Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

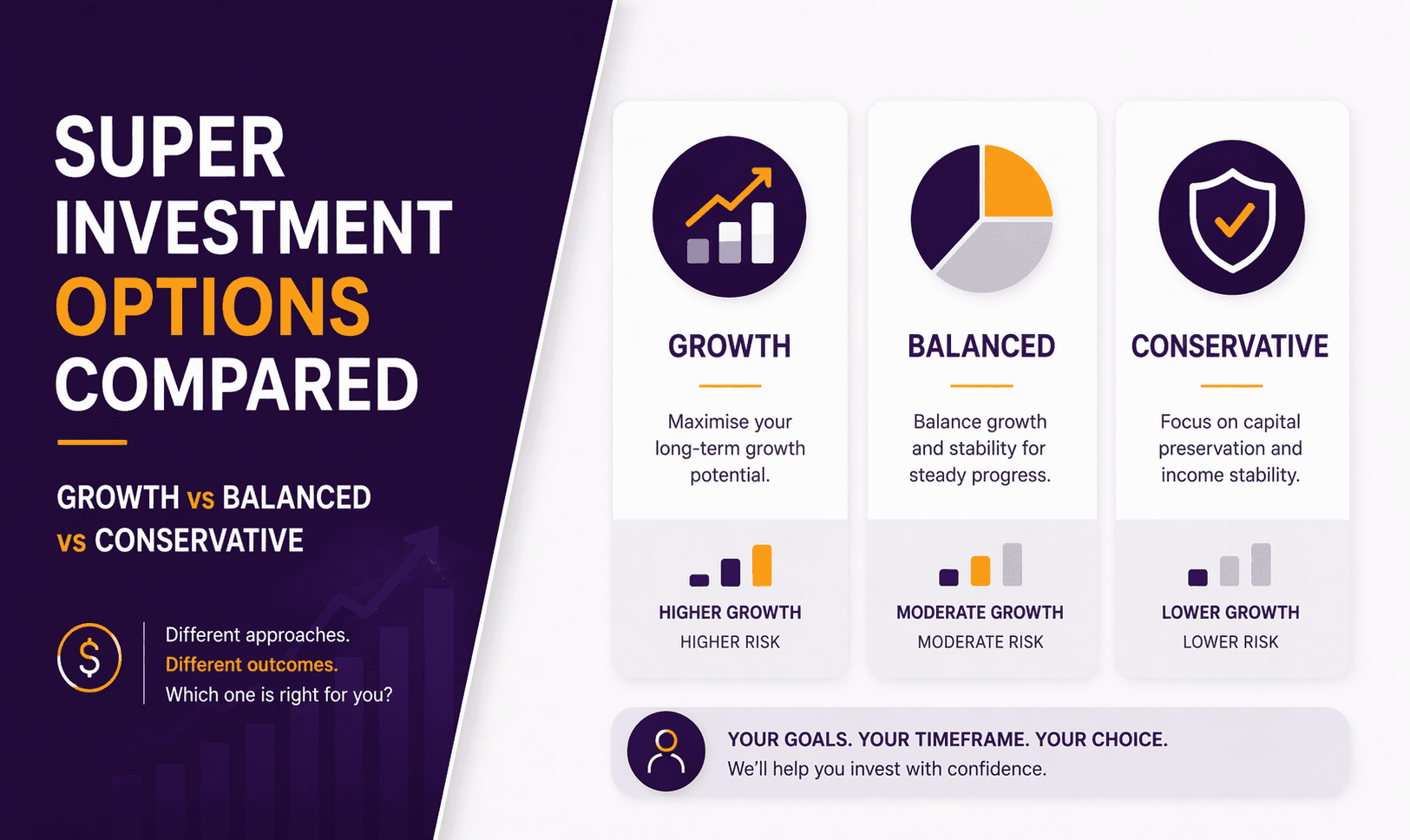

Super Investment Options Compared (Growth vs Balanced vs Conservative)

Your superannuation is likely one of your largest long-term assets. Yet many Australians never review how it is invested.

Most super funds offer three core investment options:

Growth

Balanced

Conservative

Each option has a different mix of shares, property, fixed interest and cash. The right choice depends on your time horizon, risk tolerance and retirement goals.

Here’s how they compare.

What Are Super Investment Options?

When you join a super fund, your money is invested across different asset classes.

The mix of assets determines:

Potential returns

Volatility (ups and downs)

Risk of short-term losses

Long-term growth potential

Super funds typically categorise options based on the percentage allocated to growth assets (like shares and property).

Growth Super Option

Typical Asset Allocation

70–90% growth assets (Australian & global shares, property)

10–30% defensive assets (bonds, cash)

Who It Suits

Younger members (20+ years to retirement)

Investors comfortable with market volatility

Those seeking higher long-term growth

Risk & Return Profile

Growth options can deliver stronger long-term returns, but they experience larger market swings.

For example:

During market downturns, balances may fall 10–20% or more in a short period.

Over 10–20 years, they historically tend to outperform conservative options (though past performance does not guarantee future results).

Key Advantage

Higher potential retirement balance over decades.

Key Risk

Short-term volatility can be significant.

Balanced Super Option

Typical Asset Allocation

50–70% growth assets

30–50% defensive assets

Who It Suits

Mid-career professionals

Those within 10–15 years of retirement

Investors seeking moderate growth with lower volatility

Balanced options aim to smooth returns while still delivering growth above inflation.

Risk & Return Profile

Balanced options:

Typically fall less during downturns compared to Growth.

Deliver moderate long-term returns.

They are often the default option for many super funds.

Conservative Super Option

Typical Asset Allocation

20–40% growth assets

60–80% defensive assets (bonds, cash)

Who It Suits

Retirees drawing income

Members with low risk tolerance

Those needing short-term capital stability

Conservative options prioritise capital preservation over growth.

Risk & Return Profile

Smaller fluctuations in value.

Lower long-term return potential.

Higher risk of losing purchasing power to inflation over time.

Quick Comparison Table

Feature | Growth | Balanced | Conservative |

Growth Assets | 70–90% | 50–70% | 20–40% |

Volatility | High | Medium | Low |

Long-Term Return Potential | High | Moderate | Low |

Suitable For | Long time horizon | Mid-term horizon | Short-term stability |

The Real Risk: Inflation

Many Australians choose Conservative options thinking they are “safer.”

However, if you are 40 and invested too conservatively for 25 years, the real risk is not market volatility, it’s insufficient growth.

Inflation reduces purchasing power over time. If your super does not grow above inflation after fees and tax, your retirement standard of living may suffer.

How to Choose the Right Super Investment Option

Instead of focusing only on market risk, consider:

1. Time to Retirement

20+ years: Growth may be appropriate.

10–15 years: Balanced may suit.

0–5 years: More defensive allocation may reduce volatility risk.

2. Risk Tolerance

Can you tolerate seeing your balance fall temporarily?

If a 15% drop would cause panic and poor decisions, a slightly more balanced option may be better.

3. Retirement Income Plan

Your super investment choice should align with your broader retirement income plan, not exist in isolation.

4. Other Assets

If you own investment property or shares outside super, your overall risk exposure may already be high.

What About High Growth Options?

Some funds offer “High Growth” (90%+ shares).

These are typically suited only to:

Very long investment horizons

Investors with high risk tolerance

Members who understand volatility

They are not appropriate for most retirees drawing income.

Common Mistakes Australians Make

Never reviewing their default option

Switching to Conservative after a market fall

Ignoring fees and performance consistency

Not aligning super investments with retirement strategy

Overreacting to short-term market movements

Super is a long-term investment vehicle. Short-term decisions can significantly impact long-term outcomes.

When to Review Your Super Investment Strategy

Review your allocation when:

You change jobs

You are within 10 years of retirement

Market conditions shift significantly

Your personal circumstances change

You start planning retirement income

Annual reviews are prudent.

FAQs

1. Which super investment option gives the highest returns?

Growth options typically have higher long-term return potential, but also higher volatility.

2. Is a Balanced super fund safe?

Balanced options reduce volatility compared to Growth but still experience market fluctuations.

3. Should I move to Conservative before retirement?

Not necessarily. Many retirees still need growth exposure to manage longevity and inflation risk.

4. Can I switch super investment options?

Yes. Most super funds allow members to switch investment options, though processing times vary.

5. Does the Age Pension affect my investment choice?

Indirectly. Your super balance affects Age Pension eligibility under Services Australia asset and income tests.

6. How often should I review my super allocation?

At least annually or when major life changes occur.

Align Your Super with Your Long-Term Strategy

Choosing between Growth, Balanced and Conservative is not about guessing the market. It is about aligning your super investment strategy with your retirement objectives, risk tolerance and time horizon.

At What If Advice, we help Australians structure super investments within a comprehensive retirement plan, considering Age Pension rules, tax implications and long-term sustainability.

If you are unsure whether your super is positioned correctly, seek professional advice before making changes.

Book a superannuation strategy review with What If Advice.

General Advice Disclaimer

This article provides general information only and does not consider your personal objectives, financial situation or needs. Before making any financial decisions, consider whether the information is appropriate for your circumstances and seek personal advice from a licensed financial adviser. Superannuation, taxation and Age Pension rules are subject to change under current ATO and Services Australia regulations.