Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

Retirement should be a time of freedom, not financial stress.

But many Australians make avoidable mistakes that can:

reduce their super faster than expected

trigger unnecessary tax

reduce Age Pension eligibility

create cash flow anxiety

or leave them financially vulnerable later in life

The problem isn’t usually a lack of effort, it’s a lack of clarity.

Here are the 7 most common retirement planning mistakes Australians make, and how to avoid them.

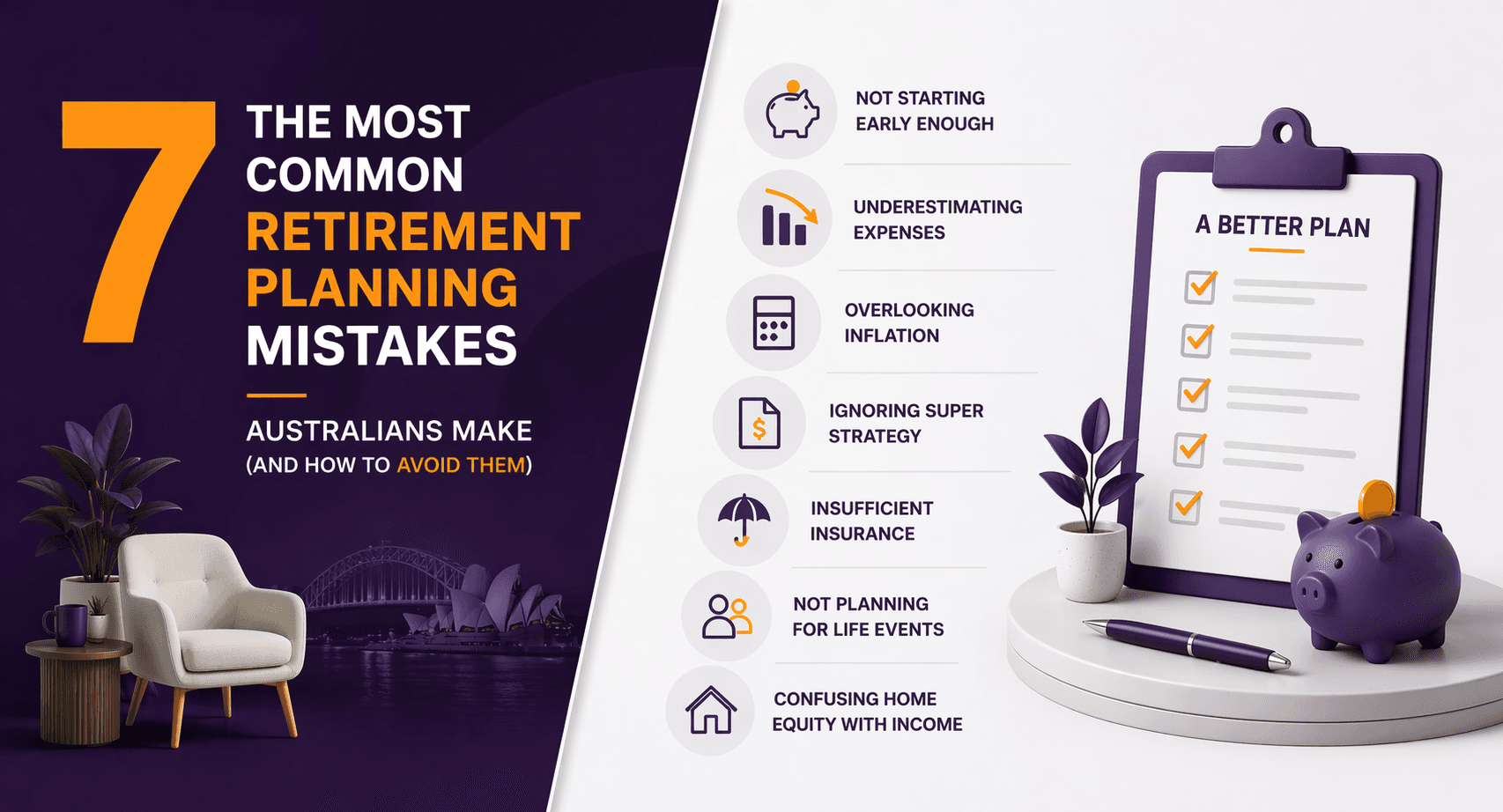

1) Underestimating How Long Retirement Will Last

One of the biggest mistakes? Planning for a short retirement.

If you retire at 60 and live to 90, that’s 30 years your super needs to last.

Many people plan for:

15–20 years

then run into problems later.

Why this is risky

Medical costs can rise with age

Investment returns aren’t guaranteed

Inflation quietly erodes purchasing power

Aged care costs may apply later

How to avoid it

Model retirement to age 90+

Build in a buffer

Review drawdown rates regularly

Avoid aggressive early withdrawals unless planned

2) Assuming “The Age Pension Will Cover Me”

The Age Pension is a valuable safety net, but it’s not designed to fund a high-comfort lifestyle.

Many Australians misunderstand:

how the assets test works

how the income test applies

how super affects eligibility

And pension rules can change over time.

Why this is risky

You may not qualify for the full pension

You may only receive a part pension

You may lose eligibility if assets increase

How to avoid it

Understand both income and assets tests

Don’t rely solely on pension assumptions

Plan retirement income independently first

Treat the Age Pension as a supplement, not a strategy

3) Accessing Super Without a Withdrawal Strategy

Reaching preservation age doesn’t mean you should withdraw randomly.

Common mistakes include:

taking large lump sums without modelling

drawing too much too early

switching to overly conservative investments

not understanding tax components

Why this is risky

You can reduce long-term growth

You may create avoidable tax

You increase the chance of running out of money

How to avoid it

Decide between lump sum vs pension strategy

Understand minimum drawdown rules

Review your super’s investment mix in retirement

Model multiple drawdown scenarios

Retirement isn’t just about accessing super, it’s about managing it properly.

4) Ignoring Inflation

Inflation quietly erodes retirement income over time.

$60,000 today won’t buy the same lifestyle in 15–20 years.

If your super is invested too conservatively for too long, it may not keep up with inflation.

Why this is risky

Spending power declines

Healthcare and aged care costs rise

Lifestyle gradually shrinks

How to avoid it

Keep some growth exposure in retirement

Review investment strategy annually

Plan for rising costs, not static expenses

Retirement portfolios still need growth, just balanced with risk management.

5) Not Reviewing Super Structure Before Retirement

Many Australians reach retirement age and still:

have multiple super accounts

pay unnecessary insurance premiums

have outdated beneficiaries

haven’t reviewed their investment options

Why this is risky

Fees erode returns

Insurance may no longer be needed

Estate planning can become messy

Investment strategy may not match retirement goals

How to avoid it

Consolidate super (if appropriate)

Review insurance inside super

Update binding death benefit nominations

Review asset allocation before retirement

A “set and forget” super strategy doesn’t work at retirement.

6) Forgetting About Healthcare and Aged Care Costs

Retirement planning often focuses on travel and lifestyle, not healthcare.

Later-life expenses can include:

increased medical costs

private health premiums

home care

residential aged care

These costs can significantly affect retirement income.

Why this is risky

You may underestimate required savings

Sudden health changes can strain cash flow

Family may need to step in financially

How to avoid it

Build a contingency buffer

Understand how aged care funding works

Factor health-related expenses into retirement modelling

Review insurance options before retirement

7) Not Having a Clear Retirement Income Plan

This is the biggest mistake of all.

Many people retire with:

a super balance

no structured income plan

no spending strategy

no tax planning

no Centrelink modelling

They simply “draw what feels right.”

Why this is risky

Inconsistent income

Anxiety about running out

Overdrawing in strong markets

Under-spending out of fear

How to avoid it

A proper retirement income plan should cover:

expected annual spending

income sources (super, pension, investments)

drawdown strategy

tax position

Centrelink impact

investment allocation

estate planning

Retirement should feel controlled, not uncertain.

Bonus Mistake: Relying Only on Business Sale or Property

Many Australians assume:

“I’ll just sell the business.”

or

“The house will sort it out.”

But:

Business sale values can fluctuate

Property markets move

Timing isn’t always perfect

Liquidity matters

Diversification matters in retirement, super provides structure and tax effectiveness that business equity alone doesn’t.

What Smart Retirement Planning Looks Like

Avoiding these mistakes usually means doing five things well:

1) Clear retirement goals

What lifestyle do you actually want?

2) Realistic budgeting

Separate essentials from discretionary spending.

3) Structured income plan

Decide how super will be accessed and invested.

4) Centrelink awareness

Understand how the assets and income tests affect you.

5) Regular reviews

Retirement planning is not a one-time event.

Key Takeaways

Plan for a long retirement (30+ years is common)

Don’t rely solely on the Age Pension

Create a structured super withdrawal strategy

Account for inflation and healthcare costs

Review super accounts and investment structure before retiring

Build a retirement income plan, not just a retirement balance

Regular reviews reduce risk and increase confidence

FAQ (5 Questions with Short Answers)

1) What is the biggest retirement planning mistake?

Not having a structured retirement income plan. A balance without a strategy creates uncertainty.

2) How much should I withdraw from super each year?

It depends on your age, super balance, lifestyle and longevity assumptions. Many planners use conservative drawdown rates to reduce the risk of running out.

3) Does the Age Pension replace super?

No. The Age Pension is designed as a safety net, not a full lifestyle replacement.

4) Should I invest conservatively once I retire?

Not necessarily. Most retirees still need some growth exposure to manage inflation risk.

5) How often should I review my retirement plan?

At least annually, and whenever there’s a major life or financial change.

Conclusion

Retirement planning mistakes are rarely dramatic, they’re usually small oversights that compound over time.

The good news?

Most of them are avoidable with clear modelling and structured advice.

If you’re approaching retirement or already retired, it’s worth asking:

Do I have a proper income plan?

Am I relying on assumptions?

Have I stress-tested my super?

Do I understand how Centrelink fits into the picture?

Want to avoid these mistakes and retire with confidence?

At What If Advice, we help Australians create structured, tax-aware retirement plans that align super, pension eligibility and lifestyle goals.

Book a Retirement & Super Workshop and get a clear plan for your next stage.

General Advice Disclaimer

This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions.