Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

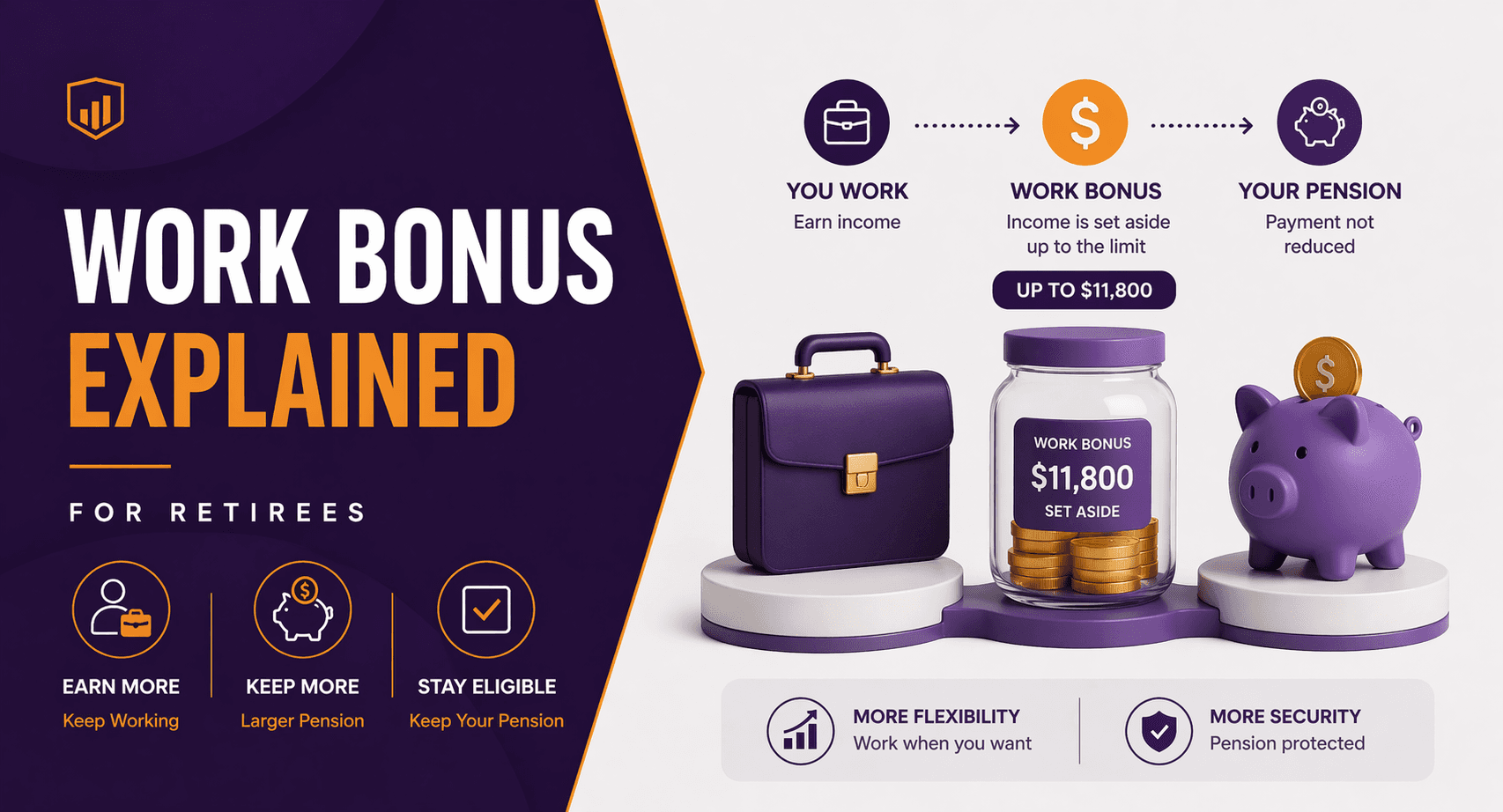

Work Bonus Explained for Retirees

Many Australians choose to continue working after reaching Age Pension age.

Part-time work can provide additional income, social engagement and a sense of purpose. However, retirees often worry that earning money will immediately reduce their Age Pension.

The Work Bonus helps address this concern.

It allows Age Pension recipients to earn employment income without immediately affecting their pension payment under the income test.

(All rules subject to current Services Australia guidelines.)

What Is the Work Bonus?

The Work Bonus is an incentive that allows Age Pensioners to earn employment income while reducing the impact on their pension payment.

It works by excluding a portion of employment income from the Age Pension income test.

This means retirees can earn some income before their pension begins to reduce.

The Work Bonus only applies to income from employment or self-employment, not investment income.

How Much Income Is Exempt?

Currently, the Work Bonus allows eligible pensioners to exclude up to $300 per fortnight of employment income from the income test.

This means:

Employment Income | Income Counted for Pension Test |

$300 per fortnight | $0 counted |

$400 per fortnight | $100 counted |

$600 per fortnight | $300 counted |

This exemption is applied before the Age Pension income test thresholds are calculated.

The Work Bonus Income Bank

One of the more useful features of the Work Bonus is the income bank.

If you do not use your Work Bonus exemption in a particular fortnight, it accumulates in your Work Bonus balance.

Key features include:

Up to $300 per fortnight can accumulate

Maximum balance currently $11,800

The balance can offset future employment income

This allows retirees who work irregularly to benefit from accumulated exemptions.

Example: How the Work Bonus Works

Susan receives the Age Pension and works occasionally.

Her Work Bonus bank has accumulated $3,000.

She takes a temporary job earning $2,000 in one fortnight.

Instead of the entire amount affecting her pension:

$300 Work Bonus applies

Remaining income can be offset by her Work Bonus balance

This significantly reduces the pension reduction.

Who Is Eligible for the Work Bonus?

You may be eligible if you:

Receive the Age Pension

Earn employment or self-employment income

Meet Age Pension eligibility requirements

The Work Bonus does not apply to income from:

Investments

Rental property

Superannuation pensions

Only employment income qualifies.

Why the Work Bonus Matters

The Work Bonus encourages older Australians to remain active in the workforce without losing pension benefits immediately.

Benefits may include:

Higher total income

Greater financial flexibility

Reduced reliance on savings

Continued social engagement

For many retirees, even a small amount of work can improve retirement sustainability.

Interaction With the Age Pension Income Test

The Work Bonus applies before the Age Pension income test.

Example:

If a single retiree earns $450 per fortnight from employment:

First $300 ignored under Work Bonus

Remaining $150 counted under income test

This reduces the impact on pension payments.

Common Mistakes Retirees Make

Many retirees misunderstand how the Work Bonus works.

Common issues include:

Assuming it applies to investment income

Forgetting to report employment income to Services Australia

Not realising unused bonus amounts accumulate

Believing any work will cancel their pension

Understanding the rules can help retirees maximise both income sources.

When to Review Your Retirement Income Strategy

If you plan to work in retirement, it is worth reviewing:

Total income sources

Super pension withdrawals

Age Pension thresholds

Work Bonus eligibility

A coordinated approach can help maximise retirement income.

FAQs

1. What is the Work Bonus for Age Pensioners?

The Work Bonus allows Age Pension recipients to exclude part of their employment income from the income test.

2. How much can you earn under the Work Bonus?

Currently up to $300 per fortnight of employment income may be excluded (subject to current Services Australia rules).

3. Does the Work Bonus apply to investment income?

No. It only applies to employment or self-employment income.

4. What is the Work Bonus income bank?

Unused Work Bonus amounts accumulate in a balance that can offset future employment income.

5. Do you need to apply for the Work Bonus?

Eligible Age Pension recipients generally receive it automatically when reporting employment income.

6. Does working reduce the Age Pension?

It can, but the Work Bonus reduces the impact of employment income under the income test.

Understand How Work Income Affects Your Pension

Many retirees assume earning income will automatically cancel their Age Pension. In reality, rules such as the Work Bonus can allow you to earn more while maintaining pension benefits.

At What If Advice, we help Australians structure retirement income strategies that coordinate super withdrawals, employment income and Age Pension rules under current Services Australia regulations.

If you are considering part-time work in retirement, strategic planning can help you maximise your income.

Book a retirement income strategy consultation with What If Advice.

General Advice Disclaimer

This article provides general information only and does not take into account your personal objectives, financial situation or needs. Before making financial decisions, consider whether the information is appropriate to your circumstances and seek personal advice from a licensed financial adviser. Age Pension, taxation and superannuation rules are subject to change under current Services Australia and ATO regulations.