Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

If you’ve ever thought:

“I’ve got a lump sum, can I put a big amount into super?”

You’ve probably come across the bring-forward rule.

This rule is one of the most useful (and misunderstood) parts of the superannuation system. When used correctly, it can help Australians boost their retirement savings faster; especially if you’ve received money from an inheritance, property sale, business sale, or savings.

But there’s a catch:

it only applies to non-concessional (after-tax) contributions

you must meet eligibility rules

and triggering it can limit what you can contribute for the next few years

In this guide, we’ll explain it clearly, no jargon, and show how to think about it safely.

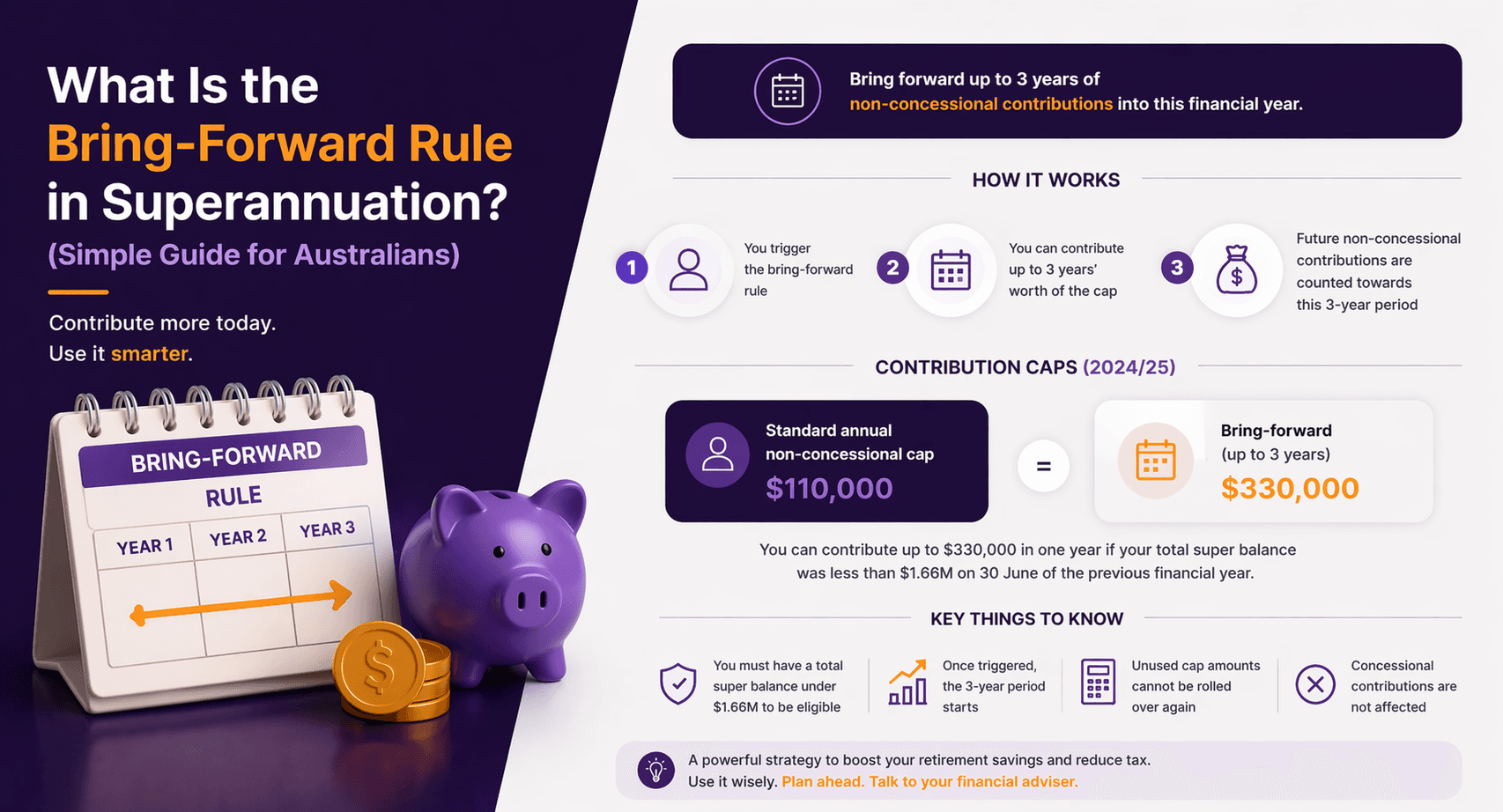

What Is the Bring-Forward Rule?

The bring-forward rule is an ATO rule that allows eligible people to contribute more than the normal annual non-concessional contribution cap by bringing forward future years’ caps.

In simple terms:

“You may be able to use up to multiple years’ worth of non-concessional contribution caps in one go.”

It’s designed for people who want to make a larger after-tax contribution to super than what’s normally allowed in a single year.

Quick Refresher: What Are Non-Concessional Contributions?

Non-concessional contributions are contributions made to super from after-tax money, meaning you’ve already paid income tax on it.

Examples include:

putting savings into super

contributing an inheritance

contributing money from selling an investment asset

personal contributions where you don’t claim a tax deduction

Non-concessional contributions generally aren’t taxed when they enter your super fund (subject to rules) but they are strictly capped.

The bring-forward rule only applies to non-concessional contributions. Not concessional contributions like employer super or salary sacrifice.

How Does the Bring-Forward Rule Work?

Normally, you can contribute up to the annual non-concessional cap each financial year (check current ATO rules).

But if you’re eligible, the bring-forward rule may allow you to contribute a larger amount by using future years’ caps in advance; often across a 2 or 3-year period.

What happens when you “trigger” it?

If you make a non-concessional contribution above the annual cap (and you’re eligible), you may automatically trigger the bring-forward rule.

When triggered:

you effectively lock in your allowed non-concessional contributions limit for the next few years

you generally can’t contribute additional non-concessional amounts beyond that limit until the bring-forward period ends

This is why planning matters, once it’s triggered, you can’t “undo” it.

Who Can Use the Bring-Forward Rule?

You may be able to use the bring-forward rule if you meet key eligibility requirements, including:

1) You are under a certain age

Eligibility is commonly linked to your age (e.g., under a specified age at the start of the financial year).

Rules can change, so always check current ATO rules.

2) Your total super balance is under the threshold

Your ability to make non-concessional contributions (and use bring-forward) can depend on your total super balance, the total of all your super accounts combined.

If your total super balance is too high, your non-concessional cap may reduce to zero.

This is one of the most common reasons people accidentally make excess contributions. They assume they can contribute, but their balance disqualifies them.

3) You haven’t already triggered a bring-forward period

You generally can’t start a new bring-forward arrangement if you’re still in an active bring-forward period from previous years.

A Simple Example

Let’s use a simplified scenario.

Example: One-off lump sum contribution

Chris is 55 and has $150,000 from selling an investment.

He wants to contribute it to super as after-tax money (non-concessional).

If Chris contributes more than the standard annual non-concessional cap, he may trigger the bring-forward rule and be allowed to contribute more than the usual yearly limit (up to the bring-forward maximum), depending on his eligibility.

Outcome:

He can boost super faster in one hit, but may have limited ability to make further non-concessional contributions for the next few years.

When Might the Bring-Forward Rule Be Useful?

The bring-forward rule is commonly used for retirement planning when someone has a lump sum and wants to move it into super.

Here are common scenarios where it may help:

1) Receiving an inheritance

If you inherit money and want to build retirement savings, the bring-forward rule may allow you to contribute more into super sooner.

2) Selling an investment property

If you sell an investment property and want to move proceeds into super (after tax), it may help you invest in a tax-effective environment.

3) Downsizing later in life

Some Australians combine strategies like downsizer contributions (separate rules apply) with non-concessional strategies.

4) Selling a business

If you sell a business and have surplus funds, a contribution strategy may help with retirement planning.

5) Catching up later in life

If you didn’t contribute much earlier, the bring-forward rule can sometimes be used to “catch up” closer to retirement, but it must be done carefully.

Important Things to Check Before You Use It

Before making a large non-concessional contribution, it’s worth checking these things first:

1) Your total super balance

Because eligibility is linked to your total super balance, you need to know your current total balance across all funds.

2) Whether you’ll trigger the bring-forward rule

Sometimes people accidentally trigger it by making a contribution they didn’t realise was above the cap.

3) How it affects your next few years

If you trigger bring-forward and use the full amount, you may not be able to make more non-concessional contributions for a period.

4) Whether a concessional strategy is better

Sometimes a concessional contribution strategy (like salary sacrifice or personal deductible contributions) can provide tax benefits, depending on your situation.

5) Your future plans

If you plan to:

sell another asset soon

receive another lump sum

use spouse contributions,

you want to plan so you don’t lock yourself out of future contributions.

Common Mistakes Australians Make With the Bring-Forward Rule

Mistake 1: Not realising they triggered it

Many people trigger the rule without intending to. Then discover they can’t contribute more for years.

Mistake 2: Contributing while ineligible due to total super balance

This can result in excess contributions and extra tax consequences.

Mistake 3: Assuming “after-tax means unlimited”

Non-concessional contributions are capped, and the bring-forward rule doesn’t remove the cap; it just brings forward future caps.

Mistake 4: Forgetting spouse contribution plans

If your spouse also wants to contribute, you may need to plan contributions strategically between both super accounts.

Bring-Forward Rule vs Other Super Contribution Options

The bring-forward rule is just one tool. Sometimes other contributions may be more suitable.

Other options that may apply (depending on your situation):

Salary sacrifice (concessional contributions)

Personal deductible contributions (concessional contributions

Spouse contributions

Downsizer contributions (different rules and eligibility)

Transition-to-retirement strategies (for older Australians)

The best strategy depends on:

your income

your age

your total super balance

retirement goals

how soon you want access to super

tax planning considerations

Key

The bring-forward rule lets eligible Australians contribute more to super using future years’ non-concessional caps

It applies only to non-concessional (after-tax) contributions

Triggering it can limit how much you can contribute for the next few years

Your eligibility depends on things like age, total super balance, and whether you’ve already triggered it

It can be useful for lump sums. Inheritance, property sales, business sales, savings

Always check current ATO rules before contributing large amounts

FAQ

1) What is the bring-forward rule in simple terms?

It’s a rule that may allow you to contribute multiple years’ worth of non-concessional caps into super in one go.

2) Does the bring-forward rule apply to concessional contributions?

No. It only applies to non-concessional (after-tax) contributions.

3) Do I automatically trigger the bring-forward rule?

You may trigger it if you contribute above the annual non-concessional cap and you’re eligible. It can happen automatically.

4) Can I use the bring-forward rule every year?

Not usually. Once triggered, you’re generally locked into a bring-forward period and can’t start another until it ends.

5) What happens if I exceed the bring-forward limit?

You may face excess contribution consequences and additional tax. It’s important to check caps and eligibility before contributing.

The bring-forward rule can be a powerful way to boost your super; especially if you’ve received a lump sum or want to build your retirement savings faster.

But because eligibility depends on your balance, age, and your past contributions, it’s easy to make a mistake if you go it alone.

Still asking “what if” about your finances?

That’s exactly where clarity begins.

Whether you’re planning ahead, growing wealth, or simply want confidence in your financial decisions, the advisers at What If Advice can help you turn questions into a clear, personalised plan.

👉 Book a free 15-minute strategy session or get in touch today at

whatifadvice.com.au