Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

One of the most common questions Australians ask about retirement is:

“When can I access my super?”

It’s a great question, because unlike a normal savings account, super is locked away until you meet certain rules. These rules are designed to make sure your super is used for retirement, not everyday spending.

In Australia, access to super depends on two key things:

Your preservation age

Meeting a condition of release

This guide explains what preservation age means, when you can withdraw your super, and the most common situations where Australians can access their super legally.

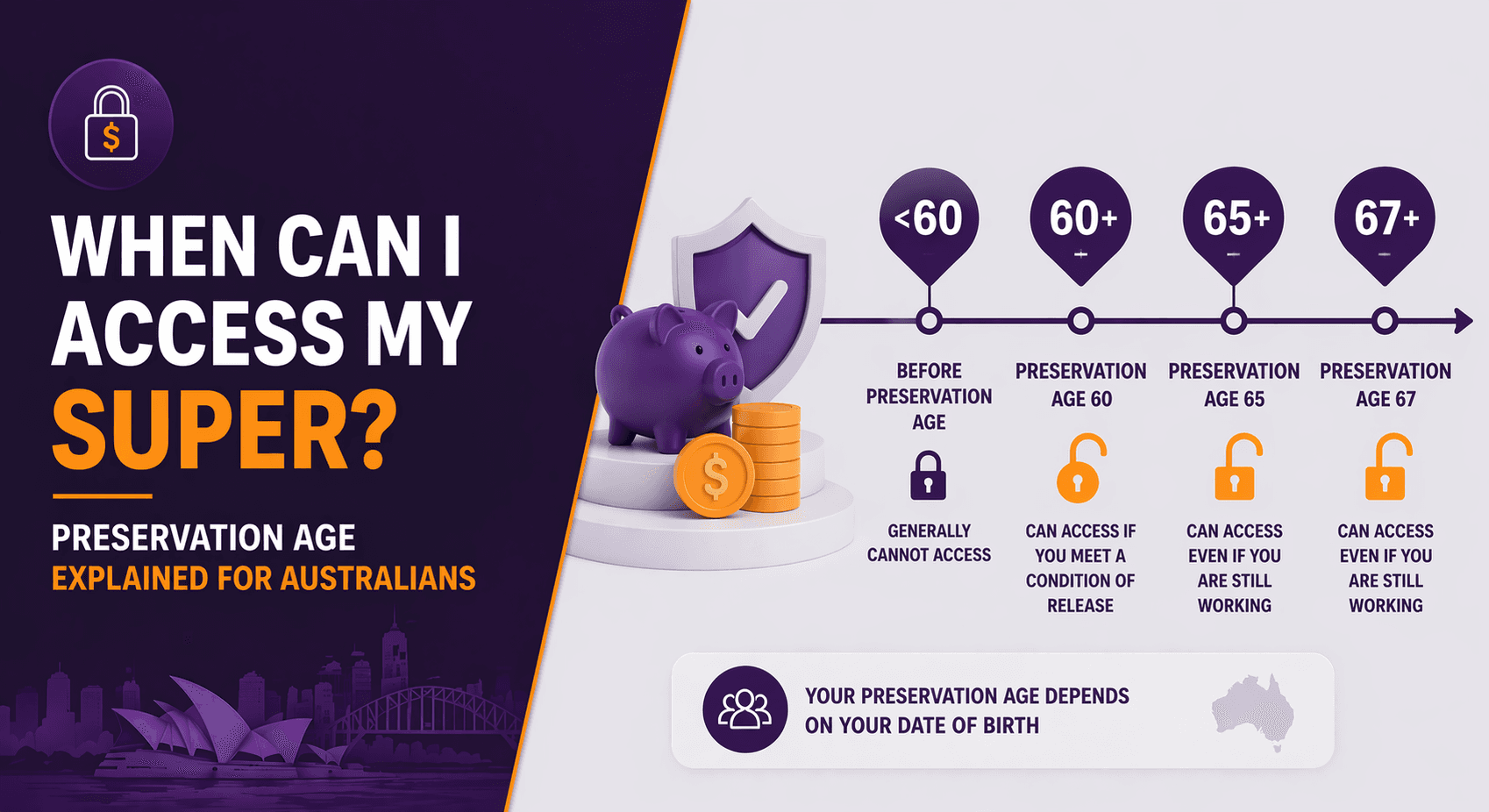

What Is Preservation Age?

Preservation age is the minimum age you must reach before you can access your super under normal retirement conditions (assuming you also meet a condition of release).

Your preservation age depends on your date of birth.

In simple terms:

If you were born earlier, your preservation age is lower

If you were born later, your preservation age is higher

This is because the government gradually increased the preservation age over time.

Tip: Preservation age is not the same as Age Pension age. They are separate systems with different rules.

Preservation Age in Australia (By Date of Birth)

Here’s a simple breakdown:

Born before 1 July 1960: preservation age is 55

Born 1 July 1960 – 30 June 1961: preservation age is 56

Born 1 July 1961 – 30 June 1962: preservation age is 57

Born 1 July 1962 – 30 June 1963: preservation age is 58

Born 1 July 1963 – 30 June 1964: preservation age is 59

Born on or after 1 July 1964: preservation age is 60

So for most Australians today, the preservation age is 60.

Preservation Age vs Age Pension Age: What’s the Difference?

Many people confuse these two, but they’re very different.

Preservation age (super access)

This is when you may be able to access super, depending on your circumstances.

Age Pension age (Centrelink)

This is when you may be eligible to receive the Age Pension from Services Australia, depending on your income and assets.

Your Age Pension age is generally higher than your preservation age.

If you retire early and access super before Age Pension age, your super may need to fund you for a longer period.

Can I Access My Super As Soon As I Reach Preservation Age?

Not automatically.

Reaching preservation age simply means you are old enough, but you still need to meet a condition of release.

Think of it like this:

Preservation age = “You’ve reached the minimum age”

Condition of release = “You’ve met the reason you’re allowed to withdraw”

What Are “Conditions of Release”?

A condition of release is a situation recognised by superannuation law that allows you to withdraw some or all of your super.

Some conditions of release allow:

full access to super

partial access only

restricted access (for specific reasons)

Below are the most common conditions that apply to everyday Australians.

The Most Common Ways Australians Access Super

1) Retirement after reaching preservation age

This is the most common way people access super.

To access your super under retirement:

you must have reached preservation age, and

you must have retired (i.e., stopped working)

Your fund will usually require a declaration that you’ve retired.

Example:

You turn 60 and leave work permanently. You can generally access your super under the retirement condition of release.

2) Reaching age 65 (even if still working)

This is one of the simplest rules.

Once you turn 65, you can generally access your super without needing to retire.

Even if you’re still working part-time or full-time, reaching 65 is itself a condition of release.

Example:

You’re 65 and still working 3 days a week. You can still withdraw your super if you want to.

3) Transition to Retirement (TTR) strategy (limited access)

If you’ve reached preservation age but aren’t ready to fully retire, you may be able to access a portion of your super using a Transition to Retirement (TTR) pension.

This allows you to:

reduce your work hours while still receiving income

supplement your income while contributing to super

potentially smooth your transition into retirement

However:

TTR withdrawals are usually restricted to an annual

you can’t withdraw your full balance under TTR unless you meet full retirement or another condition of release

Example:

You’re 60, still working, but want to reduce it to 3 days per week. A TTR pension may help cover the income gap.

4) Permanent incapacity

If you become permanently unable to work due to illness or injury, you may be able to access your super early.

This typically requires:

medical evidence

fund approval

meeting your fund’s criteria

5) Severe financial hardship or compassionate grounds (early access)

In limited circumstances, you may be able to access part of your super early if you’re in serious hardship.

There are strict eligibility rules, and it often requires approval.

Common situations may include:

being unable to meet reasonable living expenses

needing money for certain medical treatment

preventing foreclosure or forced home sale (depending on rules)

These rules are tightly controlled and you should check current ATO/APRA/Services Australia conditions before relying on this option.

6) Terminal medical condition

If you have a terminal medical condition, you may be able to access your super early, and there may be tax concessions depending on circumstances.

7) Death (benefits paid to beneficiaries)

Super can also be paid out to beneficiaries when someone dies. This process is called death benefit payments and has its own tax rules and nomination options.

Can I Access Super Early Just Because I Want To?

Generally, no.

Super is designed as retirement savings, and you can’t withdraw it early for things like:

paying off normal debts

buying a car

renovations (unless under strict hardship grounds)

starting a business

everyday expenses (unless under severe hardship rules)

The system is strict because it’s meant to protect long-term retirement outcomes.

What About Accessing Super at 60?

This is very common now, since most Australians have a preservation age of 60.

If you turn 60, you can usually access super if you:

permanently retire

ORstart a TTR pension (limited access)

But if you turn 60 and continue working full-time without a TTR arrangement:

you may not be able to access your super until you retire or reach 65

What About Accessing Super at 67?

Age 67 is often linked to the Age Pension, not super.

By the time you’re 67, you’ve already passed preservation age, and you can definitely access super (because you’ve also passed 65).

The bigger question at 67 is usually:

whether you’re eligible for the Age Pension

how to balance super withdrawals with Centrelink rules

Things to Consider Before You Access Your Super

Even when you’re eligible, accessing super is a major decision.

Key things to think about:

1) How long your retirement might last

Many Australians live 20–30 years in retirement.

Withdrawing super early can increase the risk of running out later.

2) Tax on withdrawals

Super withdrawals can be tax-free or taxable depending on:

your age

whether you’re taking a lump sum or pension

the taxable and tax-free components of your super

whether you meet a full condition of release

Tax rules can be complex, so always check current ATO rules or get advice.

3) Impact on Centrelink

If you receive or plan to apply for Centrelink payments (like Age Pension), super withdrawals and account balances can affect your entitlement depending on your age and how your money is held.

4) The best withdrawal strategy

You may need to choose between:

lump sum withdrawals

account-based pension

transition to retirement pension

a combination strategy

This is where a retirement plan can save you from costly mistakes.

Key Takeaways

Preservation age is the minimum age you can access super (most Australians: 60)

You must meet a condition of release to withdraw super

Retirement after preservation age is the most common condition

Turning 65 gives you full access even if you keep working

TTR pensions allow limited access if you’re still working

Early access is only allowed in specific, strict situations

Super access decisions can affect tax, Centrelink and long-term retirement income

FAQ

1) What is preservation age in Australia?

Preservation age is the minimum age you must reach to access your super under normal retirement conditions. For most Australians, it’s 60.

2) Can I access super at 60?

You may be able to if you retire permanently, or through a Transition to Retirement (TTR) pension with limited access.

3) Can I access super at 65 even if I’m still working?

Yes. Turning 65 is a condition of release, meaning you can access your super even if you’re still working.

4) Is preservation age the same as Age Pension age?

No. Preservation age relates to accessing your super. Age Pension age relates to Centrelink and eligibility for the Age Pension.

5) Can I withdraw super early for financial hardship?

In some situations, yes. But the rules are strict and you must meet eligibility requirements. Always check current ATO and Services Australia rules.

Understanding preservation age is one of the most important steps in planning a retirement that feels safe and stress-free.

The big takeaway is this:

You can’t always access super just because you reach a certain age. You need preservation age and a condition of release.

Once you are eligible, the way you access your super can affect your long-term retirement income, tax, and Centrelink outcomes.

Still asking “what if” about your finances?

That’s exactly where clarity begins.

Whether you’re planning ahead, growing wealth, or simply want confidence in your financial decisions, the advisers at What If Advice can help you turn questions into a clear, personalised plan.

👉 Book a free 15-minute strategy session or get in touch today at

whatifadvice.com.au

Disclaimer

This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions.