Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

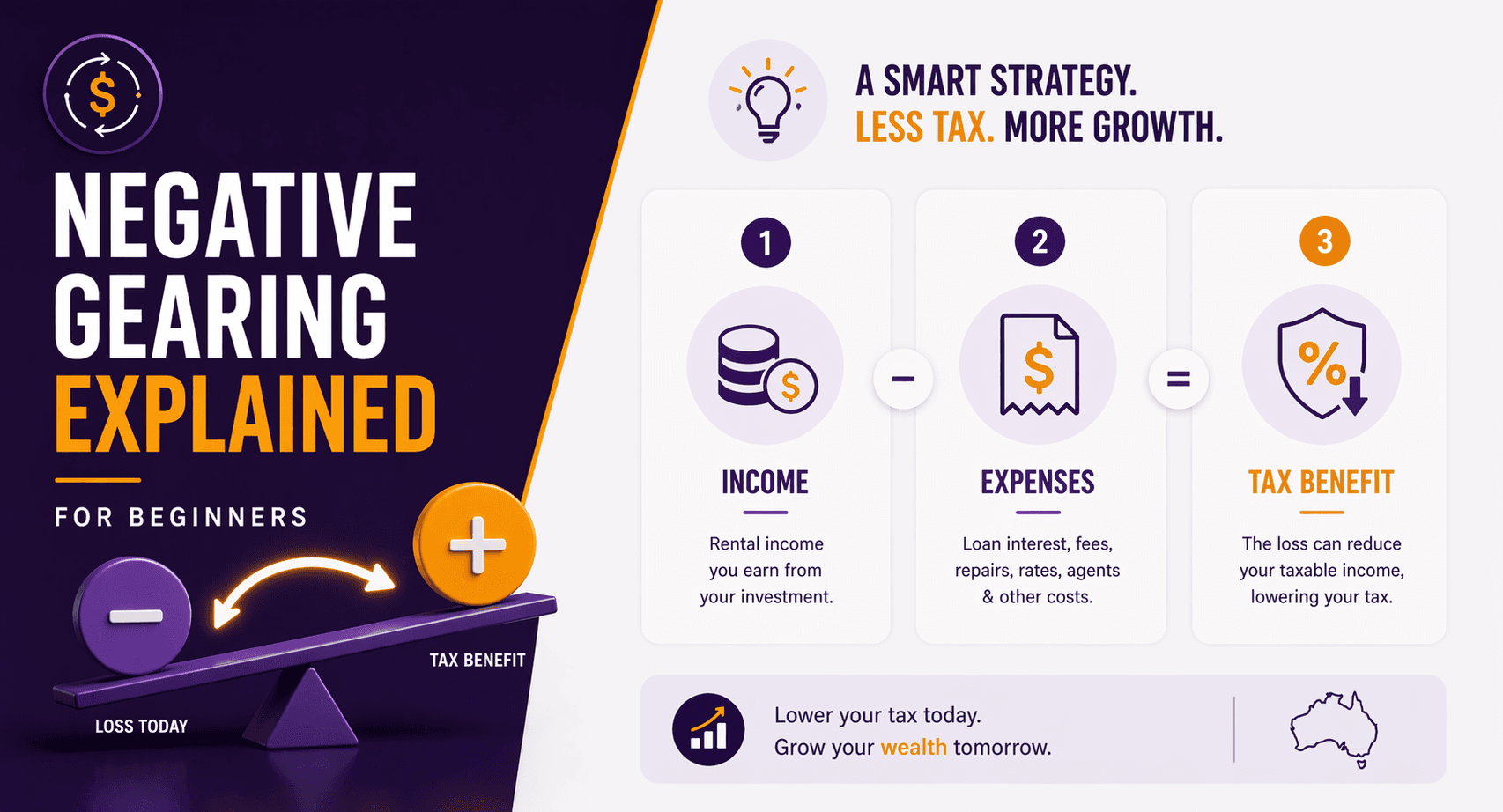

Negative Gearing Explained for Beginners (Australia)

Negative gearing is a strategy where your investment property costs more to hold than it earns in rental income.

The short answer:

You make a loss, and that loss can reduce your taxable income (subject to ATO rules).

It sounds simple. In reality, it’s often misunderstood and sometimes used for the wrong reasons.

What Is Negative Gearing?

Negative gearing occurs when:

Rental income < property expenses

Expenses may include:

Loan interest

Maintenance

Property management fees

Insurance

Depreciation (subject to ATO rules)

Simple Example

Item | Annual Amount |

Rental income | $25,000 |

Expenses | $32,000 |

Net loss | -$7,000 |

That $7,000 loss can generally be deducted against your income (e.g. salary), reducing your taxable income.

How the Tax Benefit Works

The tax benefit depends on your marginal tax rate.

Example:

Loss: $7,000

Tax rate: 37%

Tax saving:

~$2,590

But here’s the part people conveniently ignore:

You still lost $7,000 to get back $2,590.

You’re still out of pocket.

Why Do Investors Use Negative Gearing?

Because they’re betting on capital growth.

The idea:

Short-term loss

Long-term property value increase

If the property grows significantly, the gain may outweigh the ongoing losses.

Negative vs Positive Gearing

Feature | Negative Gearing | Positive Gearing |

Cash flow | Negative | Positive |

Tax impact | Reduces taxable income | Increases taxable income |

Risk level | Higher | Lower |

Strategy focus | Capital growth | Income generation |

What Expenses Can You Claim?

Subject to current ATO rules, common deductions include:

Interest on investment loans

Property management fees

Repairs and maintenance

Council rates

Insurance

Depreciation

Important:

Only the portion related to income-producing use is deductible.

The Real Benefit: Capital Gains (Not Tax Deductions)

Negative gearing is often misunderstood as a “tax strategy.”

It’s not.

The tax deduction simply reduces the pain of holding the property.

The real outcome depends on:

Property growth

Time in the market

Risks of Negative Gearing

This is where the brochure version of investing usually stops.

1. Ongoing Cash Flow Losses

You need to fund the shortfall every year.

If:

Interest rates rise

Costs increase

Your losses may grow.

2. Reliance on Property Growth

If the property doesn’t increase in value:

You’ve taken losses without upside

3. Interest Rate Risk

Higher rates → higher repayments → larger losses

This can significantly impact affordability.

4. Policy Risk

Negative gearing rules are subject to government policy.

Future changes could affect tax outcomes.

When Negative Gearing May Make Sense

You have stable, high income

You can comfortably absorb losses

You have a long-term investment horizon

You’re targeting quality assets with growth potential

When It May Not Be Suitable

You’re relying on tax savings to justify the investment

You have limited cash flow

You’re highly leveraged

You’re uncertain about long-term holding

Real-Life Scenario

Daniel (Perth, $650,000 investment property):

Rental income: $27,000

Expenses: $34,000

Loss: $7,000

Tax benefit:

~$2,500 (approx.)

Outcome:

Out-of-pocket cost: ~$4,500 per year

Strategy relies on long-term growth

Key Question: Is Negative Gearing Worth It?

Negative gearing is not inherently good or bad.

It’s simply a structure.

What matters is:

Whether the investment stands on its own merits

Whether you can sustain the cash flow

Whether it aligns with your broader financial plan

A tax deduction should never be the main reason to invest.

FAQs

1. Is negative gearing only for property?

No, but it’s most commonly used with property investments in Australia.

2. Do you always get money back from negative gearing?

No. You reduce your tax, but you still incur a net loss.

3. Can negative gearing make you rich?

Only if the underlying asset performs well over time.

4. What happens if the property becomes positively geared?

You’ll pay tax on the net income instead of claiming a loss.

5. Is negative gearing risky?

Yes. It depends on property growth and your ability to manage cash flow.

6. Can first-time investors use negative gearing?

Yes, but it should be approached carefully with proper planning.

7. Is negative gearing guaranteed to work?

No. It depends on market conditions, interest rates, and individual circumstances.

Considering Property Investment?

Negative gearing can be a useful strategy, but only when it’s part of a broader, well-structured plan.

It’s important to understand:

Your cash flow position

The risks involved

Whether the investment stands up beyond tax benefits

A structured approach can help ensure your investment decisions are driven by long-term outcomes, not short-term tax incentives.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional financial advice. Information is subject to current ATO and Services Australia rules and may change over time.