Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

If you’re in your late 50s or early 60s and starting to think about retirement, you may have heard of a Transition to Retirement (TTR) strategy.

It’s often talked about as a way to:

reduce your working hours but maintain income

boost your super faster

potentially save tax (in certain situations)

ease into retirement without a sudden income drop

But here’s the key:

TTR can be valuable, but it’s not a “magic trick” and it’s not worth it for everyone.

A good TTR strategy depends on:

your age and preservation age

how much super you have

your income and tax bracket

whether you plan to keep working

your cash flow needs

your retirement timeline

This article breaks it down in plain English so you can understand how it works and whether it might suit you.

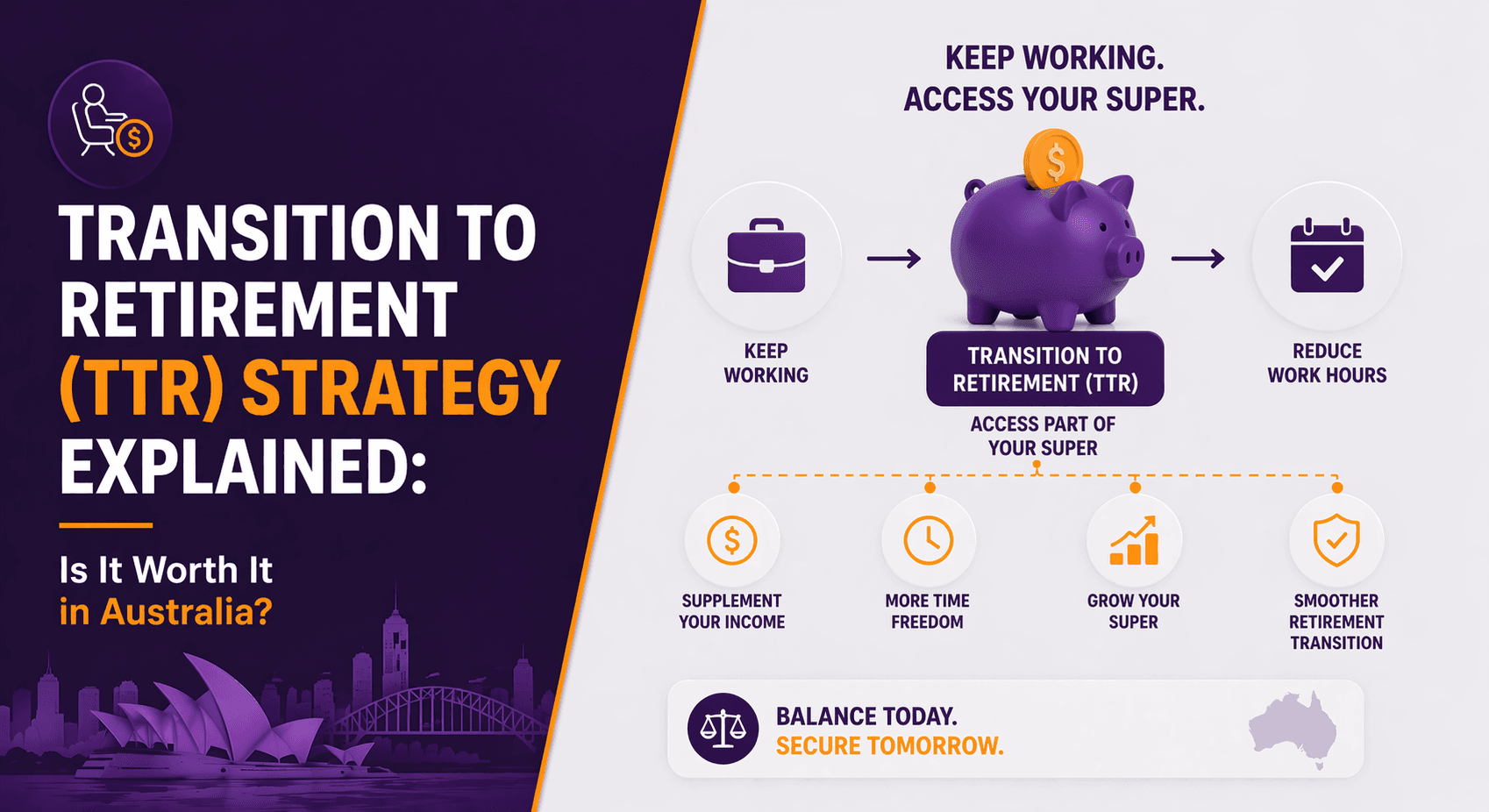

What Is a Transition to Retirement (TTR) Strategy?

A Transition to Retirement strategy lets you access some of your super once you’ve reached your preservation age, even if you’re still working.

You do this by starting a TTR pension (also known as a transition to retirement income stream).

Instead of withdrawing a large lump sum, the money is paid to you as a regular income stream.

This can allow you to:

reduce your work hours and top up income from super

keep working full-time but use TTR to restructure contributions

use a “replace income” strategy while salary sacrificing into super

When Can I Start a TTR Pension?

You can generally start a TTR pension once you’ve reached preservation age.

For most Australians, preservation age is 60, but it depends on your date of birth.

Important: TTR access isn’t full access. It’s a restricted form of access that comes with limits on how much you can withdraw each year.

How Does a TTR Pension Work?

Here’s the simple process:

You reach preservation age

You start a TTR pension inside your super fund

Your super is converted into an income stream account

Each year, you can withdraw an amount within limits (set by law and fund rules)

You continue working (full-time or part-time)

Key restriction: you can’t withdraw unlimited amounts

A TTR pension generally:

has a minimum annual drawdown amount

also has a maximum annual drawdown limit (until you meet full retirement conditions)

The limits can change and vary depending on your age, so always check current rules.

Why Do People Use a TTR Strategy?

There are two main reasons Australians use TTR:

1) Reduce work and maintain income

This is the most straightforward use.

You might want to move from:

5 days to 3 days per week

full-time to part-time

a physically demanding role into lighter work,

Without taking a big drop in take-home pay.

A TTR pension can help top up the income gap.

2) Boost super using contribution recycling (in some cases)

This is the “strategic” version of TTR.

The idea is:

you salary sacrifice more into super (concessional contributions)

you use the TTR pension withdrawals to replace the pay you sacrificed

in some situations, this can increase your super balance over time and improve tax efficiency

However, whether this works depends heavily on:

your marginal tax rate

fees inside your super

investment returns

how long you run the strategy

your ability to salary sacrifice within caps

This is where the “is it worth it?” question really matters.

Is a TTR Strategy Still Tax Effective?

Historically, TTR strategies were heavily marketed for tax savings.

But rules have changed over the years, and tax benefits are not always as strong as they once were.

These days, a TTR strategy is most useful for:

income smoothing (reducing work hours)

maintaining lifestyle without full retirement

contribution boosting (for the right income levels and timeframes)

improving retirement readiness with structure and planning

So yes, it can still be worth it. But only when the numbers stack up.

Pros of a Transition to Retirement Strategy

1) Helps you reduce work without losing income

If your goal is lifestyle and flexibility, this can be a big win.

2) Can help you keep contributing while drawing income

You can continue working and contributing to super while also receiving a pension payment.

3) May boost your super over time (in the right setup)

For some people, salary sacrificing plus TTR withdrawals can grow super faster; especially if you would otherwise spend that money.

4) Helps you “test” retirement income

It can be a good trial run to understand how retirement income feels before you fully retire.

5) May improve retirement planning outcomes

It can create a smoother transition into a full account-based pension later on.

Cons (and Risks) of a TTR Strategy

1) You may reduce your super faster than expected

If you’re drawing from super too early without a clear plan, you may deplete your balance more quickly.

2) Fees can reduce benefits

Starting a pension account may come with:

additional administration costs

higher fund fees

complexity that reduces outcomes

3) The tax benefit may be minimal

If your income isn’t in a suitable tax bracket, the strategy may not save meaningful tax compared to the extra admin and fees.

4) Investment risk still applies

Your super continues to be invested, so market downturns can impact your balance while you’re withdrawing income.

5) Limits on withdrawals apply

TTR is not full access. You can’t just withdraw your full balance unless you meet full retirement conditions or reach 65.

Who Might a TTR Strategy Suit?

A TTR strategy may be worth considering if you:

have reached preservation age (usually 60)

want to cut back work hours but keep income stable

have enough super to support pension payments

have stable employment income

are close enough to retirement that planning matters (5–10 years)

can benefit from salary sacrifice or contribution strategies

want to create a structured retirement pathway

Who Might Not Benefit Much?

A TTR strategy may be less useful if:

your super balance is low and withdrawals would reduce long-term security

you’re already earning a lower income (limited tax benefit)

you can’t salary sacrifice much

your super fund has high pension fees

you plan to retire very soon (too little time for benefits to compound)

you don’t need income top-ups and just want access to cash

A Simple Example of How a TTR Strategy Works

Let’s say:

you are 60

you earn $100,000

you want to reduce work hours but maintain your lifestyle

you have a healthy super balance

You might:

reduce work to 4 days/week

start a TTR pension to top up income

continue receiving super contributions through work

optionally salary sacrifice to keep building super

The key advantage here might not be tax, it might be lifestyle flexibility without financial stress.

Common Mistakes to Avoid With TTR

Mistake 1: Starting one without clear goals

If you don’t know whether your goal is income replacement or super boosting, the strategy can become messy.

Mistake 2: Not checking caps and limits

Salary sacrifice and concessional contributions must stay within ATO caps.

TTR pension withdrawals also have limits.

Mistake 3: Not accounting for fees

If your TTR pension adds higher fees, it can erode the benefits.

Mistake 4: Forgetting the impact on long-term retirement income

Drawing down early without modelling can reduce income later; especially if retirement lasts 25+ years.

Mistake 5: Not reviewing strategy yearly

A TTR strategy should be reviewed annually because:

your income may change

tax rules can change

super returns fluctuate

retirement plans evolve

Key Takeaways

TTR allows you to access some super after reaching preservation age while still working

It’s mainly used to reduce work hours or restructure contributions

Tax benefits exist in some cases, but not always

Fees, withdrawal limits and strategy design matter

It’s often most useful 5–10 years before retirement

Personal modelling is the best way to know if it’s worth it

FAQ

1) What is a Transition to Retirement (TTR) strategy?

A TTR strategy lets you access some of your super as an income stream after preservation age, while still working.

2) Can I start a TTR pension at 60?

Yes, if your preservation age is 60 (which it is for most Australians born after 1 July 1964).

3) Can I withdraw my whole super using TTR?

No. TTR pensions have annual limits and do not provide full access unless you retire or reach age 65.

4) Is a TTR strategy still worth it for tax savings?

Sometimes, but the tax benefit depends on your income, contribution level, fund fees, and how long you run the strategy.

5) Is a TTR strategy good if I want to reduce work hours?

Yes. This is one of the most common and practical reasons to use a TTR strategy.

A Transition to Retirement strategy can be a great way to ease into retirement; especially if you want to reduce work hours without sacrificing lifestyle.

But it’s not automatically “worth it”. The only way to know is to model the numbers based on your:

super balance

income

expected retirement age

tax situation

lifestyle goals

Still asking “what if” about your finances?

That’s exactly where clarity begins.

Whether you’re planning ahead, growing wealth, or simply want confidence in your financial decisions, the advisers at What If Advice can help you turn questions into a clear, personalised plan.

👉 Book a free 15-minute strategy session or get in touch today at

whatifadvice.com.au