Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

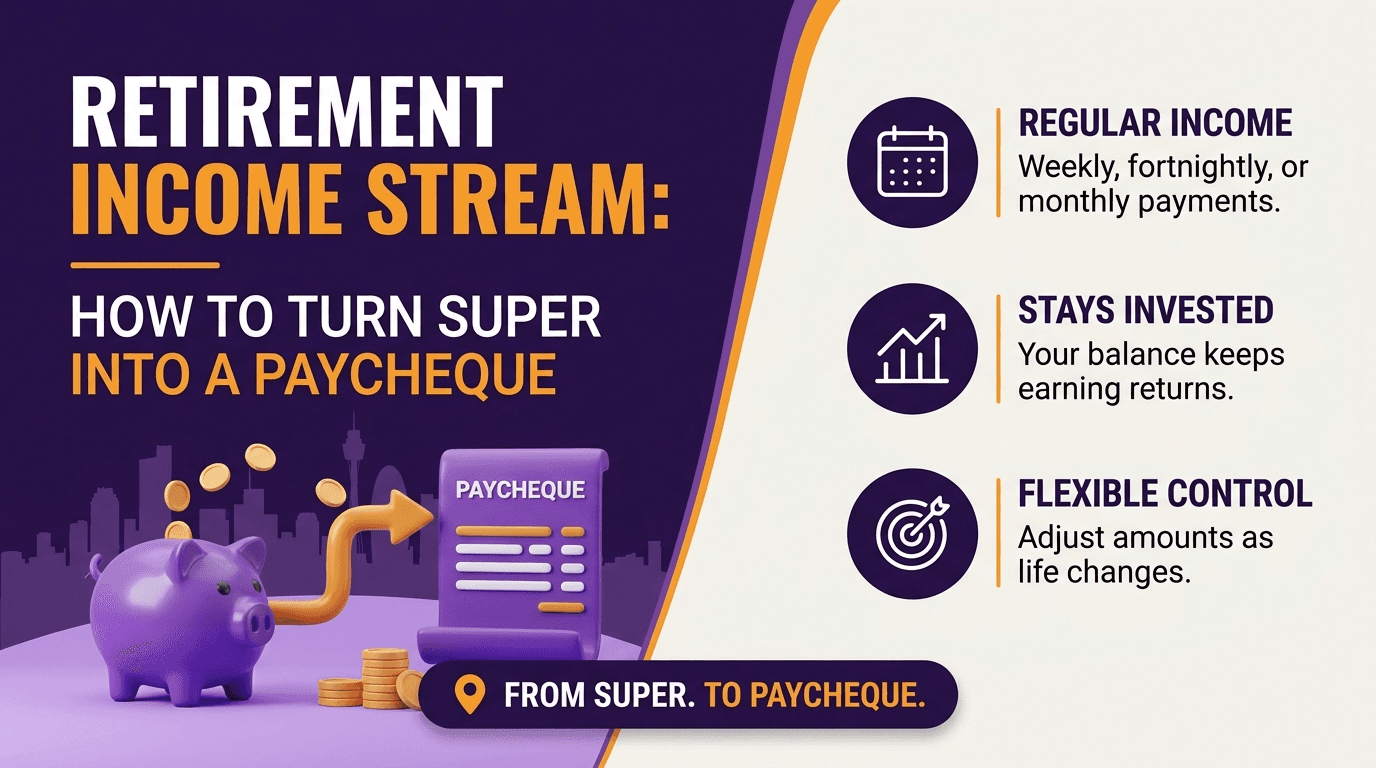

Retirement Income Stream: How to Turn Super Into a Paycheque

What if your super runs out at 84, and you still have a decade of rent, groceries, and grandkids' birthdays ahead of you? What if the drawdown decision you make in your first year of retirement quietly costs you eight years of income at the end? Most Australians spend 40 years building super and then 90 days deciding how to spend it, usually in a rush, often alone, and almost never with the structure that the next 30 years actually requires. This guide walks through exactly how to turn that balance into a regular, tax-effective, properly structured retirement paycheque.

TL;DR: The 6 Things You Need to Know

An account-based pension is the most common way Australians turn super into income. Your balance stays invested and pays you regularly

Minimum drawdown rates start at 4% under 65 and scale to 14% at age 95+

From age 60, both pension payments and investment earnings inside the pension are typically tax-free

The transfer balance cap is $2M in 2025-26, rising to $2.1M from 1 July 2026

Other options (annuities, defined benefit pensions, lump sums) each carry different trade-offs in flexibility, certainty, and tax

Most retirees combine super income with the Age Pension, and the two work best when planned together

Bottom line: Converting super into a retirement income stream is one of the most important financial decisions of your life. The right structure depends on your balance, goals, lifestyle, and other assets, and the cost of getting it wrong compounds for 25 years.

Jump to a Section

What Is a Retirement Income Stream?

How Does an Account-Based Pension Work?

What Are the Minimum Drawdown Rates for 2025-26?

Is Your Retirement Income Stream Tax-Free?

What Is the Transfer Balance Cap in 2026?

How Do You Set Up a Retirement Income Stream?

Practical Examples

What Are the Most Common Retirement Income Mistakes?

FAQ

Ready to Turn Your Super Into a Paycheque?

What Is a Retirement Income Stream?

A retirement income stream is a regular, often tax-free, income paid from your super after you retire. It replaces your salary as your primary source of cashflow.

Most Australians have more options than they realise. The right one depends on your balance, your appetite for flexibility, and how much certainty you want about future income. The main types available in Australia are:

Account-based pension. The most common option. Super stays invested in your name; you draw a regular income while the balance continues to grow or decline depending on returns and drawdowns.

Annuity. A guaranteed regular income from a life insurance company in exchange for a lump sum. Income is fixed (or indexed), but flexibility is reduced.

Defined benefit pension. Available only to members of certain government and corporate funds. Income is calculated on years of service and salary rather than account balance.

Innovative retirement income streams. Newer products such as lifetime income streams that combine some features of annuities and account-based pensions.

For most Australian retirees, the account-based pension is the central retirement income tool.

Bottom line: A retirement income stream is the structural product that converts your super balance into ongoing income. The most common is an account-based pension.

How Does an Account-Based Pension Work?

An account-based pension takes your accumulated super and moves it into a retirement phase structure. Your money stays invested, but several things change.

An account-based pension is the most common retirement structure in Australia for good reason. It balances tax efficiency with flexibility better than any other option. The key features:

Earnings inside the pension are tax-free (compared to 15% in the accumulation phase)

You must draw a minimum annual income based on your age and balance

Payments are typically monthly, quarterly, or annually, at your choice

You can withdraw lump sums in addition to regular pension payments

The pension continues as long as there is a balance

The structure provides flexibility, tax efficiency, and ongoing investment growth. The trade-off is that you carry the investment and longevity risk. If markets underperform or you live longer than expected, the balance may run out.

What if the market drops 15% in your first year of retirement? Sequencing risk, the order in which returns happen, matters more in the first five years of retirement than at any other point. A balanced drawdown strategy and a cash buffer are how directors of their own retirement plan for this.

Bottom line: Account-based pensions are the most flexible retirement income structure, with the trade-off being that you retain investment and longevity risk.

What Are the Minimum Drawdown Rates for 2025-26?

The Australian government sets minimum annual drawdown rates for account-based pensions to ensure super is used for retirement income rather than indefinite tax-free wealth accumulation.

The standard minimum drawdown rates are:

Age at 1 July | Minimum Annual Drawdown |

Under 65 | 4% |

65 to 74 | 5% |

75 to 79 | 6% |

80 to 84 | 7% |

85 to 89 | 9% |

90 to 94 | 11% |

95 and over | 14% |

The percentage is applied to your account balance at 1 July each year. For example, a 67-year-old with $600,000 at 1 July must draw at least $30,000 during the financial year (5% of $600,000).

The drawdown rules have a couple of quirks that catch people out, especially in the year they retire:

If your pension commences mid-year, the minimum is pro-rated for the remaining days in the financial year

If your pension starts on or after 1 June, no minimum drawdown is required that financial year

There is no maximum drawdown limit on a retirement-phase account-based pension. You can withdraw lump sums or increase your regular payments at any time without restriction.

What if you only draw the minimum? Many retirees treat the minimum as a target. It isn't. It's a floor. Drawing only the minimum often means underspending in the early, healthy years of retirement when you could be travelling, helping family, or simply enjoying the life you've earned.

Bottom line: Minimum drawdown rates set a floor on your annual income from super, not a ceiling. Most retirees draw close to the minimum to preserve the balance, while others draw more to fund specific goals.

Is Your Retirement Income Stream Tax-Free?

The tax treatment of super income streams is one of the most generous features of the Australian retirement system.

The tax treatment of super in retirement phase is genuinely generous, to the point where many retirees are surprised when their adviser confirms what they're actually paying. Or rather, not paying. For most Australians in a standard taxed super fund:

From age 60, both pension payments and investment earnings inside the pension are tax-free

Lump sum withdrawals from age 60 are also generally tax-free

The pension does not need to be declared as taxable income in your tax return

The pension income is still relevant to Age Pension assessment and some Centrelink calculations

For Australians under 60 (typically those drawing a TTR pension), tax treatment is more complex:

The taxable component of pension payments is taxed at marginal rates with a 15% tax offset

The tax-free component is paid free of tax

Earnings inside a TTR pension that is not in retirement phase are taxed at 15%, not tax-free

The tax efficiency from 60 onwards is one of the strongest reasons to defer non-urgent super withdrawals until at least preservation age.

Bottom line: From age 60, Australian super pensions are typically completely tax-free for both income and earnings. This is the most tax-effective income structure available to retirees.

Want to see exactly how this works with your numbers? The free Retire Ready Roundtable workshop walks through tax treatment, drawdown strategy, and Age Pension integration in 90 minutes. Brisbane, Melbourne, and online sessions available.

What Is the Transfer Balance Cap in 2026?

The amount of super that can be transferred into the tax-free retirement phase is capped. This is the transfer balance cap (TBC), and the transfer balance cap rules are one of the most important planning considerations for higher-balance members.

Key figures:

2025-26 general TBC: $2 million

From 1 July 2026: $2.1 million

Personal cap: Each individual has a personal TBC based on the highest balance they have ever held in retirement phase

Excess amounts: Stay in accumulation phase, where earnings are taxed at 15%

For couples, the cap applies per person. A couple can have up to $4.2 million combined in tax-free retirement phase (from 1 July 2026) if each fully utilises their cap.

Most Australians retire with balances below the cap and are not affected. For those approaching $2M+, the cap becomes a planning consideration, often combined with Division 296 tax on balances above $3M.

Bottom line: The transfer balance cap limits how much super moves into tax-free pension phase. For most retirees this is not a constraint; for higher-balance members it requires active planning.

How Do You Set Up a Retirement Income Stream?

The typical process for converting super into a retirement income stream involves several steps.

Confirm eligibility. You must have met a condition of release, typically meaning you have retired after preservation age (60) or reached age 65.

Select your income stream type. Most members choose an account-based pension; some combine with annuities or innovative income streams.

Choose your investment option. Your balance remains invested. Conservative, balanced, growth, and other options remain available within the pension.

Set your payment amount. Choose an annual income at or above the minimum, and select the frequency (monthly, quarterly, annually).

Make beneficiary nominations. Update binding death benefit nominations and consider reversionary pension nominations, particularly for couples. This is where estate planning for super becomes critical.

Coordinate with Centrelink. Notify Centrelink of the new income stream for Age Pension assessment if eligible. The Age Pension assets test treats account-based pensions as assessable assets.

Review annually. Drawdown amounts, investment performance, and income needs all warrant annual review.

Many Australians make their first retirement income decisions in a hurry. A structured, advised approach over 1 to 3 months produces materially better outcomes.

Bottom line: Setting up a retirement income stream is not a quick decision. Plan it carefully, ideally with professional advice.

Practical Examples

Example 1: Margaret, 67, Single Retiree with $720,000 in Super

Margaret is a 67-year-old retiring from a long career in healthcare, downsizing from her family Queenslander in Wilston into a low-maintenance apartment in Toowong to be closer to the river walks and the inner-west cafes she loves. She has $720,000 in super, a fully owned home post-downsize, and targets a comfortable retirement income of approximately $54,000 per year. A downsizer contribution topped up her super before retirement.

Her income strategy:

Convert $720,000 to an account-based pension in retirement phase

Draw 6% per year initially ($43,200), above the 5% minimum

Receive a partial Age Pension of approximately $10,800 per year initially (subject to Services Australia rules)

Total annual income: approximately $54,000, matching her target

Her balance is invested in a balanced option, projected to support her income to approximately age 90. As her balance reduces over time, her Age Pension entitlement increases, maintaining the income trajectory. Margaret reviews her pension annually with her adviser, adjusting drawdowns and investment option as her circumstances change.

Example 2: David and Linda, Both 65, Couple with $1.3M Combined Super

David and Linda are 65-year-old high school teachers from Kedron, considering a sea change to Melbourne to be closer to their grandchildren in Brunswick. David has $780,000 and Linda has $520,000 in super, totalling $1.3M. They want to retire together at 65 and target a comfortable couple income of approximately $77,000 per year.

Their strategy:

Both convert their full super balances to account-based pensions (well below the TBC)

David draws 5% ($39,000) and Linda draws 5% ($26,000) annually, totalling $65,000

Receive a partial Age Pension of approximately $12,000 combined when they reach Age Pension age at 67 (subject to Services Australia rules)

Both nominate each other as reversionary beneficiaries to ensure seamless continuation on first death

Review investment options annually, gradually shifting to slightly more conservative settings as they age

Their combined pension and Age Pension produces approximately $77,000 per year, supporting a comfortable lifestyle. Their balance is projected to support this income through to approximately age 90, with Age Pension entitlements rising as their balances reduce.

What if we ran these numbers with your actual super balance? Book a free 15-minute consultation.

What Are the Most Common Retirement Income Mistakes?

After 1,000+ client conversations, the same seven mistakes show up again and again, and each one has a specific, measurable cost.

Drawing only the minimum without considering goals. The minimum drawdown is a floor, not a target. We've sat across the kitchen table from a 78-year-old who didn't take the European trip at 67 because she was being "careful", and now isn't well enough to take it. The balance she preserved will outlive her. The trip won't come back.

Switching entirely to cash at retirement. A 65-year-old retiree has 25 to 30 years of investment horizon ahead. Modelling consistently shows that a 100% cash portfolio over 25 years can produce $200,000 to $400,000 less in total retirement income than a balanced portfolio on a $600,000 starting balance, depending on inflation. Cash feels safe. It often isn't.

Forgetting binding death benefit nominations. Without a valid binding nomination, the super fund trustee decides who receives the death benefit. The typical consequences: 6 to 12 months of administrative delays, family disputes, and tax outcomes (15% to 17% on payments to non-dependants) that a 30-minute paperwork exercise would have prevented.

Ignoring the Age Pension. Many retirees underestimate the role of the Age Pension in their long-term income. Over a 25-year retirement, an Age Pension entitlement that grows from $0 to $30,000+ per year as super reduces can represent more than $400,000 in cumulative income, easily missed by retirees who assume they're "not eligible".

Failing to coordinate with a spouse. Couples who plan independently regularly end up with the higher-balance spouse capped out at the TBC while the lower-balance spouse has untapped tax-free room. The cost is real money, often $5,000 to $15,000 per year in unnecessary tax on accumulation-phase earnings.

Drawing super lump sums without strategy. A $200,000 lump sum withdrawal at 65 to clear a mortgage can reduce Age Pension entitlement, eliminate $10,000+ per year of tax-free compounding inside the pension, and remove income flexibility for the next 25 years. Sometimes it's still the right call. Sometimes it costs $150,000+ over the retirement.

Not reviewing annually. Markets change, drawdown rates shift with age, life circumstances evolve. A retiree who set up their pension in 2018 and hasn't reviewed it once is almost certainly drawing the wrong amount from the wrong investment mix relative to today's situation.

What if you're already making one of these? Most are reversible if caught early. The mistakes that hurt most are the ones that compound silently for five years before showing up in your balance.

📞 Worried you're heading toward one of these? Our advisers in Toowong, Grange, and Melbourne can stress-test your retirement plan in 30 minutes, no cost, no obligation. Call 1800 942 843 or book online.

FAQ

How much can I take out of my super at 65? At 65 the minimum drawdown is 5% of your account-based pension balance, and there's no maximum. On a $600,000 balance that's at least $30,000 per year, but you can draw more (or take lump sums) at any time. The right amount depends on your spending needs, other income, and how long you need the balance to last.

Do you pay tax on an account-based pension after 60? For most Australians in a standard taxed super fund, no. Both the pension payments and the investment earnings inside the pension are typically tax-free from age 60, and the income doesn't need to be declared in your tax return. Tax may still apply for those drawing from certain untaxed government schemes.

Can I take a lump sum from my super pension whenever I want? Yes. Retirement-phase account-based pensions have no maximum drawdown limit, so you can take lump sums on top of your regular pension at any time, provided your balance allows. Larger lump sums can affect Age Pension entitlements, so it's worth modelling first.

What happens to my pension when I die? Depending on your nominations and the type of pension, it may continue to a reversionary beneficiary (usually a spouse), be paid as a death benefit to your nominated beneficiaries, or revert to your estate. Tax treatment depends on the beneficiary's status. Dependants typically receive death benefits tax-free, while non-dependants may pay 15% to 17% tax on the taxable component.

Is it better to take super as a lump sum or a pension? For most Australians, a pension is more tax-effective and supports longer-term retirement income. Lump sums can be useful for specific purposes such as debt repayment, home renovation, or replacing a car, but are rarely optimal as the sole retirement strategy because they remove the tax-free earnings environment.

Can I change my drawdown amount during the year? Yes. You can increase or decrease your regular pension payments at any time, provided you meet the annual minimum by 30 June. You can also take additional lump sums on top of your regular payments without restriction.

How long will $500,000 in super last in retirement? Drawing 5% per year ($25,000) on a balanced investment mix, $500,000 typically lasts 20 to 25 years before reducing significantly, often supplemented by a growing Age Pension entitlement as the balance falls. The Moneysmart account-based pension calculator can model your specific situation, and an adviser can stress-test the assumptions.

Will I lose the Age Pension if I have an account-based pension? Not necessarily. The account-based pension balance is assessed under the assets test, and the income drawn is assessed under the income test (using deeming rules for most pensions started after 1 January 2015). Many retirees with $300,000 to $900,000 in super still qualify for a partial Age Pension, and the entitlement grows as the balance reduces.

What happens if my super runs out before I die? The account-based pension ends, but your Age Pension entitlement typically increases significantly as your assets fall. For many retirees, the full Age Pension becomes available. The risk is lifestyle, not destitution: full Age Pension supports a modest, not comfortable, retirement, which is why drawdown strategy and longevity planning matter.

Ready to Turn Your Super Into a Paycheque?

If you've made it this far, you already know this isn't a decision you want to make alone, and you don't have to. WIAA has advised more than 1,000 Australians through this exact conversation, under AFSL 528250.

Three ways to take the next step:

Book a free 15-minute consultation with a retirement-focused adviser at WIAA. Call 1800 942 843 or book online. We'll talk through your numbers, your timeline, and where the biggest leverage points are.

Attend a free Retire Ready Roundtable workshop in Brisbane, Melbourne, or online. 90 minutes covering retirement income, super strategy, and Age Pension. Reserve your seat.

Email the client services team at clientservices@whatifadvice.com.au if you'd rather start with a written question. We reply within one business day.

Still asking what if about your retirement income? Let's turn the question into a plan.

General Advice Disclaimer: This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions. What If Advice is an Authorised Representative under Beryllium Advisers Pty Ltd, AFSL 528250.