Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

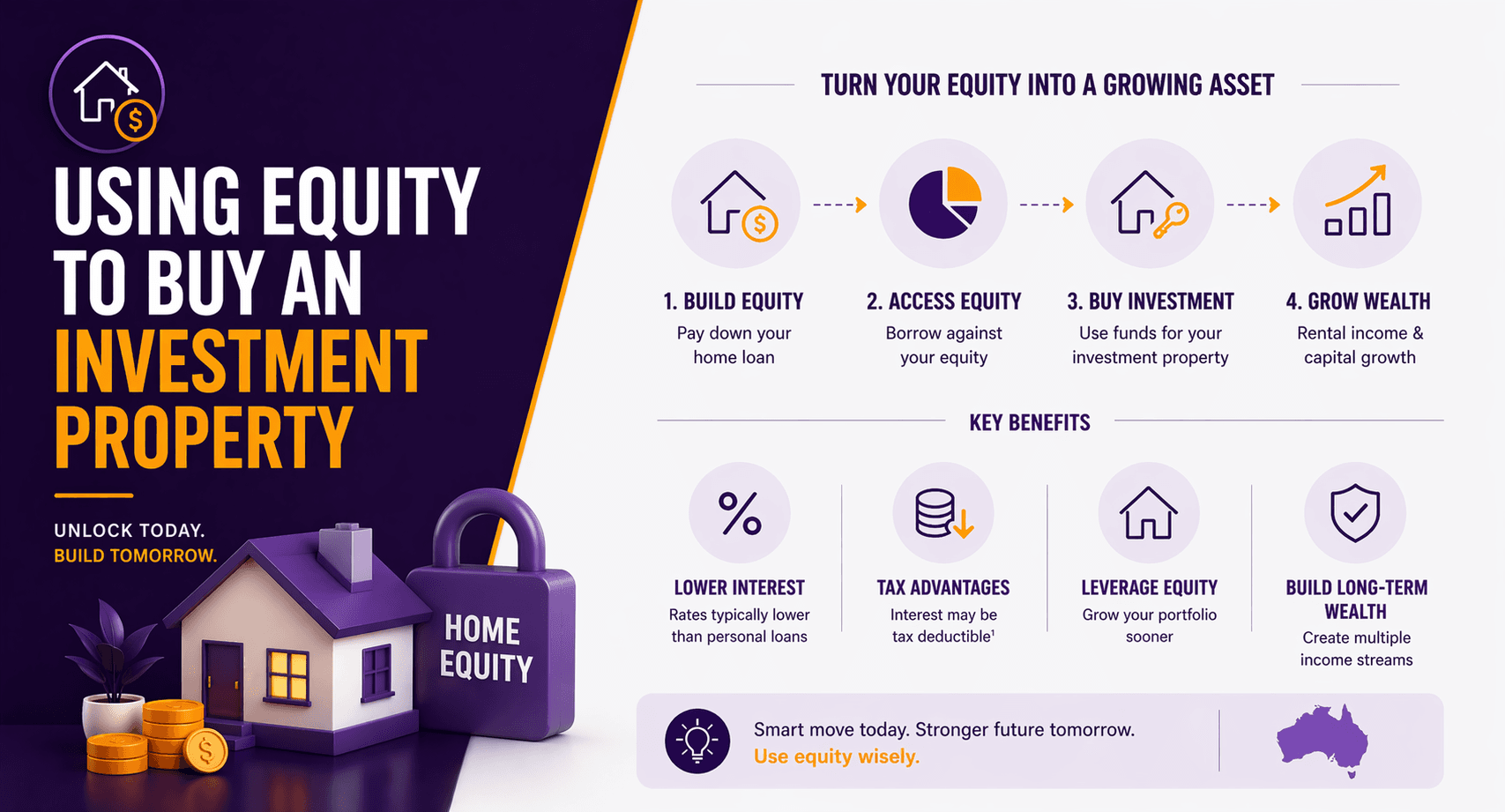

Using Equity to Buy an Investment Property in Australia

Using equity in your home is one of the most common ways Australians enter the property investment market.

The short answer:

You can use your home’s equity as a deposit to buy an investment property, but it increases your overall risk.

Done well, it can accelerate wealth building. Done poorly, it can stretch your finances and limit future flexibility.

What Is Equity?

Equity is the difference between:

Your property’s value

Your remaining loan balance

Example:

Property value: $900,000

Loan balance: $500,000

Equity = $400,000

But not all of this is usable.

How Much Equity Can You Access?

Most lenders allow borrowing up to 80% of your property value without paying Lenders Mortgage Insurance (LMI).

Example:

Item | Amount |

Property value | $900,000 |

80% lending limit | $720,000 |

Current loan | $500,000 |

Usable equity | $220,000 |

This $220,000 can potentially be used as:

Deposit

Stamp duty

Purchase costs

(Subject to lender policies and your borrowing capacity.)

How Using Equity Actually Works

You don’t “withdraw cash” from your house.

Instead, you:

Refinance or top up your existing loan

Create a separate loan split for investment purposes

Use those funds as your deposit

This keeps:

Owner-occupied debt separate

Investment debt structured correctly

Why Australians Use Equity to Invest

1. Enter the Market Sooner

You don’t need to save a full cash deposit.

2. Leverage Growth

If your property has increased in value, you can use that growth to acquire another asset.

3. Build a Property Portfolio

Equity is often used repeatedly to expand a portfolio over time.

Example Scenario

Emma (Melbourne):

Home value: $800,000

Loan: $450,000

Usable equity: ~$190,000

She uses:

$120,000 → deposit

$30,000 → costs

Result:

Purchases a $600,000 investment property

No need to save a separate deposit

Key Risks of Using Equity

This is where things get less exciting and more real.

1. Increased Debt Exposure

You’re increasing your total debt.

If:

Interest rates rise

Rental income drops

You still need to cover repayments.

2. Cash Flow Pressure

Investment properties don’t always cover their own costs.

You may need to fund:

Shortfalls

Maintenance

Vacancies

3. Property Market Risk

If property values fall:

Your equity reduces

Your loan-to-value ratio increases

This can limit future borrowing.

4. Overleveraging

Using too much equity too quickly can leave you financially stretched.

This is how people end up “asset rich, cash poor.”

Equity vs Cash Deposit: What’s the Difference?

Factor | Using Equity | Using Cash |

Upfront savings required | Low | High |

Debt level | Higher | Lower |

Liquidity | Preserved | Reduced |

Risk | Higher | Lower |

Speed to invest | Faster | Slower |

Structuring Your Loan Correctly Matters

This part is often overlooked and quietly causes problems later.

A proper structure may involve:

Separate loan splits

Clear purpose for each loan

Avoiding mixed-use loans

This can affect:

Tax deductibility (subject to ATO rules)

Clarity of repayments

Long-term flexibility

Can You Use Equity Without Refinancing?

Sometimes yes, through:

Loan top-ups

Line of credit

But refinancing often provides:

Better rates

Cleaner loan structure

When Using Equity May Make Sense

Your property has grown in value

You have stable income

You can comfortably manage higher repayments

You have a long-term investment strategy

When It May NOT Be the Right Move

You’re already financially stretched

You’re relying on optimistic rental assumptions

You don’t have a buffer for unexpected costs

You’re unclear on your investment strategy

Key Question: Should You Use Equity to Invest?

Using equity is a strategy, not a shortcut.

It works best when:

It aligns with a broader financial plan

Risks are understood and managed

Borrowing is sustainable

Without that, it becomes speculation disguised as strategy.

FAQs

1. Do I need a deposit to buy an investment property?

Yes, but equity can be used instead of cash savings.

2. Can I use 100% equity to buy property?

In some cases, yes, but you still need sufficient borrowing capacity and may incur higher risk.

3. Will I pay LMI when using equity?

Not if total borrowing remains within 80% LVR (subject to lender rules).

4. Is using equity risky?

Yes. It increases your overall debt and exposure to market and interest rate changes.

5. Can I use equity for multiple properties?

Potentially, if your equity and borrowing capacity allow.

6. Does equity guarantee loan approval?

No. Lenders also assess income, expenses, and credit profile.

7. Is interest on equity loans tax deductible?

It may be if used for investment purposes, subject to current ATO rules and advice from a qualified professional.

Thinking About Using Equity to Invest?

Using equity can be a powerful way to enter the property market sooner and build long-term wealth.

But it also increases your financial exposure and requires careful structuring to avoid costly mistakes.

Before making a decision, it’s important to understand:

How much you can safely borrow

How the loan should be structured

Whether the strategy aligns with your long-term goals

A tailored approach can help ensure you’re not just buying another property, but building a sustainable investment strategy.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional financial advice. Information is subject to current ATO and Services Australia rules and may change over time.