Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

Super is one of the most tax-effective ways Australians can build long-term wealth, but the rules around how much you can contribute each year are strict.

In 2025–26, the key super contribution caps you need to know are:

Concessional contributions cap (before-tax contributions)

Non-concessional contributions cap (after-tax contributions)

Bring-forward rule (for larger after-tax contributions)

Carry-forward concessional contributions (to “catch up” on unused caps)

The tricky part?

A lot of people accidentally exceed their caps because they don’t realise:

employer contributions count

salary sacrifice counts

personal deductible contributions count

contributions across multiple funds are combined

timing is based on when your fund receives the contribution (not when you send it)

This guide explains what you can contribute in 2025–26, and what happens if you exceed the caps.

Quick Definitions (So You Don’t Get Lost)

Concessional contributions (before-tax)

These are contributions made from pre-tax money or claimed as a tax deduction.

Examples:

employer Super Guarantee (SG)

salary sacrifice

personal contributions you claim as a deduction

Concessional contributions are generally taxed at 15% inside your super fund (extra tax may apply for high-income earners).

Non-concessional contributions (after-tax)

These are contributions made from money you’ve already paid income tax on.

Examples:

personal after-tax contributions

spouse contributions

Non-concessional contributions aren’t taxed when entering the fund (unless you exceed the cap).

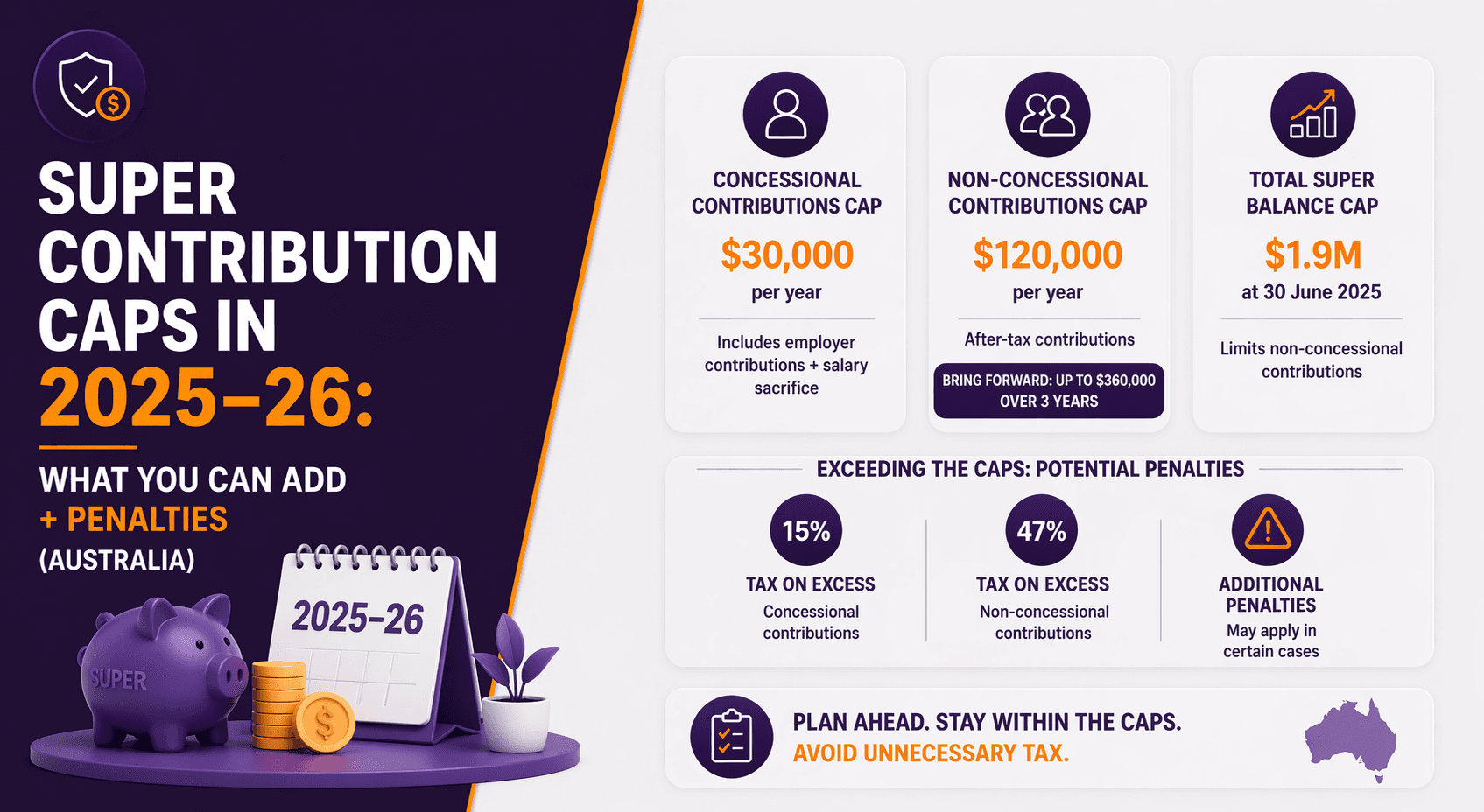

Concessional Contributions Cap (2025–26)

Concessional cap for 2025–26: $30,000

In 2025–26, the general concessional contributions cap is $30,000.

This cap includes all concessional contributions made to all your super funds combined, including:

employer SG

salary sacrifice

personal deductible contributions

Example (easy to miss!)

If your employer contributes $12,000 in SG and you salary sacrifice $20,000:

Total concessional contributions = $32,000

That’s $2,000 over the cap → may trigger excess concessional contributions assessment

Carry-Forward Concessional Contributions (Catch-Up Rule)

If you haven’t used your full concessional cap in previous years, you may be able to carry forward unused amounts, but only if you meet eligibility rules.

The ATO allows you to carry forward unused concessional cap amounts for up to five years if your total super balance is below the relevant threshold (commonly referenced as $500,000, but always check the current ATO rules).

Why this matters

This is one of the best “catch-up” strategies for Australians who:

had time out of work

were self-employed

had a high-income year and want a bigger deduction

want to boost retirement savings quickly

Non-Concessional Contributions Cap (2025–26)

Non-concessional cap for 2025–26: $120,000

In 2025–26, the non-concessional contributions cap is $120,000.

These are contributions made from after-tax money where you don’t claim a tax deduction.

Important: Not everyone can contribute after-tax

Your ability to make non-concessional contributions depends on your total super balance.

If your total super balance is too high (the ATO uses thresholds linked to the transfer balance cap), you may have a reduced cap, or no cap at all, meaning you cannot make non-concessional contributions without extra tax consequences.

Bring-Forward Rule (Non-Concessional) in 2025–26

The bring-forward rule lets eligible Australians contribute more than $120,000 in one year by “bringing forward” future years’ non-concessional caps.

Bring-forward maximum: up to $360,000

In 2025–26, if you’re eligible and trigger the bring-forward rule, you may be able to contribute up to $360,000 in one go (across a 3-year bring-forward period).

Key points:

It applies only to non-concessional contributions

You must meet age and total super balance eligibility rules

Once you trigger it, your ability to make future non-concessional contributions may be limited until the bring-forward period ends

Other Caps You Should Know (Often Overlooked)

Division 293 Tax (High Income Earners)

This isn’t a contribution cap but it is a tax penalty that applies to some concessional contributions if you earn above the threshold.

If your income plus certain concessional contributions exceed the Division 293 threshold, an extra 15% tax applies to the relevant concessional contributions (or part of them).

This means some high-income earners can pay a total of 30% tax on concessional contributions (15% contributions tax + 15% Division 293).

What Happens If You Exceed the Caps? (Penalties Explained Simply)

Exceeding contribution caps doesn’t always mean you’re “in trouble”, but it does mean the ATO will step in and adjust tax outcomes.

1) Excess Concessional Contributions (CC)

If you exceed the concessional cap:

the excess amount is generally added back to your personal taxable income

you pay tax on it at your marginal tax rate (with an offset for contributions tax already paid in super)

you can usually elect to release up to 85% of the excess from your super to pay the tax bill

In simple terms:

You lose the full tax benefit on the excess amount, and you may end up paying extra tax.

2) Excess Non-Concessional Contributions (NCC)

This is the one that can get very expensive.

If you exceed the non-concessional cap, the ATO will generally give you an option to:

withdraw the excess amount plus associated earnings (notional earnings), OR

if you don’t withdraw it, the excess may be taxed at a very high rate (often referenced around the top marginal rate, but check current rules)

Heffron notes the ATO usually assumes you want the excess refunded to avoid the harsher tax treatment, but you still need to act within timeframes.

In simple terms:

Excess after-tax contributions can trigger major tax consequences if not handled properly.

Why People Accidentally Exceed Their Caps (Common Scenarios)

1) Employer SG + salary sacrifice = over the cap

People often salary sacrifice without checking how much employer SG counts toward the same concessional cap.

2) Multiple funds

If you have two super funds, the caps apply across both combined, not separately.

3) Late June contributions processed in July

A contribution counts in the financial year when your fund receives it, not when you transfer it.

4) Personal deductible contributions without planning

If you make a large contribution late in the year and claim a deduction, it can exceed your concessional cap quickly.

5) Bring-forward rule triggered accidentally

Contributing above $120,000 can trigger the bring-forward rule automatically (if eligible), limiting future contribution flexibility.

Practical Checklist: How to Stay Within the Rules (2026)

Here’s a simple way to avoid cap problems:

Before you contribute:

Check your employer SG amount for the year

Check any salary sacrifice you’ve already done

Check if you’ve made deductible contributions

Check your total super balance (important for NCC eligibility)

Confirm what year the fund will receive the contribution

Keep a buffer under the cap if you’re close

Speak to an accountant or adviser before making a large lump sum contribution

Key Takeaways (Quick Summary)

Concessional cap in 2025–26 is $30,000 (includes SG + salary sacrifice + deductible contributions)

Non-concessional cap in 2025–26 is $120,000 (after-tax contributions)

Bring-forward rule may allow up to $360,000 (eligibility applies)

Carry-forward concessional caps may allow catch-up contributions (eligibility applies)

Exceeding caps can trigger extra tax, admin and forced withdrawals

Non-concessional cap breaches can be particularly costly if not managed

FAQ

1) What is the concessional contributions cap for 2025–26?

The general concessional contributions cap for 2025–26 is $30,000, including employer SG, salary sacrifice and personal deductible contributions.

2) What is the non-concessional cap for 2025–26?

The non-concessional contributions cap for 2025–26 is $120,000, subject to eligibility and total super balance rules.

3) How much can I contribute using the bring-forward rule?

If eligible and triggered, you may be able to contribute up to $360,000 in non-concessional contributions across a bring-forward period.

4) What happens if I exceed the concessional cap?

The excess is generally added to your personal taxable income and taxed at your marginal tax rate (with a credit for contributions tax already paid), and you may be able to release funds from super to pay the bill.

5) What happens if I exceed the non-concessional cap?

You’ll usually be prompted to withdraw the excess (and notional earnings) to avoid high tax consequences on the excess amount.

Super contribution caps are one of the easiest areas to get wrong; especially when employer contributions, salary sacrifice and personal top-ups are all happening at once.

If you’re planning to:

salary sacrifice heavily this year

make a large personal contribution

contribute a lump sum from savings or an asset sale

use bring-forward or carry-forward rules,

getting the timing and caps right can save you thousands in avoidable tax and admin.

Still asking “what if” about your finances?

That’s exactly where clarity begins.

Whether you’re planning ahead, growing wealth, or simply want confidence in your financial decisions, the advisers at What If Advice can help you turn questions into a clear, personalised plan.

👉 Book a free 15-minute strategy session or get in touch today at

whatifadvice.com.au

General Advice Disclaimer

This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions.