Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

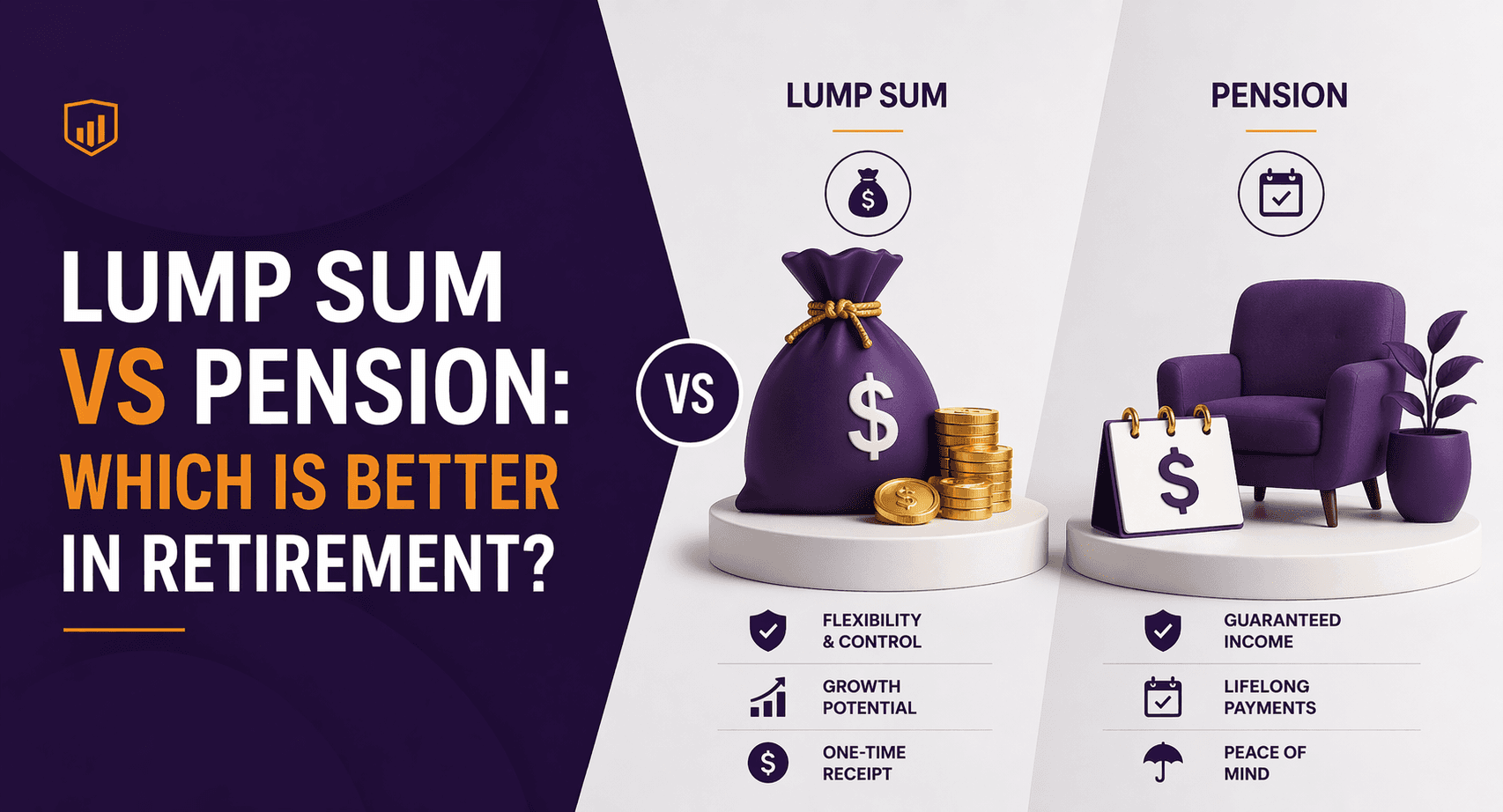

Lump Sum vs Pension: Which Is Better in Retirement?

When you retire, one of the first decisions you face is how to access your super.

You typically have three options:

Withdraw a lump sum

Start an account-based pension

Use a combination of both

Each approach affects tax, investment growth, income stability and how long your retirement savings may last.

Choosing the right structure is a key part of retirement planning.

What Is a Super Lump Sum?

A lump sum is a one-off withdrawal from your superannuation balance.

You may choose to withdraw part or all of your super as a cash payment once you meet a condition of release (subject to current super rules).

Common reasons retirees take a lump sum include:

Paying off a mortgage

Renovating or downsizing a home

Clearing personal debts

Funding large lifestyle purchases

After age 60, lump sum withdrawals from most taxed super funds are generally tax-free under current ATO rules.

What Is a Super Pension?

Instead of withdrawing all funds at once, you can convert your super into an account-based pension.

This creates a regular income stream.

Key features include:

Minimum annual withdrawal requirements

Investments remain inside super

Earnings are generally tax-free in pension phase (subject to ATO rules)

This structure allows retirement savings to continue growing while providing income.

Key Differences: Lump Sum vs Pension

Feature | Lump Sum | Account-Based Pension |

Access | Immediate | Regular income payments |

Investment growth | Stops if withdrawn | Continues inside super |

Longevity risk | Higher if spent quickly | Managed through drawdowns |

Tax treatment (60+) | Usually tax-free | Usually tax-free |

Flexibility | High | Moderate with structured withdrawals |

Both approaches can be appropriate depending on personal circumstances.

When a Lump Sum Might Make Sense

A lump sum withdrawal may be appropriate in certain situations.

1. Paying Off Debt

Clearing a mortgage before retirement can reduce living expenses and improve financial security.

2. Downsizing Housing

Some retirees withdraw funds to purchase a smaller home or relocate.

3. Major One-Time Expenses

Examples include:

Home modifications

Medical expenses

Helping family members

However, withdrawing too much early can increase longevity risk.

When a Pension May Be Better

For most retirees, an account-based pension becomes the core retirement income strategy.

1. Ongoing Income

A pension provides regular payments that support everyday living expenses.

2. Continued Investment Growth

Funds remain invested, which helps manage inflation over long retirements.

3. Tax Efficiency

After age 60, pension payments are generally tax-free under current super rules.

4. Sustainability

Structured withdrawals can help ensure savings last longer.

The Most Common Strategy: A Combination

Many retirees use a hybrid approach.

Example:

Total super: $800,000

$100,000 lump sum to clear mortgage

$700,000 moved into an account-based pension

Benefits include:

Reduced living expenses

Ongoing retirement income

Continued investment growth

This approach balances flexibility and sustainability.

How the Age Pension Fits In

Your decision may affect Age Pension eligibility.

Under Services Australia rules:

Assets inside super pension phase count toward the assets test

Lump sum withdrawals may affect bank balances and investments

Structuring withdrawals carefully can help optimise entitlements.

Risks of Taking Too Much Too Soon

One of the biggest risks in retirement is withdrawing large lump sums early.

Potential consequences include:

Reduced retirement income later in life

Increased longevity risk

Loss of tax-effective investment growth

Once money leaves super, it may be taxed differently depending on how it is invested.

Example Scenario

Michael retires at 67 with $900,000 in super.

Option A: Withdraw entire balance as lump sum

Funds invested personally

Tax treatment may vary

Option B: Start account-based pension

Minimum withdrawal around 5%

Remaining balance continues growing tax-free

Option C: Hybrid strategy

$150,000 lump sum

$750,000 pension

The hybrid strategy often balances flexibility and long-term income.

Common Mistakes

Retirees sometimes:

Withdraw their entire super unnecessarily

Underestimate how long retirement may last

Move too much money outside the tax-efficient super system

Ignore Age Pension interactions

Retirement income decisions should be part of a structured plan.

FAQs

1. Is it better to take super as a lump sum or pension?

For many retirees, a pension provides more sustainable income, while lump sums are useful for specific expenses.

2. Can I take both a lump sum and a pension?

Yes. Many retirees combine both approaches.

3. Is a super pension taxable after age 60?

Pension payments are generally tax-free after age 60 under current ATO rules.

4. Can I withdraw all my super at retirement?

Yes, once a condition of release is met. However, this may not be the most effective long-term strategy.

5. Does taking a lump sum affect the Age Pension?

It may affect assessable assets under Services Australia rules.

6. What happens if my pension balance runs out?

Payments stop once the account balance reaches zero.

Structure Your Super Withdrawals Strategically

Choosing between lump sum withdrawals and pension income can significantly affect how long your retirement savings last.

At What If Advice, we help Australians model retirement income scenarios and structure super withdrawals to support long-term sustainability under current ATO and Services Australia rules.

If you are approaching retirement or preparing to access your super, structured advice can help you make confident decisions.

Book a retirement income planning consultation with What If Advice.

General Advice Disclaimer

This article provides general information only and does not take into account your personal objectives, financial situation or needs. Before making financial decisions, consider whether the information is appropriate for your circumstances and seek personal advice from a licensed financial adviser. Superannuation, taxation and Age Pension rules are subject to change under current ATO and Services Australia regulations.