Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

If you’re shopping for a home loan, you’ve probably asked the question:

“Should I use a mortgage broker or go directly to my bank?”

It’s a smart question, because the choice can affect:

the interest rate you get

the fees you pay

how long approval takes

the range of lenders available

and whether your loan setup fits your long-term plans

The good news: both options can work well, depending on your circumstances.

The key is understanding what each option does best, and what the common pitfalls are, so you can make a confident decision.

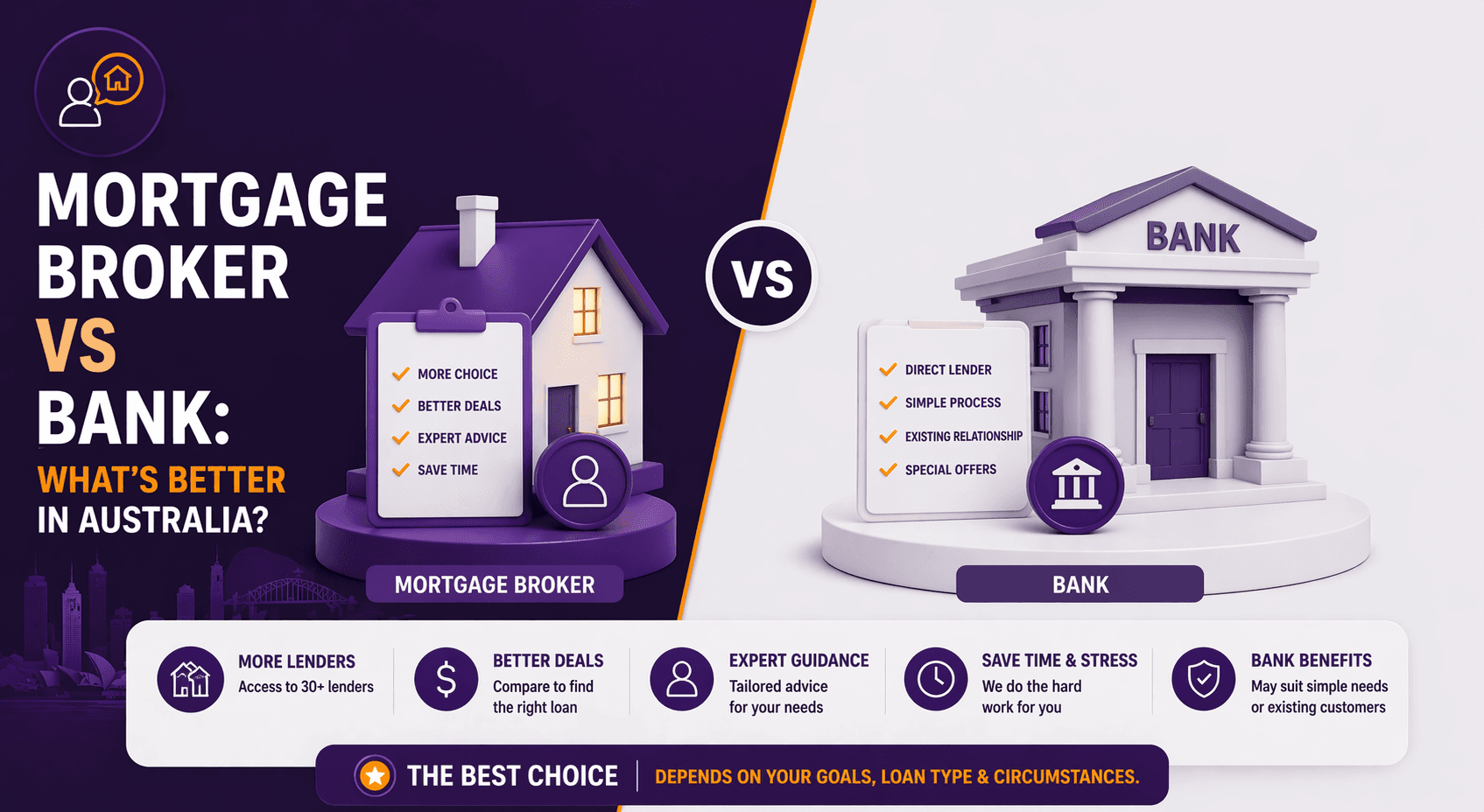

Quick Answer: Broker vs Bank (In Plain English)

A mortgage broker may be better if:

you want access to multiple lenders (not just one bank

your situation is complex (self-employed, variable income, multiple debts)

you want someone to negotiate and compare options for you

you want help with paperwork and lender policies

you want to shop around without doing it yourself

A bank may be better if:

you already bank there and want simplicity

you prefer direct dealing with the lender

your situation is straightforward

your bank offers strong pricing or loyalty benefits

you’re comfortable comparing offers yourself

What Does a Mortgage Broker Do?

A mortgage broker is a licensed professional who helps you:

compare home loan products

choose a lender that matches your needs

prepare and submit your loan application

manage communication with the lender

coordinate approvals and settlement

Most brokers can access a panel of lenders, which can include:

major banks

smaller banks

credit unions

non-bank lenders

specialist lenders

That means brokers can offer you more options than walking into a single bank.

Mortgage brokers must act in your best interests

In Australia, mortgage brokers have a legal obligation known as the Best Interests Duty, which requires them to act in the consumer’s best interests when providing credit assistance.

This is designed to reduce conflicted recommendations, but it doesn’t remove all risk (more on that below).

What Does a Bank Do?

When you go directly to a bank, you’re speaking with a lender who can only offer their own home loan products.

They can still:

give you competitive pricing

assess your borrowing capacity

approve and settle the loan

potentially offer package benefits or relationship pricing

But they won’t compare other lenders for you.

So the bank option is usually:

simple

direct

fast (sometimes)

but less broad in comparison.

The Big Difference: Choice vs Simplicity

Brokers offer choice

Mortgage brokers can compare multiple lenders and loan types, which can be helpful because not all lenders have the same:

interest rates

fees

cashback offers

approval policies

borrowing limits

risk appetite (especially for self-employed borrowers)

Banks offer simplicity

A bank can be easier if you:

already have your income and accounts there

have a straightforward PAYG job

fit cleanly into their lending criteria

don’t want back-and-forth across multiple lenders

Is a Mortgage Broker More Expensive Than Going to a Bank?

This is one of the biggest myths.

In most cases, you don’t pay a mortgage broker directly, the lender pays the broker a commission for introducing the loan. Brokers must disclose their commission structure to clients.

That said, “free” doesn’t mean “no cost”.

It means:

the broker is paid by the lender

and the loan pricing may include that distribution cost built into the lender’s margins

which can create potential conflicts (even with best interests rules)

ASIC has long reviewed broker remuneration and the effect commissions can have on consumer outcomes.

Practical takeaway:

A broker may still help you access a better deal than your bank, but you should understand how they’re paid and ask about alternatives.

Pros and Cons: Mortgage Broker

Pros

1) Access to multiple lenders and loan products

You’re not limited to one bank. Brokers can compare across lenders, which can increase your chance of finding a suitable loan.

2) Helpful if your situation is not “standard”

Brokers can be very useful if you are:

self-employed

casual or contract-based

earning commissions/bonuses

buying an investment property

refinancing with multiple debts

dealing with lower deposits or complex scenarios

3) Less legwork for you

They handle:

paperwork

lender communication

valuation processes

follow-ups

settlement coordination

4) Potentially better negotiation

A good broker can negotiate discounts and structure the loan well; especially if you’re refinancing or comparing multiple lenders.

Cons

1) They may not cover the entire market

Most brokers have a panel of lenders. That panel can be broad, but it might not include every lender or every product in the market.

2) Commission structure can influence behaviour

Brokers are paid commissions by lenders, and ASIC has historically flagged that commission structures can affect recommendations if not controlled properly

Even with Best Interests Duty, it’s worth asking:

why they recommended a certain lender

whether other lenders were considered

what the trade-offs are

3) Quality varies

Some brokers are outstanding, others are transactional. The broker’s skill affects the outcome more than people realise.

Pros and Cons: Going Direct to a Bank

Pros

1) Simple and direct

You deal with the decision-maker and can often move quickly.

2) Relationship benefits

Some banks offer:

discounts for existing customers

package benefits

offset account bundling

easier account linking

3) Certain banks are pushing direct lending

Some big banks are increasing their focus on direct lending channels due to cost pressures around broker commissions.

This can sometimes mean aggressive pricing or offers for direct customers.

Cons

1) You only see one lender’s options

Even if your bank has a good deal, there may be a better deal elsewhere, and you won’t know unless you compare.

2) Bank staff are not comparing the market

They work for the lender, so their job is to place you into their products.

3) Some banks may be stricter than other lenders

You might be declined at one bank even though another lender would approve you (particularly common with self-employed or non-standard income).

Which One Gets You a Better Rate in Australia?

This depends more on your profile than the channel.

A broker might get you a better rate if:

your bank isn’t competitive

you have strong equity and can refinance

you’re eligible for special lender policies

you want to compare smaller lenders and non-banks

Your bank might match or beat a broker offer if:

you have a strong relationship and high-value customer profile

the bank has a strong direct promotion

the bank is competing heavily for refinancing customers

In Australia, many rate comparison platforms track thousands of rates across dozens of providers, and rates can change frequently.

Practical move:

Even if you love your bank, compare at least 2–3 options (either yourself or through a broker).

A Simple “Decision Guide” (Choose Based on Your Situation)

Choose a mortgage broker if you:

want multiple lender comparisons

are self-employed or have complex income

want a structured recommendation

are refinancing and want negotiation

don’t have time to shop around

Choose a bank if you:

have a straightforward PAYG job

already have a strong banking relationship

are confident comparing rates and features yourself

don’t want broker involvement

your bank is offering a strong deal that’s hard to beat

What to Ask Before You Choose a Mortgage Broker

If you’re considering a broker, ask these questions upfront:

1) How many lenders do you have access to?

A broader panel often gives more options.

2) Are there lenders you don’t deal with, and why?

Transparency matters.

3) Why is this loan suitable for me?

A good broker should explain it simply.

4) How are you paid, and what commission do you receive?

Brokers must disclose this.

5) Can you show me 2–3 alternatives?

Seeing comparisons helps you understand trade-offs.

What to Ask Your Bank Before You Sign

If you go direct to your bank, ask:

Can you offer a rate discount?

Are there any package fees?

Is there an offset account?

What are the exit fees or discharge costs?

Is there a cashback offer?

What happens when the fixed rate ends?

Are there limits on extra repayments?

This helps prevent the common trap of signing a loan that looks good today but becomes expensive later.

Key Takeaways

Brokers offer broader lender choice and help with paperwork

Banks offer simplicity and direct access, but only to their own products

Brokers are usually paid by lenders and must disclose commission structures

Brokers have a Best Interests Duty under Australian law

The best option depends on complexity, time, and your desire to compare

Even if you go to your bank, it’s smart to compare at least a few options

FAQ

1) Is a mortgage broker better than a bank in Australia?

Not always. Brokers are often better for choice and complex situations, while banks can be better for simplicity if your situation is straightforward.

2) Do mortgage brokers cost money?

Usually no direct cost to you. They’re paid commission by lenders and must disclose how they’re paid.

3) Do mortgage brokers have to act in my best interests?

Yes. Brokers have a legal Best Interests Duty when providing credit assistance.

4) Can a bank match a broker’s deal?

Often yes; especially if you have strong equity or a good customer relationship. It’s worth asking for a discount.

5) Should I use a broker for refinancing?

Many Australians do this because brokers can compare lenders and negotiate, but it still depends on your needs and whether your broker has access to the right lenders.

So, mortgage broker vs bank: what’s better in Australia?

For most Australians, the best answer is:

Use a broker if you want choice, help, and guidance

Use your bank if you want simplicity and already have a strong deal

The smartest approach is usually to compare both. Even one comparison can save you thousands over the life of a loan, not just from interest rate differences, but from avoiding the wrong structure, fees, and features.

Still asking “what if” about your finances?

That’s exactly where clarity begins.

Whether you’re planning ahead, growing wealth, or simply want confidence in your financial decisions, the advisers at What If Advice can help you turn questions into a clear, personalised plan.

👉 Book a free 15-minute strategy session or get in touch today at

whatifadvice.com.au

General Advice Disclaimer

This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions.