Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

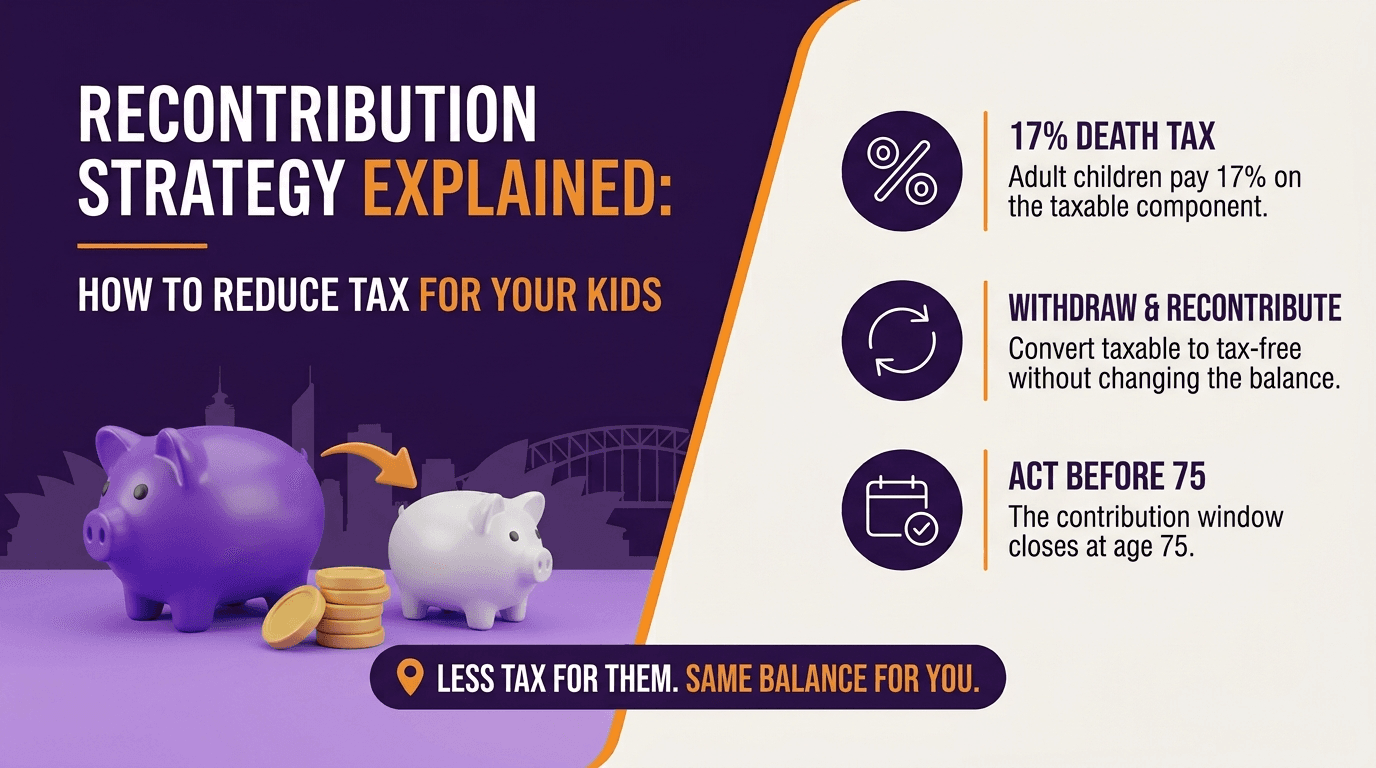

Recontribution Strategy Explained: How to Reduce Tax for Your Kids

Most Australians know that super is tax-effective during their lifetime. Fewer realise that the tax treatment of super on death depends almost entirely on who receives it and what component the money sits in.

If your super passes to a spouse or a dependent child, it is generally received tax-free. If it passes to an adult child who is financially independent, which describes most adult children, the taxable component of your super is subject to a death benefits tax of up to 17%. On a large super balance, that tax bill can run to tens of thousands of dollars that your children pay before they receive a cent.

The recontribution strategy is a legal approach to reducing that liability. By withdrawing super you can already access tax-free and recontributing it as an after-tax contribution, you convert taxable component into tax-free component. The total in your super does not change. What changes is the proportion that your children will one day inherit without paying tax on it.

This guide explains how the strategy works, who it suits, what conditions and limits apply, and what it cannot do.

TL;DR: The Key Points

Here is the short version before the detail:

When adult children inherit super, they pay up to 17% tax on the taxable component (15% tax plus 2% Medicare levy)

The tax-free component of super passes to any beneficiary, including adult children, with no tax

The recontribution strategy converts taxable component into tax-free component by withdrawing super and recontributing it as a non-concessional (after-tax) contribution

You must have met a condition of release to withdraw the money and recontribute it

The strategy is limited by the non-concessional contributions cap of $130,000 per year, or up to $390,000 using the bring-forward rule where eligible

Your total super balance affects how much you can recontribute

Those aged 67 to 74 must satisfy the work test to make personal contributions

Those aged 75 and over cannot generally make personal non-concessional contributions

The strategy does not reduce your super balance or your retirement income, it only changes the composition

Recontribution works best for those with a large taxable component, adult children as intended beneficiaries, and sufficient remaining NCC cap to make the exercise worthwhile

Jump to a Section

Why Super Is Taxed Differently on Death

The Two Components of Super Explained

How the Recontribution Strategy Works

Who Can Use the Strategy

Contribution Caps and Total Super Balance Limits

The Work Test for Those Aged 67 to 74

How Much Tax the Strategy Can Save

What the Strategy Cannot Do

Recontribution and Binding Death Benefit Nominations

Common Mistakes People Make

FAQ

Why Super Is Taxed Differently on Death

Super is not automatically part of your estate. It sits in a trust structure managed by your fund, and the trustee determines who receives it on your death, guided by your nominated beneficiaries and the rules of the fund.

The tax treatment of that payment, called a death benefit, depends on two things: who receives it, and which component of the super is being paid.

Tax dependants receive super death benefits tax-free. The ATO defines tax dependants broadly to include:

A spouse or de facto partner

A child under 18

A person in an interdependency relationship with the deceased

A person who was financially dependent on the deceased

Non-tax dependants, which in practice means most adult children, do not receive the same treatment. They pay tax on the taxable component of any super death benefit they receive.

The tax rate on the taxable component paid to a non-tax dependant from a taxed super fund is:

Component | Recipient | Tax Rate |

Tax-free component | Any beneficiary | 0% |

Taxable component (taxed fund) | Tax dependant | 0% |

Taxable component (taxed fund) | Non-tax dependant (adult child) | 17% (15% plus 2% Medicare levy) |

Taxable component (untaxed fund) | Non-tax dependant | 32% (30% plus 2% Medicare levy) |

Most Australian super funds are taxed funds. The 17% rate on the taxable component is the figure relevant to most families.

A super balance of $800,000 with a taxable component of $600,000 inherited by an adult child would generate a death benefits tax bill of approximately $102,000. The same balance with a $200,000 taxable component generates approximately $34,000. The strategy that changes that outcome is the recontribution strategy.

Bottom line: the tax your adult children pay on your super depends almost entirely on how much of it sits in the taxable component. The recontribution strategy is specifically designed to reduce that amount.

The Two Components of Super Explained

Every superannuation balance is made up of two components. Understanding the difference is essential to understanding why the recontribution strategy works.

The tax-free component consists of:

Non-concessional (after-tax) contributions you have made

Certain other amounts that entered the fund without a tax concession

This component has already been taxed before entering super. It passes to any beneficiary, including adult children, completely free of tax on death.

The taxable component consists of:

Employer contributions (Super Guarantee)

Salary sacrifice contributions

Personal contributions claimed as a tax deduction

Fund earnings that have been taxed at 15% inside the fund

This component received a tax concession on the way in. The ATO recovers part of that concession when it passes to a non-tax dependant on death.

Most people accumulate the majority of their super through employer Super Guarantee contributions and salary sacrifice. These are all concessional contributions that form part of the taxable component. Voluntary after-tax contributions, which form the tax-free component, are made less frequently.

The result is that a typical Australian approaching retirement has a super balance heavily weighted toward the taxable component. The recontribution strategy addresses this imbalance deliberately and within the rules.

What if the balance you have spent a working life building is going to cost your children six figures in tax because of how the contributions were structured along the way? The recontribution strategy exists precisely to address that outcome.

How the Recontribution Strategy Works

The mechanics are straightforward. The planning around them is where the strategy requires care.

Step 1: Withdraw a lump sum from your super.

To do this, you must have met a condition of release. The most common conditions are:

Reaching preservation age (currently 60 for those born from 1 July 1964) and retiring from the workforce

Reaching age 65, regardless of employment status

If you are aged 60 or over and have satisfied a condition of release, withdrawing from a taxed super fund is generally tax-free for Australian residents. This is the critical point that makes the strategy work: you can take the money out at zero tax cost.

Step 2: Recontribute the withdrawn amount as a non-concessional contribution.

A non-concessional contribution is an after-tax personal contribution. Because the money comes from funds already taxed (or in this case, withdrawn tax-free from super), it forms part of the tax-free component when it re-enters the fund.

Step 3: The composition of your fund changes.

The total balance is the same. You have simply withdrawn taxable component money and recontributed it as tax-free component money. The proportion of your balance sitting in the tax-free component increases. The proportion in the taxable component decreases.

Step 4: Your beneficiaries inherit a lower taxable component.

When the super eventually passes to your adult children, the death benefits tax applies only to whatever taxable component remains. Where the recontribution strategy has been applied over multiple years within the contribution limits, the taxable component can be reduced substantially.

A simple illustration:

Sarah is 63, retired, and has $700,000 in super. Her balance is:

Tax-free component: $80,000 (11%)

Taxable component: $620,000 (89%)

She withdraws $130,000 (the annual NCC cap for 2026-27) as a lump sum, tax-free, and recontributes it as a non-concessional contribution. Her balance remains $700,000 but is now:

Tax-free component: $210,000 (30%)

Taxable component: $490,000 (70%)

The death benefits tax her adult children would pay has reduced from approximately $105,400 to approximately $83,300, a saving of $22,100 from a single year's recontribution. Over multiple years, within the available caps, the saving compounds further.

Who Can Use the Strategy

The recontribution strategy is not available to everyone. Several eligibility conditions must be met simultaneously.

Condition of release: you must have already satisfied a condition of release to make the withdrawal. The most common paths are:

Preservation age (60) plus retirement: you have reached age 60 and have genuinely retired from the workforce. Returning to work after satisfying this condition does not remove your ability to access the already-withdrawn funds, but re-engaging with paid work can affect whether you are considered retired for future conditions of release decisions.

Age 65: once you reach 65, you can access super regardless of your employment status. This is the simplest condition to satisfy and requires no further action beyond reaching the age.

Age and contribution eligibility:

Those under 67 can generally make personal non-concessional contributions without restriction, subject to the contribution caps and total super balance rules

Those aged 67 to 74 must satisfy the work test (discussed below)

Those aged 75 and over are generally not able to make personal non-concessional contributions

The strategy therefore has a practical window: from the time you satisfy a condition of release (typically from age 60) to the time you turn 75. For those who retire at 60, this provides up to 15 years of potential recontribution. For those who continue working into their late 60s and do not satisfy the retirement condition until later, the window narrows.

The strategy works best for people who:

Have a large taxable component relative to their total super balance

Have adult children, rather than a spouse or dependent children, as their intended beneficiaries

Have sufficient NCC cap remaining to make meaningful reductions to the taxable component

Have a total super balance under the thresholds that reduce or eliminate the NCC cap

The strategy is less useful where:

The intended beneficiaries are a spouse or dependent children who will receive the super tax-free regardless of the component split

The total super balance is above the NCC eligibility thresholds

The remaining window before age 75 is short and the contribution cap limits restrict how much can be converted

The taxable component is already small relative to the total balance

Wondering whether the recontribution strategy suits your specific fund balance and beneficiary situation? The financial advisers at What If Advice can model the component split, the available cap, and the projected death benefits tax saving for your super. Call 1800 942 843 or email clientservices@whatifadvice.com.au.

Contribution Caps and Total Super Balance Limits

The recontribution strategy is constrained by the same contribution rules that govern all non-concessional contributions. Understanding these limits determines how quickly and how much of the taxable component can be converted.

Annual non-concessional contributions cap: $130,000

For the 2026-27 financial year, the non-concessional contributions cap is $130,000 per year, up from $120,000 in 2025-26. This is the maximum that can be recontributed in any single financial year without using the bring-forward rule.

Bring-forward rule: up to $390,000

The bring-forward rule allows eligible individuals to contribute up to three years worth of NCC cap in a single year, subject to their total super balance at the prior 30 June.

Bring-forward eligibility for 2026-27 based on total super balance at 30 June 2026:

Total Super Balance | Maximum NCC Available |

Under $1.84 million | $390,000 (3-year bring-forward) |

$1.84 million to under $1.97 million | $260,000 (2-year bring-forward) |

$1.97 million to under $2.1 million | $130,000 (1-year cap only) |

$2.1 million or more | Nil (no NCC permitted) |

These thresholds are subject to current ATO rules and indexation. Always confirm the current thresholds before making a contribution decision.

The total super balance threshold is a hard limit. Where a person's total super balance across all funds reaches $2.1 million or more, they cannot make any non-concessional contributions. The recontribution strategy is not available to them regardless of how much taxable component remains in their fund.

The strategy across multiple years: where the bring-forward rule is not used, or where the balance sits above the bring-forward thresholds, the strategy can still be executed over multiple years at $130,000 per year. A person who recontributes $130,000 per year from age 63 to age 74 (12 years) could potentially convert up to $1.56 million of taxable component into tax-free component, subject to their TSB remaining within eligibility thresholds throughout.

Timing matters. Each year's NCC cap is assessed against the total super balance at the prior 30 June. A balance that grows above a threshold during the year does not affect the current year's cap, but it will affect the following year's eligibility.

The Work Test for Those Aged 67 to 74

For Australians between age 67 and 74, personal super contributions are only permitted if the work test is satisfied during the financial year in which the contribution is made.

The work test requires: at least 40 hours of gainful employment in any consecutive 30-day period during the financial year.

Gainful employment means work undertaken for reward, either as an employee or in a self-employed capacity. Volunteer work does not count. The 40 hours must be in a continuous 30-day window, not spread across the full year.

The work test exemption: a work test exemption is available for one financial year where:

The individual satisfied the work test in the prior financial year

Their total super balance at the prior 30 June was under $300,000

They have not previously used the work test exemption

For those who retire at 65 or 66 and have a super balance under $300,000, the work test exemption may provide one additional year of NCC eligibility without needing to be employed. Beyond that, the work test must be genuinely satisfied.

For those who continue working part-time past 67, the work test is often straightforward to satisfy. A few weeks of part-time work early in the financial year can establish eligibility for contributions made later in the year.

For those who have fully retired, the work test becomes a real constraint on the recontribution strategy. Where the work test cannot be satisfied, contributions cannot be made regardless of available cap or component composition. Planning the recontribution strategy to occur while still meeting the work test, or before reaching age 67, avoids this limitation.

What if you retire at 68, fully intending to use the recontribution strategy, and discover the work test prevents you from contributing? Knowing the age and work test conditions before setting a retirement date is part of the planning.

How Much Tax the Strategy Can Save

The tax saving from the recontribution strategy depends on three variables: the size of the taxable component, the amount that can be converted within the available caps, and whether the beneficiaries are non-tax dependants.

A worked example:

David is 62 and recently retired. His super balance is $900,000, comprising:

Tax-free component: $100,000

Taxable component: $800,000

His total super balance is under $1.84 million. He is eligible for the full bring-forward NCC of $390,000.

David withdraws $390,000 from his super tax-free and recontributes it as a non-concessional contribution. His balance remains $900,000. The composition is now:

Tax-free component: $490,000

Taxable component: $410,000

Death benefits tax comparison:

Scenario | Taxable Component | Death Benefits Tax (17%) |

Before recontribution | $800,000 | $136,000 |

After one recontribution ($390,000) | $410,000 | $69,700 |

Tax saving | $66,300 |

Over subsequent years, continuing to recontribute at $130,000 per year further reduces the taxable component and the associated death benefits tax.

If David continues at $130,000 per year for a further 5 years, the additional taxable component conversion is $650,000 (subject to TSB thresholds at each year's 30 June). The cumulative death benefits tax saving, applied to the full converted amount of just over $1 million, approaches $175,000 over the combined recontribution period.

These figures do not account for fund earnings, which continue to accumulate as taxable component, or for any reduction in total super balance from drawdowns during retirement. The strategy is most effective where it is applied systematically over time rather than as a single one-off exercise.

Seeing your own numbers in David's example and want to know what your version of that saving looks like? The financial advisers at What If Advice can run the actual figures for your balance, component split, and available caps. Call 1800 942 843 or email clientservices@whatifadvice.com.au.

What the Strategy Cannot Do

Understanding the limits of the recontribution strategy is as important as understanding how it works.

It does not increase your total super balance. The withdrawal and recontribution are equal amounts. Your retirement savings are unchanged. The strategy only affects the split between components, not the total.

It does not help where the intended beneficiary is a spouse or dependent child. Tax dependants receive super death benefits tax-free regardless of the component split. Running the recontribution strategy to benefit a spouse who will receive the super on death produces no tax saving because the tax-free component treatment already applies to all super received by a spouse.

It cannot be used if your total super balance is at or above $2.1 million. At that threshold, no NCC can be made. The strategy is unavailable, and the taxable component remains regardless of its size relative to the overall balance.

It cannot fully convert a large taxable component in a short timeframe for older members. The NCC cap limits annual conversions to $130,000, or $390,000 with the bring-forward rule. A member with $700,000 in taxable component who begins the strategy at age 72 has limited time before age 75 closes the contribution window.

It does not eliminate death benefits tax entirely in most cases. Fund earnings continue to accumulate as taxable component throughout the retirement phase. Each year of fund earnings partially offsets the component conversion achieved through recontribution. The strategy reduces the taxable component, it does not reduce it to zero unless the balance is small enough to be fully converted within the available caps.

It requires cashflow to execute. The recontribution requires withdrawing cash from super and physically redepositing it. This is straightforward for most retirees who hold their super in an account-based pension or accumulation fund with liquid assets. It becomes more complex where the fund holds illiquid investments, such as direct property inside an SMSF.

Recontribution and Binding Death Benefit Nominations

The recontribution strategy addresses the tax treatment of the super that passes to adult children. It does not address whether the super actually reaches them. For that, a binding death benefit nomination is the essential companion tool.

Without a valid nomination, the trustee of the super fund exercises discretion over who receives the death benefit. In an APRA-regulated fund, that may mean a trustee who does not know your intentions distributes your super in a way you did not intend.

A binding death benefit nomination directs the trustee to pay the death benefit to specific beneficiaries. Combined with the recontribution strategy, it ensures:

The super goes to the intended beneficiaries (the binding nomination)

The tax on receipt is minimised (the recontribution strategy)

Important limitation: super cannot be nominated to pass to a non-dependant directly without going through the estate in some fund structures. Some funds only accept nominations to legal personal representatives (the estate) or tax dependants. Confirming your fund's rules around nominations is a prerequisite for any death benefit planning.

Non-lapsing versus lapsing nominations: many funds issue nominations that expire after three years. A binding nomination made in 2022 that was not renewed may have already lapsed. Reviewing the status of your current nomination, and whether it is binding and current, should be part of any estate planning review.

The recontribution strategy and a current binding nomination together form the core of super death benefit planning. Neither is complete without the other.

Want to review your current beneficiary nominations alongside your super component split? The financial advisers at What If Advice can review both and model the combined outcome for your estate. Call 1800 942 843 or email clientservices@whatifadvice.com.au.

Common Mistakes People Make

Starting the strategy too late. The window between satisfying a condition of release and turning 75 is fixed. A retiree who waits until 72 to begin the recontribution strategy has limited years and capped annual contributions. Beginning the strategy as early as possible after satisfying a condition of release maximises the amount that can be converted.

Using the bring-forward rule without checking the total super balance threshold. The bring-forward cap is determined by the TSB at the prior 30 June. A balance that has grown above the threshold since then does not affect the current year, but one that was already above the threshold at the prior 30 June means the full bring-forward is not available.

Applying the strategy when the intended beneficiary is a spouse. The strategy produces no death benefits tax saving where the super will pass to a spouse, because a spouse receives super tax-free regardless of the component split. The planning effort is better directed at the nomination rather than the component composition in that case.

Not accounting for ongoing fund earnings. Fund earnings accumulate as taxable component even while the recontribution strategy is reducing it. A plan that does not account for this may overestimate the final tax-free proportion achieved.

Failing to maintain a current binding nomination. The recontribution strategy only produces its intended outcome if the super reaches the intended adult child beneficiaries. A lapsed or non-binding nomination undermines the entire plan.

Not satisfying the work test before making contributions between 67 and 74. A contribution made without satisfying the work test is an excess non-concessional contribution with significant tax consequences. The work test must be confirmed before contributions are made in this age range.

Withdrawing and recontributing in the same financial year without checking the available cap. The withdrawal and recontribution are separate events. The contribution must not exceed the available NCC cap for the year. Exceeding the NCC cap triggers excess contribution tax that negates the benefit of the strategy.

What if a recontribution plan that was financially sound on paper fails because a binding nomination lapsed two years ago and the fund trustee exercises discretion differently from what was intended? The strategy and the nomination must work together.

FAQ

What is the recontribution strategy in super?

The recontribution strategy involves withdrawing super as a lump sum (generally tax-free for those aged 60 and over who have satisfied a condition of release) and recontributing the same amount as a non-concessional (after-tax) contribution. This converts money from the taxable component into the tax-free component without changing the total balance. The purpose is to reduce the death benefits tax that adult children pay when they inherit the super.

Why does the recontribution strategy reduce tax for adult children?

Adult children who are financially independent are non-tax dependants for super purposes. They pay up to 17% tax (15% plus 2% Medicare levy) on the taxable component of any super death benefit they receive. The tax-free component passes to them with no tax. By converting taxable component into tax-free component through the recontribution strategy, the taxable amount on which death benefits tax is calculated is reduced, directly reducing the tax bill your adult children face.

Does the recontribution strategy affect my retirement income?

No. The strategy does not change your total super balance. You withdraw and recontribute the same amount. Your income stream capacity, your account-based pension payments, and your total retirement savings are all unchanged. Only the internal composition of the fund shifts.

Can I use the bring-forward rule to speed up the recontribution?

Yes, where you are eligible. The bring-forward rule allows up to three years of non-concessional contributions in a single year, subject to your total super balance at the prior 30 June. For 2026-27, the maximum bring-forward amount is $390,000 for those with a TSB under $1.84 million. This can significantly accelerate the conversion of taxable component into tax-free component in a single financial year.

Can I use the recontribution strategy if my total super balance is above $2.1 million?

No. Where your total super balance across all funds is $2.1 million or more, you are not permitted to make non-concessional contributions. The strategy is unavailable at that balance level regardless of how much taxable component your fund holds.

Do I need to satisfy the work test to use the recontribution strategy?

If you are aged 67 to 74, you must satisfy the work test (at least 40 hours of gainful employment in any 30-day period during the financial year) to make personal super contributions, including recontributions. Those under 67 who have satisfied a condition of release can make contributions without satisfying the work test. Those aged 75 and over generally cannot make personal non-concessional contributions.

Is the recontribution strategy relevant if my super will pass to my spouse?

Generally no. A spouse who receives super as a death benefit is a tax dependant and pays no death benefits tax on any component. The recontribution strategy produces its benefit by reducing the taxable component that non-tax dependants (adult children) pay tax on. Where the super is intended to pass to a spouse, the component split does not affect the tax outcome and the planning effort is better directed elsewhere.

Does the recontribution strategy affect my Age Pension entitlement?

The recontribution strategy changes the composition of your super, not the total balance. Since the Age Pension income and assets tests assess the total value of super (not its component split), the recontribution strategy does not change your Age Pension position. The withdrawal and recontribution happen sequentially and the total super balance at any assessment date should be essentially unchanged.

What happens to the taxable component I cannot convert?

Fund earnings continue to accumulate inside your super as taxable component throughout the retirement phase. Even with an active recontribution strategy, some taxable component will persist because ongoing earnings partially offset the conversion. The strategy reduces the taxable component materially but rarely eliminates it entirely. Ongoing annual recontributions within the available cap progressively reduce it over time.

Should I combine the recontribution strategy with a binding death benefit nomination?

Yes. The recontribution strategy only produces its intended outcome if the super reaches the intended adult child beneficiaries. A binding death benefit nomination ensures the trustee pays the death benefit to the correct people. Without a current binding nomination, the trustee exercises discretion over who receives the super, and a lapsed or non-binding nomination may direct the super to a different beneficiary or into your estate in a way that changes the tax treatment. Review the nomination at the same time as reviewing the recontribution strategy.

What happens if I die partway through a multi-year recontribution plan?

Whatever component split exists in your super at the date of death is what your beneficiaries inherit, regardless of how far through a planned multi-year recontribution strategy you were. A plan to convert $500,000 of taxable component over four years that stops after year one due to death only delivers the tax benefit of that first year's conversion. This is one of the reasons starting the strategy as early as your condition of release allows, rather than treating it as a later-retirement task, matters: the earlier the plan starts, the more of the intended benefit is actually locked in before it needs to be. It is also a reason to prioritise the largest practical contributions early in the plan, such as using the bring-forward rule in year one, rather than spreading the strategy evenly and hoping for a long enough runway to finish it.

Can I use the recontribution strategy inside an SMSF, or is it only available through a retail or industry fund?

The strategy is available through both. The mechanics, withdrawing an amount you are eligible to access and recontributing it as a non-concessional contribution, work the same way regardless of fund type. The practical difference is liquidity. A retail or industry fund typically holds liquid, tradeable assets, so withdrawing and recontributing a lump sum is usually straightforward. An SMSF that holds illiquid assets, such as direct property, can make the cash mechanics harder, since the fund needs actual liquid cash available to pay out the withdrawal before the recontribution can occur. This does not prevent the strategy inside an SMSF, but it does mean cashflow planning within the fund needs to be considered alongside the contribution caps.

Is your super's component split working against your adult children's inheritance?

Most Australians have super balances heavily weighted toward the taxable component, simply because that is how employer and salary sacrifice contributions accumulate. Without deliberate action, that composition does not change on its own.

The recontribution strategy is one of the most straightforward legal tools available to reduce a foreseeable tax bill. The window to use it is defined by age and contribution caps. Starting earlier within that window always produces a better outcome than starting later.

The financial advisers at What If Advice work with Australians in Brisbane, Melbourne, and virtually across Australia to model the recontribution strategy within the context of a full retirement and estate plan, including component split, binding nominations, and the interaction with Age Pension and other income.

Call 1800 942 843 or email clientservices@whatifadvice.com.au to have the conversation before the window narrows.

Still asking what if about what your kids will actually receive from your super? That question has a specific, modelable answer. The team at What If Advice can work through it with you. AFSL 528250.

General Advice Disclaimer: This information is general in nature and does not take into account your personal financial situation, needs, or objectives. Superannuation contribution rules, death benefits tax treatment, and estate planning laws are complex and subject to change. The application of the recontribution strategy depends on your specific super balance, component split, age, total super balance thresholds, and beneficiary circumstances. You should seek advice from a licensed financial adviser before making any decisions about your super structure or estate planning. What If Advice is an Authorised Representative under Beryllium Advisers Pty Ltd, AFSL 528250.