Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

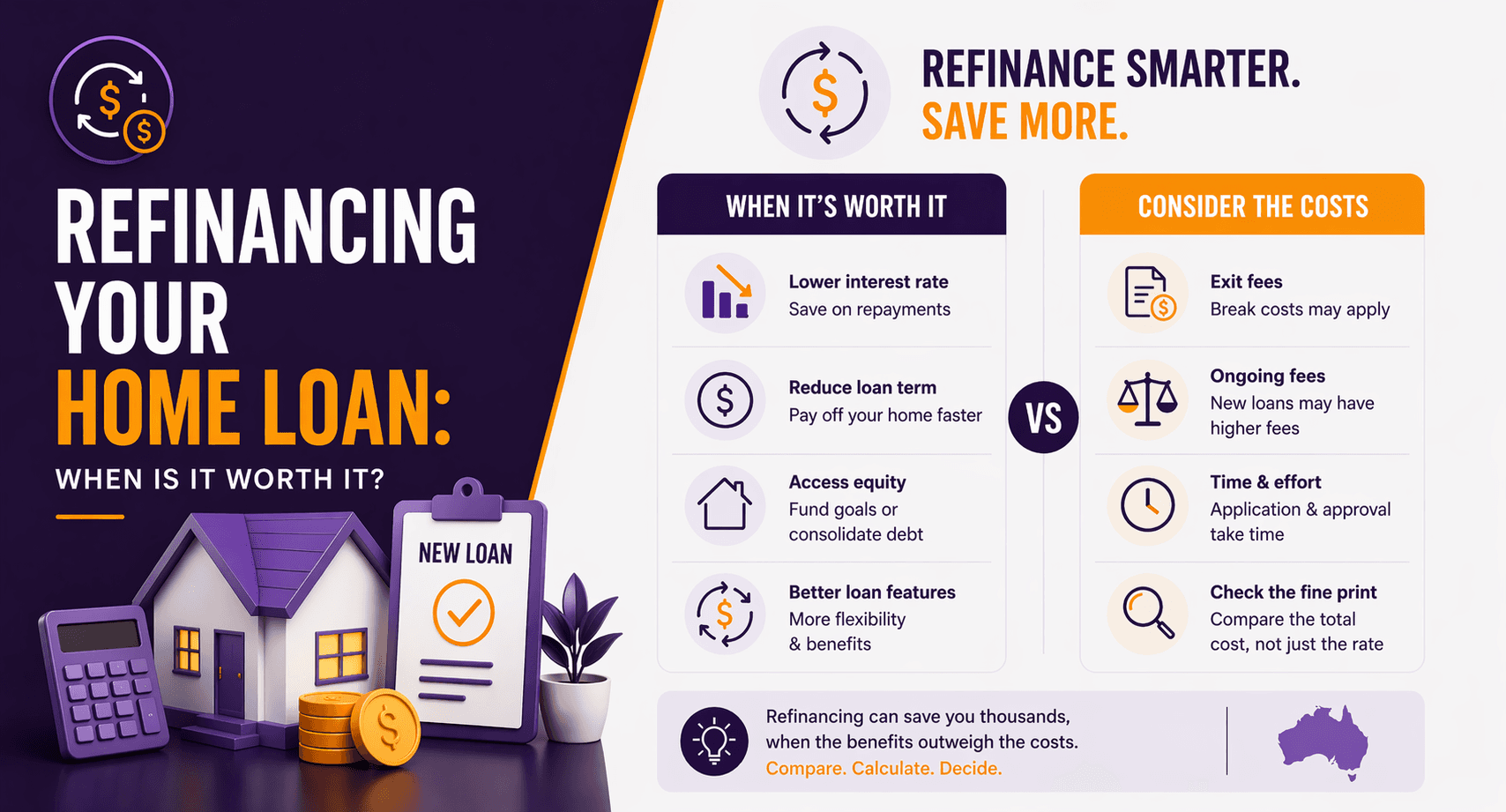

Refinancing Your Home Loan: When Is It Worth It?

Refinancing your home loan means replacing your current mortgage with a new one, either with your existing lender or a different lender.

The short answer:

Refinancing is worth it if the long-term savings or benefits outweigh the costs.

But timing and strategy matter. Done well, it can save you thousands. Done poorly, it can cost you more than you realise.

What Does Refinancing Actually Mean?

When you refinance, you:

Pay out your existing loan

Take out a new loan (usually with different terms)

This could involve:

A lower interest rate

A different loan structure

Accessing equity

The Most Common Reasons to Refinance

1. To Get a Lower Interest Rate

This is the most common reason.

Even a small rate reduction can make a big difference.

Example:

Loan: $600,000

Rate drop: 6.50% → 6.00%

Potential savings:

~$3,000 per year in interest (approximate)

~$90,000+ over 25–30 years

(Actual savings depend on loan structure and repayments.)

2. To Reduce Monthly Repayments

If cash flow is tight, refinancing to:

A lower rate

A longer loan term

can reduce your monthly commitments.

Be careful though. Extending your loan term may increase total interest paid over time.

3. To Access Equity

If your property has increased in value, you may be able to borrow against that equity.

Common uses:

Renovations

Investment property deposits

Debt consolidation

4. To Change Loan Features

You might refinance to:

Add an offset account

Enable redraw

Switch between fixed and variable

5. To Consolidate Debt

Refinancing can combine:

Credit cards

Personal loans

into your home loan at a lower interest rate.

This can improve cash flow, but it also turns short-term debt into long-term debt.

When Refinancing Is Worth It

1. You Can Get a Meaningfully Lower Rate

As a general rule, a reduction of 0.50% or more is worth investigating.

2. You Plan to Stay in the Property Long Enough

Refinancing has upfront costs.

If you sell or refinance again too soon, you may not recover those costs.

3. Your Financial Situation Has Improved

If your:

Income has increased

Credit profile has improved

You may qualify for better loan terms.

4. You’re Paying a “Loyalty Tax”

Many borrowers stay with the same lender for years and end up on higher rates than new customers.

Refinancing can correct this.

When Refinancing May NOT Be Worth It

1. High Break Costs (Fixed Loans)

If you’re on a fixed rate loan, breaking it early can trigger significant fees.

These costs depend on:

Remaining fixed term

Current interest rate environment

2. Small Interest Rate Difference

If the rate difference is minimal, the savings may not justify the costs.

3. High Switching Costs

Typical refinancing costs may include:

Discharge fees

Application fees

Valuation fees

Government charges

Quick Cost vs Benefit Check

Factor | What to Look For |

Rate difference | Ideally 0.50%+ |

Upfront costs | ~$500–$2,000+ (varies) |

Annual savings | Compare interest savings |

Break costs | Check with lender |

Time horizon | Stay long enough to benefit |

The Hidden Trap: Cashback Offers

Some lenders offer cashback deals (e.g. $2,000–$4,000).

These can be useful, but shouldn’t drive the decision.

A slightly higher interest rate can wipe out cashback benefits over time.

How to Calculate If Refinancing Is Worth It

Simple approach:

Estimate annual savings from lower interest

Subtract refinancing costs

Determine how long it takes to break even

Example:

Annual savings: $2,500

Costs: $1,500

Break-even point:

~7–8 months

If you plan to stay longer than this, refinancing may be worthwhile.

Real-Life Scenario

Mark (Sydney, $800,000 loan):

Current rate: 6.60%

New rate: 6.00%

Costs: $1,800

Estimated savings:

~$4,800 per year

Outcome:

Break-even in under 6 months

Significant long-term savings

Fixed vs Variable Consideration When Refinancing

When refinancing, you’ll also choose between:

Fixed

Variable

Split loans

Each has different implications for flexibility and risk.

(Subject to current lender offerings and market conditions.)

Key Question: Should You Refinance Your Home Loan?

Refinancing isn’t just about chasing the lowest rate.

It’s about aligning your loan with:

Your financial goals

Your cash flow

Your long-term plans

The best loan today isn’t always the best loan in two years.

FAQs

1. How often can I refinance my home loan?

There’s no strict limit, but frequent refinancing may reduce benefits due to repeated costs.

2. Does refinancing affect my credit score?

Yes, lenders will perform a credit check, which may have a temporary impact.

3. How long does refinancing take in Australia?

Typically 2 to 6 weeks, depending on the lender and complexity.

4. Can I refinance if my property value has dropped?

It may be more difficult, as your loan-to-value ratio (LVR) may be higher.

5. Is refinancing worth it for cashback offers?

Only if the long-term savings still make sense beyond the cashback.

6. Do I need a deposit to refinance?

No, but sufficient equity is usually required.

7. Can I refinance to pay off debt?

Yes, but this should be done carefully, as it may increase long-term interest.

Thinking About Refinancing Your Home Loan?

Refinancing can reduce your interest costs, improve your cash flow, or help you access equity for future opportunities.

But the wrong move can lock you into higher costs or reduce flexibility.

A structured review of your current loan, interest rate, and long-term goals can help determine whether refinancing is actually worth it.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional financial advice. Information is subject to current ATO and Services Australia rules and may change over time.