It does not win on flexibility, which is equivalent to a lump sum since additional withdrawals are always available.

The Combination Approach: What Most Retirees Actually Do

In practice, most well-advised retirees use a combination of both strategies rather than choosing one exclusively.

A typical combination approach at retirement:

Identify any specific lump sum needs — mortgage balance, planned purchase, emergency buffer, or estate planning amount.

Withdraw the identified lump sum from the accumulation account before or at pension commencement.

Convert the remaining balance to an account-based pension, maximising the tax-free earnings environment.

Draw the minimum pension where cashflow allows, preserving more capital in the tax-free environment for longer.

Take additional lump sums from the pension account as needed throughout retirement.

Example: A retiree with $750,000 in super at age 63, a $95,000 mortgage balance, and a $30,000 planned overseas trip might withdraw $125,000 as a lump sum to pay off the mortgage and fund the trip, then convert the remaining $625,000 to an account-based pension and draw the 4% minimum ($25,000 per year) initially, increasing as lifestyle expenses rise.

The $625,000 in the pension phase grows tax-free. The $125,000 withdrawn is tax-free at point of withdrawal. The retiree has both the financial goals met and the bulk of assets in the most tax-efficient structure available.

This pattern — partial lump sum for specific needs, remainder to pension — is the most common structure across WIAA's retirement planning clients. The specific amounts vary enormously, but the logic is consistent: use the tax-free withdrawal for defined purposes, maximise the tax-free earnings environment for everything else. The exact split depends on income needs, mortgage position, estate goals, and other assets.

Bottom line: The combination approach is typically optimal because it addresses specific needs efficiently while preserving the tax-free earnings environment for the majority of the balance.

The Insurance Warning: Act Before Converting

This is the section most retirement guides don't include, and it catches a significant number of retirees completely unprepared. Read this before you do anything with your super.

When super moves from the accumulation phase to the pension phase, any life insurance, TPD cover, or income protection held inside the super fund typically lapses. This default position catches many retirees completely unprepared.

Before converting accumulation super to a pension, every retiree should:

Review what insurance cover is held inside their current super fund

Assess whether they still need any of that cover in retirement

If cover is still needed (life insurance for estate planning or a surviving spouse, for example), arrange replacement cover before or simultaneously with the pension commencement

Income protection is rarely needed in full retirement. Life insurance for estate purposes or a younger dependent spouse may still be relevant. TPD cover is generally less relevant once retired. Each situation is different.

Bottom line: Converting super to a pension without reviewing insurance cover is one of the most common and potentially costly oversights in retirement planning. Check before you convert.

Unsure what insurance you hold inside your current super fund? This is the question to answer before you do anything else. Book a free 15-min chat with WIAA to review your insurance position before pension commencement: 1800 942 843 or clientservices@whatifadvice.com.au.

Two Retirement Examples: Single and Couple

Example 1: Margaret, 63, Retiring with $680,000

Margaret retires at 63 with $680,000 in super. She owns her home outright and has no debt. She wants a comfortable lifestyle income of approximately $52,000 per year and expects to become eligible for a partial Age Pension at 67.

Her strategy:

Withdraw $20,000 as a lump sum to fund a trip and establish a household cash buffer

Convert the remaining $660,000 to an account-based pension

Draw the minimum 4% ($26,400) in year one, supplemented by the $20,000 buffer as needed

Gradually increase the drawdown as needed, targeting $52,000 per year in combination with a partial Age Pension from 67

Tax on the $660,000 in pension phase: earnings of approximately $39,600 per year (at 6% net) are completely tax-free. If Margaret had withdrawn the full $680,000 and reinvested personally, her earnings would be taxed at approximately 30%, costing approximately $11,900 per year in additional tax.

By 67, her balance has reduced modestly to approximately $600,000. Her partial Age Pension supplements income as the balance gradually reduces over the following decades.

Example 2: Robert and Helen, Both 67, Combined $1.15 Million

Robert and Helen are both retiring at 67. They have $680,000 in Robert's super and $470,000 in Helen's, totalling $1.15 million. They have a $120,000 mortgage remaining and want a combined income of approximately $80,000 per year.

Their strategy:

Robert withdraws $120,000 as a lump sum to pay off the mortgage (tax-free)

Robert converts the remaining $560,000 to an account-based pension

Helen converts her full $470,000 to an account-based pension

Both draw the minimum 5% (age 67 to 74 bracket) initially: Robert $28,000, Helen $23,500, total $51,500

Age Pension supplements income: they receive an estimated partial Age Pension of approximately $28,000 combined initially

Combined income from pensions and Age Pension: approximately $79,500 per year, close to their $80,000 target

Both pension accounts earn investment returns tax-free. The $120,000 withdrawn for the mortgage is tax-free at point of withdrawal and eliminates approximately $7,200 per year in mortgage interest. Total annual tax on investment earnings: approximately $0 on the $1.03 million in combined pension phase versus approximately $34,500 per year if the same money were invested personally at their marginal rates.

Common Mistakes Retirees Make

Taking the entire balance as a lump sum and investing it personally. This moves the entire balance from 0% tax on earnings to the marginal rate. For a $700,000 balance at 6% returns and a 37% marginal rate, the annual cost is approximately $15,540 in additional tax every year.

Leaving super in the accumulation phase after retiring. Many retirees do not bother converting to a pension because they already have other income. Every year left in accumulation rather than pension phase costs 15% on earnings unnecessarily.

Not reviewing insurance before converting to a pension. Insurance in accumulation super typically lapses on pension commencement. Many retirees are briefly or permanently uninsured because they did not check before converting.

Thinking the pension locks away their money. Account-based pensions in retirement phase allow lump sum withdrawals at any time with no penalty or restriction. This is not a constraint.

Drawing more than needed from the pension in early retirement. High drawdowns in the first years of retirement reduce the compounding base for the remaining decades. Drawing closer to the minimum and supplementing with other income where possible extends the fund significantly.

Ignoring the transfer balance cap before commencing a pension. Members with balances approaching $2.1 million need to plan pension commencement carefully to maximise their personal cap entitlement. Errors here are difficult and costly to reverse.

Not seeking advice at this decision point. The pension commencement decision, including timing, amount, investment option, and beneficiary nominations, shapes retirement income for the next 25 to 30 years. It is one of the highest-value moments to engage professional advice.

FAQ

Is a lump sum from super tax-free after 60?

Generally yes. For most Australians in a standard taxed super fund, lump sum withdrawals from age 60 are tax-free on both the tax-free and taxable components. Some exceptions apply for untaxed super funds (such as certain government defined benefit schemes) where different tax treatment applies. Always verify with your specific fund.

Do I have to convert to a pension or can I just take lump sums?

You are not required to convert to an account-based pension. You can withdraw lump sums from your accumulation account as needed after meeting a condition of release. However, leaving the balance in accumulation means earnings continue to be taxed at 15%, whereas converting to a pension makes earnings tax-free. Taking everything as a lump sum and reinvesting personally means earnings are taxed at your marginal rate.

Can I take a lump sum from an account-based pension?

Yes. Account-based pensions in the retirement phase allow lump sum withdrawals at any time in any amount. There is no lock-in period and no restrictions beyond meeting the minimum annual payment requirement. Many retirees use their pension as their primary structure and take lump sums from it when needed.

What is the minimum I have to draw from an account-based pension?

The minimum drawdown is a percentage of your account balance at 1 July each year, ranging from 4% for those under 65 to 14% for those aged 95 and over. There is no maximum drawdown in the retirement phase. You can withdraw more than the minimum at any time.

What happens to my super insurance when I start a pension?

Life insurance, TPD cover, and income protection insurance held inside your accumulation super account typically lapse when you convert to an account-based pension. Review your insurance cover before commencing a pension and arrange replacement cover if still needed, before the conversion takes effect.

How does the transfer balance cap affect my pension?

The transfer balance cap limits how much super can be moved into the retirement phase where earnings are tax-free. The current cap is $2.0 million, rising to $2.1 million from 1 July 2026. Amounts above the cap must remain in accumulation where earnings are taxed at 15%. Members approaching the cap should plan pension commencement carefully.

Should I take a lump sum to pay off my mortgage before starting a pension?

Often yes, if the mortgage rate is meaningful and the lump sum is tax-free from age 60. Eliminating a 6% non-deductible mortgage provides a guaranteed 6% after-tax return. The remaining balance can then be converted to a pension. Model the specific numbers before acting, as the right answer depends on your balance, mortgage amount, and income needs.

Can I go back to lump sum withdrawals after starting an account-based pension?

Yes. An account-based pension in retirement phase allows additional lump sum withdrawals at any time with no restrictions. You can also commute (wind back) a pension to accumulation in some circumstances, though this affects your transfer balance cap position and should be considered with professional advice. Starting a pension does not permanently close off access to lump sums.

What happens to my account-based pension when I die?

You can nominate a reversionary beneficiary (typically a spouse) to whom the pension continues automatically on your death. Alternatively, a lump sum death benefit can be paid to nominated beneficiaries. Tax treatment differs for dependant and non-dependant beneficiaries: dependants (including spouses and minor children) generally receive the benefit tax-free, while non-dependants (such as adult children) may pay tax on the taxable component of the death benefit. Binding death benefit nominations and reversionary pension decisions should be reviewed regularly.

Ready to Work Out the Right Strategy for Your Retirement?

The lump sum versus pension decision shapes your income, your tax, and your financial security for the next 25 to 30 years. Most retirees make it once and can't easily reverse it. Professional advice at this moment typically pays for itself many times over.

Still asking what if about your super withdrawal strategy? This is the decision where the answer matters most, and for the longest time.

Three ways to start:

Free 15-minute phone chat at 1800 942 843 to discuss your specific balance, income needs, and the right combination approach for your situation.

Free Retire Ready Roundtable workshop in Brisbane, Melbourne, or online. 90 minutes covering retirement income, super structuring, and Age Pension integration. Reserve your seat.

In-person meeting at our Toowong office if you'd prefer face-to-face for a decision of this significance. Book online or call 1800 942 843.

WIAA has advised 1,000+ Australians through retirement planning, with 6 financial advisers operating from offices in Toowong, Grange, and Melbourne. AFSL 528250.

General Advice Disclaimer: This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions. Super rules, transfer balance cap, minimum drawdown rates, and tax treatment are subject to change. Always verify current rules with the ATO or a licensed financial adviser before making withdrawal decisions. What If Advice is an Authorised Representative under Beryllium Advisers Pty Ltd, AFSL 528250.