Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

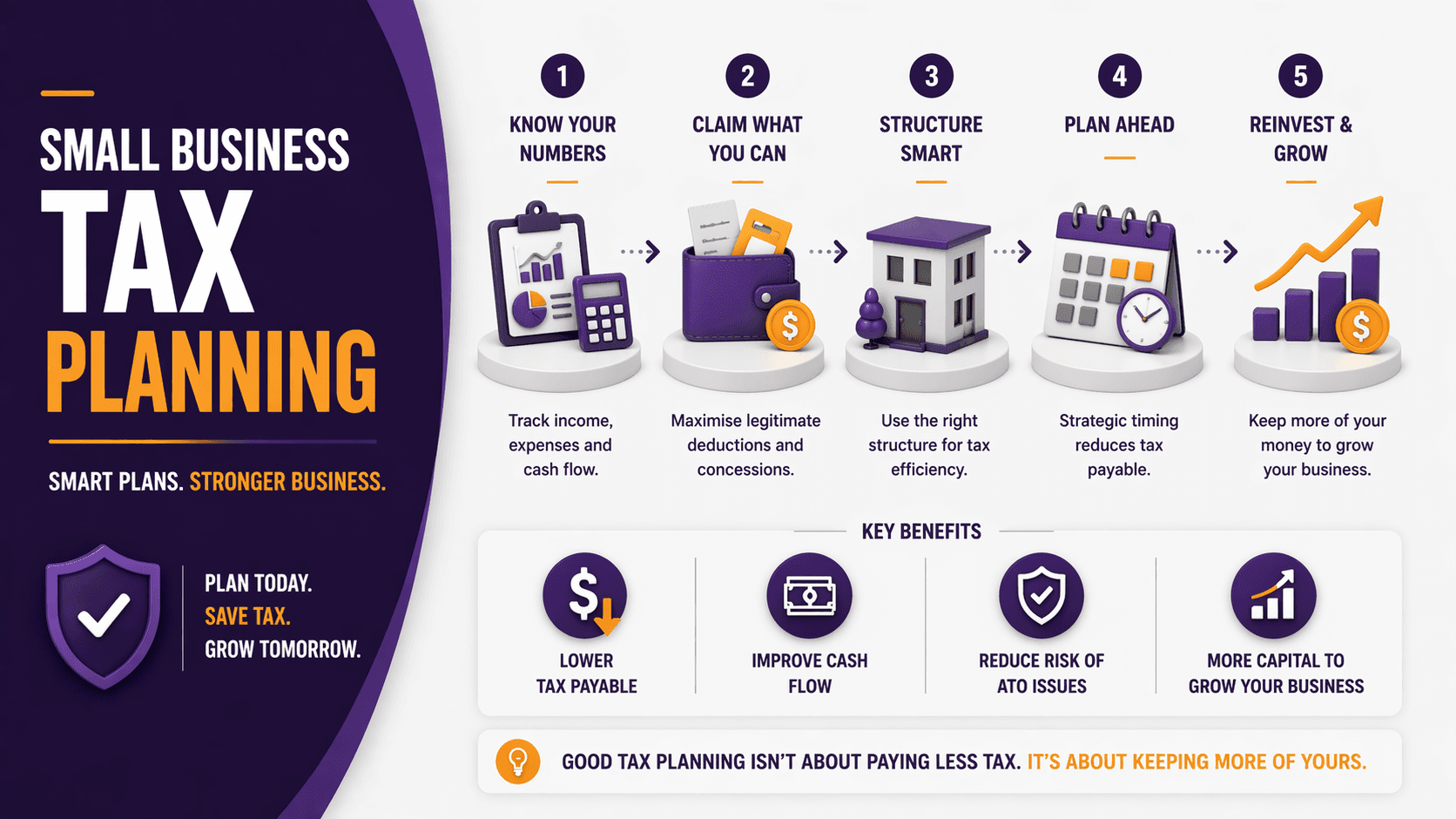

Small Business Tax Planning in Australia: Practical Strategies That Actually Work

Small business tax planning isn’t about avoiding tax. It’s about paying the right amount, at the right time, in the right structure.

Done properly, it can:

Improve cash flow

Reduce tax legally

Support long-term growth

Done poorly, it usually results in:

Last-minute stress

Missed opportunities

Unexpected tax bills

Here’s how to approach it strategically.

What Is Tax Planning (And What It’s Not)

Tax planning is:

Proactive

Structured

Ongoing throughout the year

It is not:

Scrambling in June

Guessing deductions

Hoping your accountant “fixes it later”

Why Tax Planning Matters for Small Businesses

1. Cash Flow Control

Tax is often your largest expense.

Planning helps you:

Spread liabilities

Avoid surprises

Maintain working capital

2. Lower Overall Tax (Legally)

Using the right strategies:

Timing income and expenses

Choosing the right structure

Accessing concessions

3. Better Business Decisions

When you understand tax:

You make smarter investment decisions

You avoid reactive choices

Key Tax Planning Strategies

1. Timing Income and Expenses

One of the simplest strategies.

Delay income (if appropriate) into next financial year

Bring forward deductible expenses

Example:

Invoice issued 1 July instead of 30 June

Prepay expenses before EOFY

This can shift taxable income between years.

2. Maximise Deductions

Common deductible expenses:

Equipment and tools

Software subscriptions

Professional services

Marketing costs

Also consider:

Instant asset write-off (subject to current ATO rules)

3. Choose the Right Business Structure

Different structures = different tax outcomes.

Structure | Tax Treatment |

Sole trader | Personal tax rates |

Company | Flat tax rate (typically 25%) |

Trust | Flexible income distribution |

Choosing the wrong structure can cost significantly over time.

4. Superannuation Contributions

Super can be a tax-effective strategy.

Contributions may be deductible

Helps build long-term wealth

Be mindful of:

Contribution caps (ATO rules apply)

5. Manage Company Profits Strategically

If operating through a company:

Retain profits at lower tax rate

Distribute dividends strategically

This allows:

Tax deferral

Income smoothing

6. Understand Division 7A Risks

If you take money from your company:

It must be structured properly

Otherwise:

It may be treated as a taxable dividend

7. Review GST and BAS Position

Ensure:

GST is correctly accounted for

BAS lodgements are accurate

Mistakes here can:

Create cash flow issues

Trigger ATO scrutiny

Example Scenario

Small Business Owner (Company Structure)

Profit: $180,000

Without planning:

Full profit taxed

No optimisation

With planning:

$30,000 expenses brought forward

$20,000 super contribution

Remaining profit retained

Outcome:

Lower taxable income

Improved cash flow

Structured growth

End of Financial Year (EOFY) Checklist

Before 30 June:

Review profit position

Bring forward deductible expenses

Assess asset purchases

Finalise super contributions

Review debtor and creditor timing

Check loan accounts (Division 7A)

Confirm BAS and GST position

This is where most opportunities are either captured… or missed.

Common Tax Planning Mistakes

1. Leaving It Until June

By then, your options are limited.

2. Mixing Personal and Business Finances

Creates confusion and compliance risk.

3. Overclaiming or Guessing Deductions

ATO attention is not a business goal.

4. Ignoring Structure

Structure impacts tax more than most realise.

5. No Forward Planning

Tax planning should happen year-round.

Strategic Insight: Tax Planning Is a System, Not an Event

The best businesses:

Don’t just “do tax” once a year

They build tax into their decision-making

This includes:

Forecasting

Quarterly reviews

Ongoing adjustments

When Should You Get Advice?

You should consider professional advice if:

Your business is growing

You’re generating consistent profits

You’re unsure about structure or strategy

You want to reduce tax without risk

Because:

The cost of poor tax planning is usually higher than the cost of advice.

FAQs

1. What is tax planning for small businesses?

It’s the process of legally managing your income, expenses, and structure to reduce tax and improve cash flow.

2. When should I start tax planning?

Ideally at the start of the financial year, with regular reviews throughout.

3. Can I reduce tax legally in Australia?

Yes, through deductions, timing strategies, and structuring — all within ATO rules.

4. What is the most effective tax strategy?

There is no single strategy. It depends on your business structure, income, and goals.

5. Should I operate as a company or sole trader?

It depends on your income level, risk, and long-term plans.

6. What is the instant asset write-off?

A rule allowing eligible businesses to immediately deduct certain asset purchases (subject to ATO thresholds).

7. What is the biggest tax mistake small businesses make?

Leaving tax planning until the end of the financial year.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional advice. Taxation laws and ATO rules are subject to change.