Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

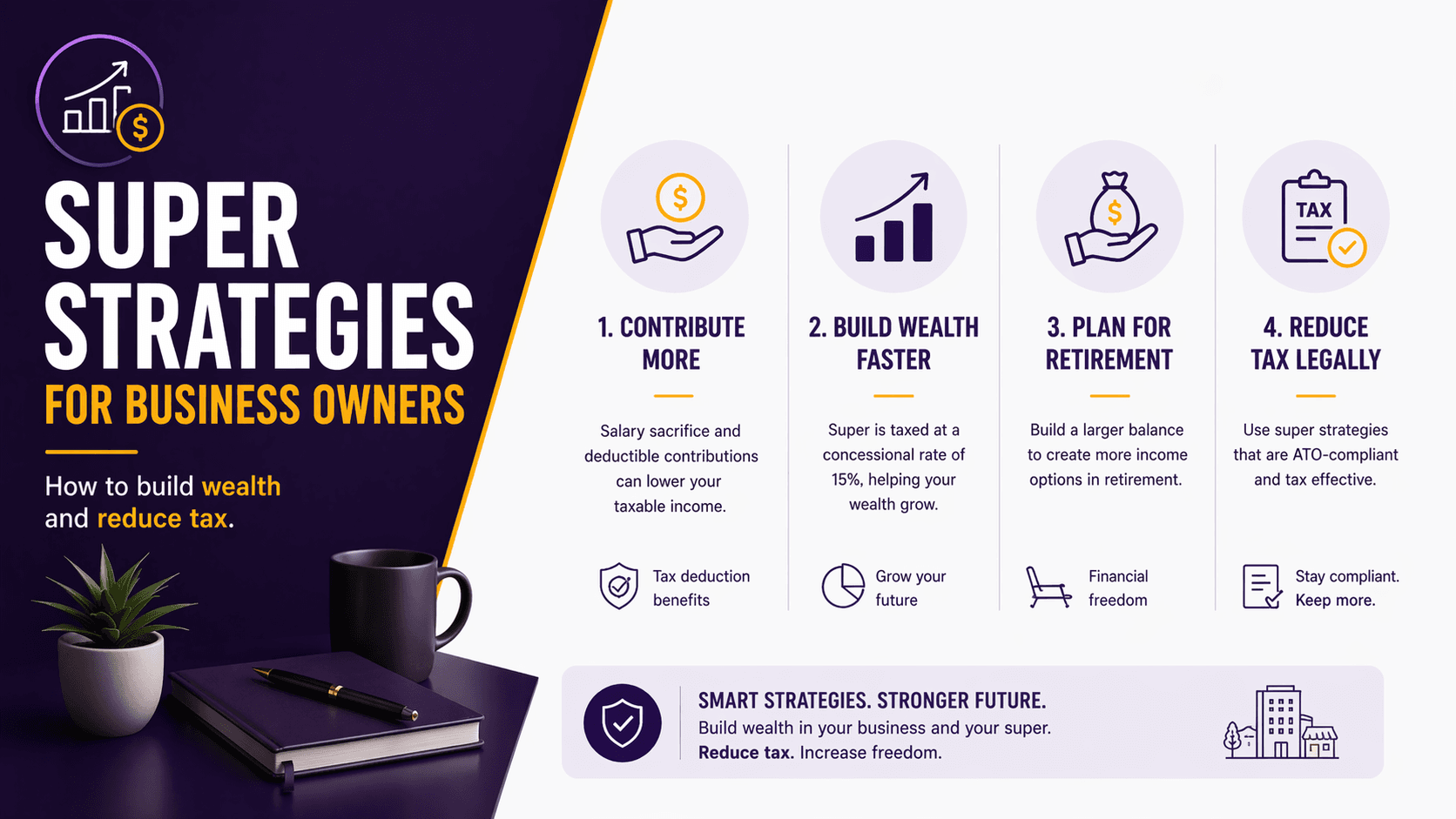

Introduction

Running a business often means your income is irregular, your time is stretched, and “retirement” feels like a future problem. But superannuation can be one of the most effective long-term wealth tools available to business owners, because it’s structured for investing over decades and can offer tax advantages, subject to current ATO rules.

The catch? Business owners commonly miss out because they prioritise the business, pay themselves inconsistently, or assume super is only for employees. The right approach depends on your structure (sole trader, company, trust), your cash flow, and how close you are to retirement.

This guide explains practical super strategies to consider, the common traps, and what to discuss with your accountant and adviser.

Quick answer: what are the best super moves for business owners?

For many business owners, the best starting points are:

Pay super consistently (even if income varies) and treat it like a non-negotiable bill

Maximise the right type of contributions for your situation (concessional vs non-concessional), subject to caps and eligibility

Consider spouse strategies if one partner has lower income

Review whether an SMSF is genuinely suitable (it’s not just about property)

Coordinate super with business structure, profit distribution, and future exit planning

Why do business owners need a different super plan?

Business income can be lumpy, and business owners often build wealth inside the business rather than in super. That can create risk:

Concentration risk (wealth tied to one business/industry)

Liquidity risk (hard to “sell down” the business when you need income)

Missed tax planning opportunities (contributions left too late)

A good plan spreads wealth across the business, super, and personal assets, while keeping cash flow realistic.

How can super reduce tax for business owners (legally)?

Super can be tax-effective because, under current ATO rules:

Concessional (pre-tax) contributions are generally taxed at a lower rate than many people’s marginal tax rate

Investment earnings in super may be taxed concessionally compared with personal names

Different tax treatment can apply when you move to retirement phase, subject to eligibility

However, extra tax may apply for higher-income earners (for example, Division 293), and contribution rules are strict. The “tax win” only works if contributions are correctly classified, recorded, and paid on time.

What contribution strategies should business owners consider?

1) Director/owner super: set a system, not a guess

If you operate a company and pay yourself wages, super guarantee obligations may apply to you as an employee/director, subject to current rules. Even where not strictly required, a scheduled contribution plan helps you:

Smooth cash flow

Avoid last-minute mistakes

Build investable assets outside the business

Practical tip: automate payments where possible, and review quarterly.

2) Personal deductible contributions (often useful for sole traders)

Many self-employed people can claim a tax deduction for personal super contributions, subject to eligibility and ATO processes (including valid notices). This can be helpful when:

Profit is higher than expected late in the year

You want flexibility versus fixed payroll

Your accountant can help ensure the deduction is claimed correctly and within deadlines.

3) Use carry-forward concessional contributions (when eligible)

Some people can “catch up” on unused concessional cap amounts from previous years, subject to eligibility criteria and current ATO rules. This may suit business owners with variable profits, for example after a strong trading year or a one-off contract.

Key risk: it’s easy to accidentally exceed caps if you don’t track employer, salary sacrifice, and personal deductible contributions together.

4) Non-concessional contributions for surplus cash

When the business has a strong year, some owners consider after-tax (non-concessional) contributions to build retirement savings faster, subject to caps and eligibility (including age-related rules).

This can be effective where:

You want to invest personally but prefer the super environment

You’ve already optimised concessional contributions

5) Spouse contributions and contribution splitting

If one partner earns less (or is out of the workforce), spouse strategies can help balance retirement savings and may provide tax outcomes, subject to current rules. Options can include:

Spouse contributions (where eligible)

Splitting certain concessional contributions to a spouse

Balancing super can also improve flexibility later; especially if one partner is likely to stop work earlier.

Should a business owner set up an SMSF?

An SMSF can be a good fit for some business owners, but it’s a compliance-heavy structure and not automatically “better” than an industry or retail fund.

When an SMSF may be worth exploring

You want more control over investment strategy and administration

You have the time (or support) to run it properly

Your balance is high enough to justify costs and complexity

Your strategy goes beyond a single asset (diversification still matters)

Common SMSF Traps for Business Owners

Purchasing property without a clear liquidity plan to cover ongoing expenses such as accounting fees, audit costs, insurance premiums, maintenance, and future pension payments.

Mixing business and personal use of SMSF assets. Strict rules apply, particularly around related-party transactions and arm’s-length arrangements.

Underestimating the administrative burden, annual audit requirements, and potential penalties for breaches of superannuation law.

If you are considering establishing an SMSF, it is important to obtain professional advice on suitability, setup and ongoing costs, and your responsibilities as a trustee.

Can I buy my business premises in super?

In limited circumstances, an SMSF may be able to purchase commercial property and lease it to your business at market rates, subject to current ATO rules (including related-party and sole-purpose tests). This can be attractive because it separates the property asset from the trading business.

Important considerations:

The SMSF must follow strict leasing and valuation requirements

Borrowing rules are complex and highly regulated

Concentrating super in one property can increase risk

This is an area where coordinated advice (SMSF specialist + accountant + adviser) matters.

What are the biggest mistakes business owners make with super?

Treating super as optional and only contributing in “good years”

Missing payroll and super payment timing requirements

Accidentally exceeding contribution caps due to multiple contribution sources

Over-focusing on tax and ignoring investment strategy, insurance, and risk

Leaving everything in the business and planning to “sell it one day”

A simple, consistent plan usually beats a clever strategy executed poorly.

FAQs

1. Do business owners have to pay themselves super?

It depends on how you’re paid and your business structure. For example, company directors on wages may have super guarantee obligations, subject to current ATO rules. Sole traders typically don’t pay SG to themselves, but can still contribute to super.

2. Is salary sacrifice worth it if my income changes month to month?

It can be, but you may need a flexible arrangement. Some owners use a base salary sacrifice and then top up with personal deductible contributions when profits are known, subject to contribution caps and eligibility.

3. Can I contribute to super right before EOFY and claim a deduction?

Often yes for eligible personal contributions, but timing and paperwork matter, and funds must be received by the super fund by required deadlines. Confirm with your accountant and the fund well before 30 June.

4. Will extra tax apply if my income is high?

Potentially. Higher-income earners may pay additional tax on concessional contributions (for example, Division 293), subject to current ATO rules. It’s worth modelling the outcome before making large contributions.

5. Should I prioritise paying down business debt or putting more into super?

It depends on interest rates, cash flow stability, risk, and your time frame. Many owners use a blended approach: maintain liquidity, manage debt, and build super steadily so retirement savings aren’t entirely dependent on the business.

Conclusion

Super doesn’t need to be complicated, but it does need to be deliberate; especially for business owners. Consistent contributions, the right mix of strategies (including spouse and catch-up options), and a clear view of your business exit plan can help you build wealth outside the business and potentially improve tax outcomes, subject to current ATO rules.

Want a clearer plan that fits your structure and cash flow? Book a What If Advice business owner super strategy session to review contributions, fund structure, and how super fits with your broader business and personal wealth plan.

General advice disclaimer: This article provides general information only and does not take into account your objectives, financial situation, or needs. Consider whether it’s appropriate for you and seek personal advice from a licensed financial adviser and/or registered tax professional before acting. Rules are subject to current ATO / Services Australia requirements.